C4ISR Market Size, Share, Trends and Forecast by Platform, Solution, End-Use Sector, Application, and Region, 2026-2034

Global C4ISR Market Size, Share, Trends & Forecast (2026-2034)

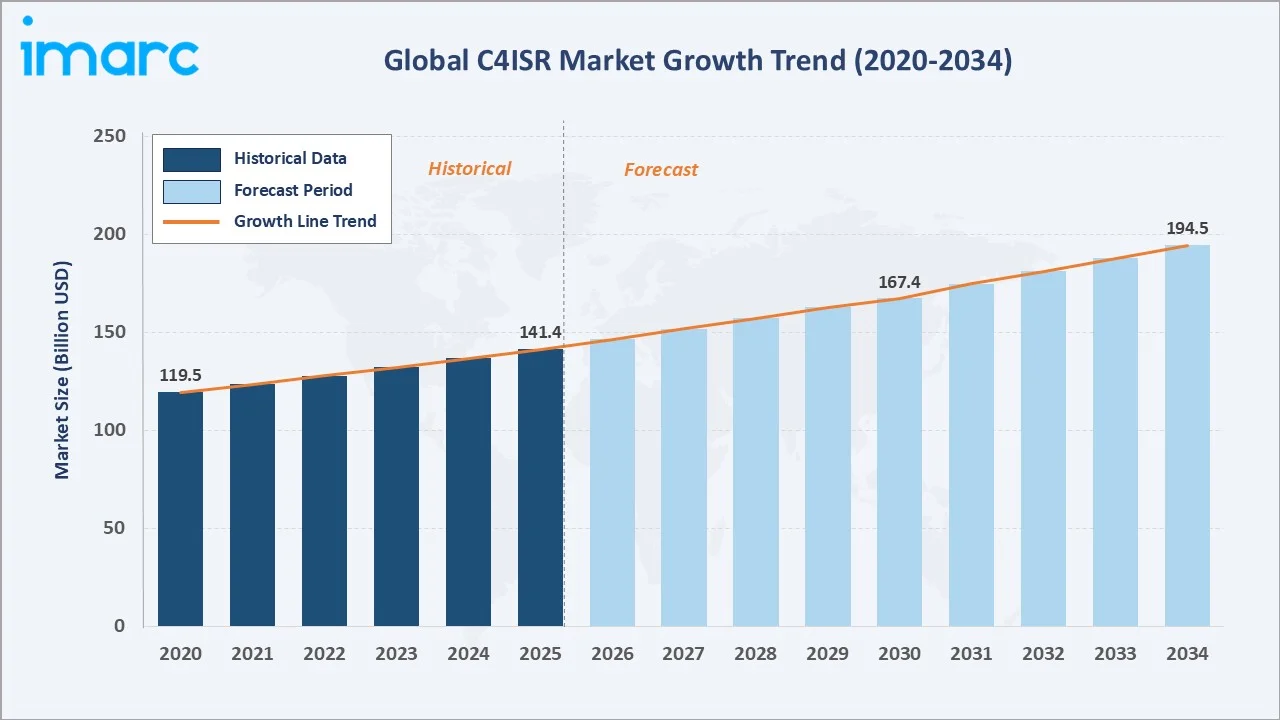

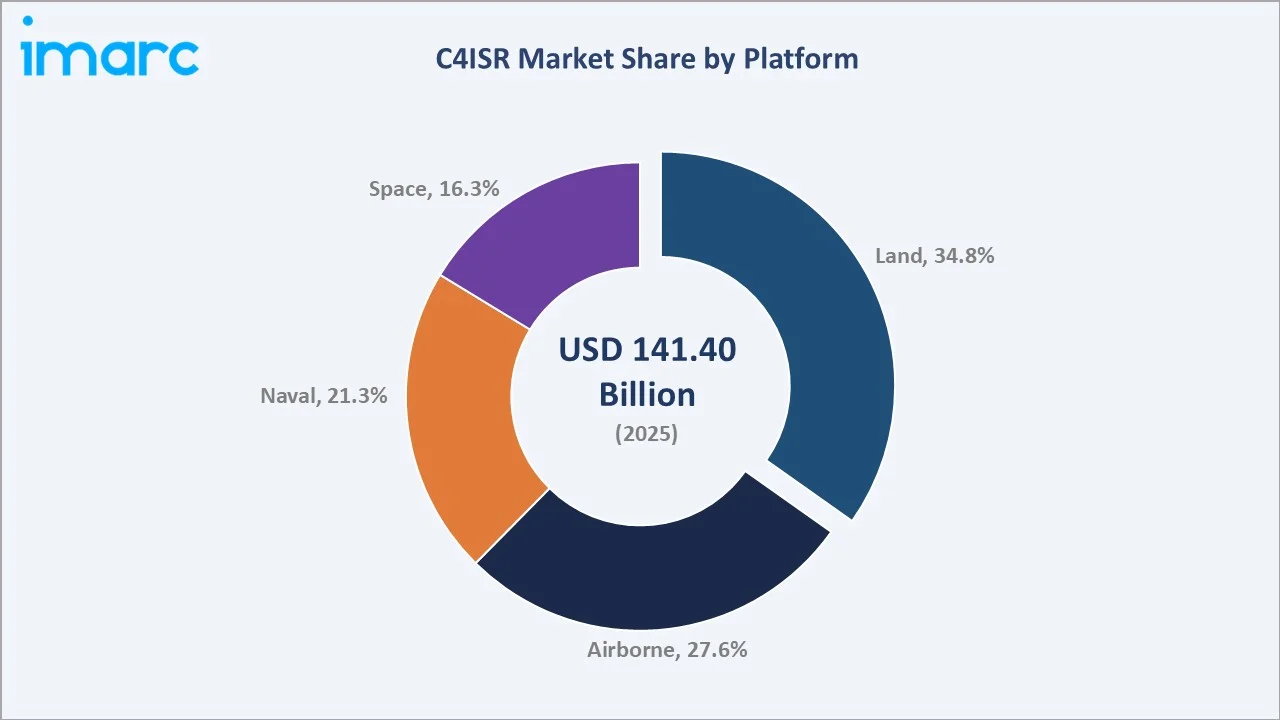

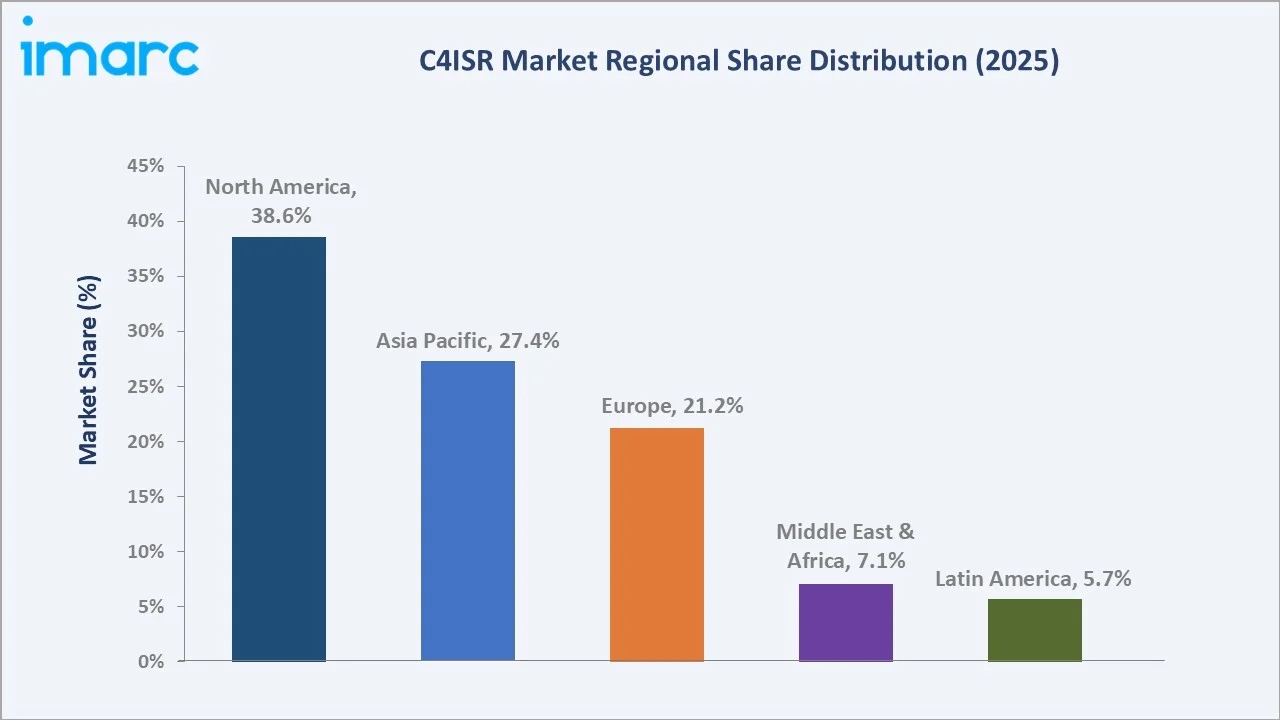

The global C4ISR market size was valued at USD 141.4 Billion in 2025 and is projected to reach USD 194.5 Billion by 2034, exhibiting a CAGR of 3.42% during 2026-2034. Rising geopolitical tensions, global defence budgets exceeding USD 2.4 Trillion in 2024, modernisation of armed forces, and integration of AI, cloud, and unmanned systems drive market growth. Land platforms lead with 34.8% share, while Products dominate the solution segment at 58.7%. North America accounts for 38.6% of global revenue, the largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 141.4 Billion |

|

Forecast Market Size (2034) |

USD 194.5 Billion |

|

CAGR (2026-2034) |

3.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Platform |

Land (34.8%, 2025) |

|

Leading Solution |

Products (58.7%, 2025) |

The market trajectory from 2020 to 2034 reflects a defensive-spending-driven path. Historical expansion from USD 119.5 Billion in 2020 to USD 141.4 Billion in 2025 shows steady accretion, with the forecast curve extending to USD 194.5 Billion by 2034.

To get more information on this market, Request Sample

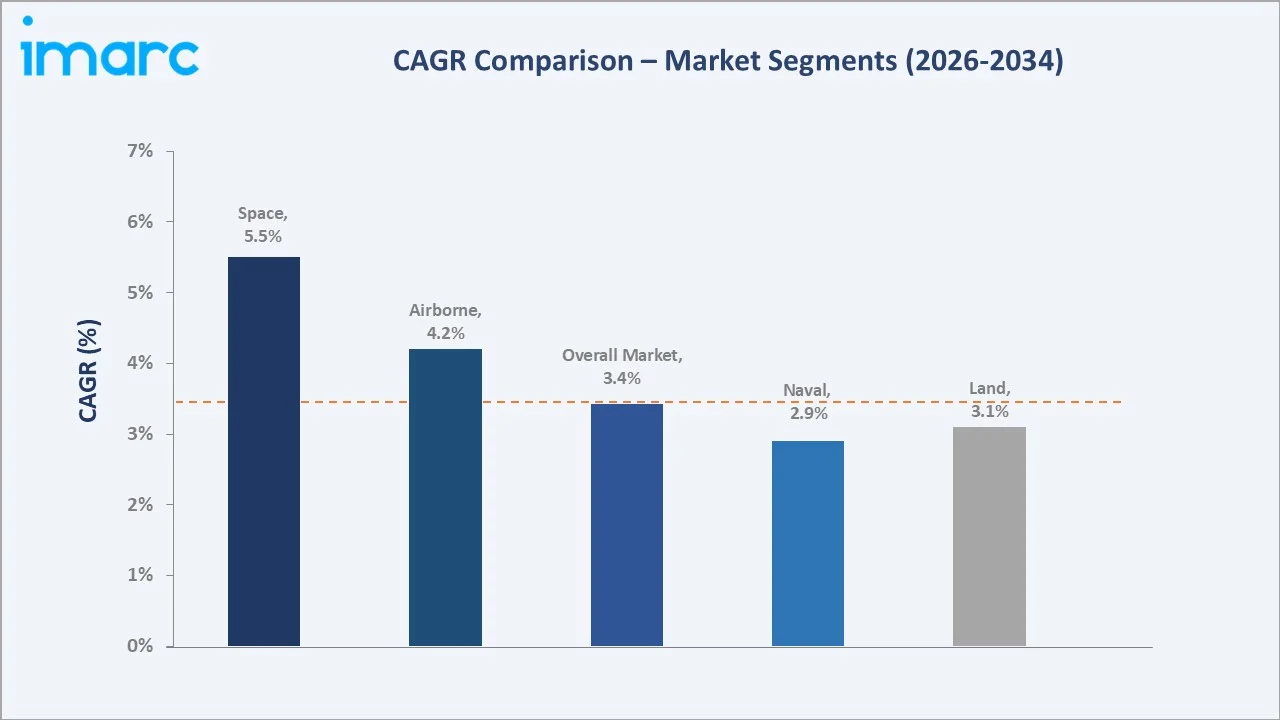

Segment-level CAGR comparisons highlight Space and Airborne platforms as the two fastest-growing sub-categories, fueled by satellite-based ISR and unmanned aerial reconnaissance expansion through 2034.

Executive Summary

The global C4ISR market is undergoing a structural transformation, shaped by intensifying geopolitical competition, the Russia-Ukraine conflict, Indo-Pacific deterrence priorities, and the convergence of AI, cloud, and unmanned systems within defence architectures. Valued at USD 141.4 Billion in 2025, the market is forecast to reach USD 194.5 Billion by 2034 at a CAGR of 3.42%. SIPRI recorded global military expenditure of USD 2.44 Trillion in 2023, a 6.8% real-terms rise.

Land platforms lead with 34.8% share in 2025, supported by battlefield management systems, soldier modernisation, and armoured vehicle C4 upgrades across NATO and Indo-Pacific forces. Airborne holds 27.6%, driven by UAV and ISR aircraft expansion. Naval commands 21.3%, and Space at 16.3% is the fastest-growing platform on LEO constellations.

North America dominates with 38.6% revenue share in 2025, anchored by the US DoD's FY2025 C3I budget exceeding USD 15 Billion. Asia Pacific at 27.4% is the fastest-growing region, led by China's modernisation and India's ~USD 21 Billion FY2025 capital outlay. Europe holds 21.2%, with MEA and Latin America at 7.1% and 5.7%.

Key Market Insights

|

Insight |

Data |

|

Largest Platform |

Land - 34.8% share (2025) |

|

Leading Solution |

Products - 58.7% share (2025) |

|

Leading Region |

North America - 38.6% revenue share (2025) |

|

Fastest-Growing Region |

Asia Pacific - 27.4% share (2025) |

|

Top Companies |

Lockheed Martin Corporation, Northrop Grumman, RTX, BAE Systems, L3Harris Technologies, Inc., General Dynamics Corporation, Leonardo S.p.A., Elbit Systems Ltd., Saab AB, and Anduril Industries |

Key Analytical Observations Supporting The Above Data:

- Land platforms' 34.8% share in 2025 reflects sustained demand for battlefield management systems, vehicle-mounted C4 suites, and soldier digital comms across NATO, Gulf, and Indo-Pacific modernisation.

- Products at 58.7% in 2025 are driven by hardware-intensive C4ISR procurement: radios, sensors, radars, ruggedised computing, displays, and avionics.

- North America's 38.6% leadership reflects sustained US DoD investment in JADC2, space-ISR programmes, and multi-domain C4ISR modernisation across all Combatant Commands.

- Asia Pacific's 27.4% share is driven by China's PLA modernisation, India's Atmanirbhar Bharat indigenous defence push, and Japan's accelerating defence build-up across air, naval, and cyber domains.

Global C4ISR Market Overview

C4ISR refers to the integrated architecture of Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance systems that enables military forces to collect, process, and act on battlefield information in near-real time. Modern ecosystems combine sensors, secure communications, edge computing, AI-driven analytics, and networked command centres into a single decision loop.

Applications span land, air, naval, and space forces, homeland security, border security, and intelligence-led law enforcement. Macroeconomic enablers include global military spending of USD 2.44 Trillion in 2023, rising NATO 2% of GDP commitment, and procurement reforms in the US, UK, Germany, Japan, and India targeting faster fielding of software-defined capabilities.

Market Dynamics

To evaluate market opportunities, Request Sample

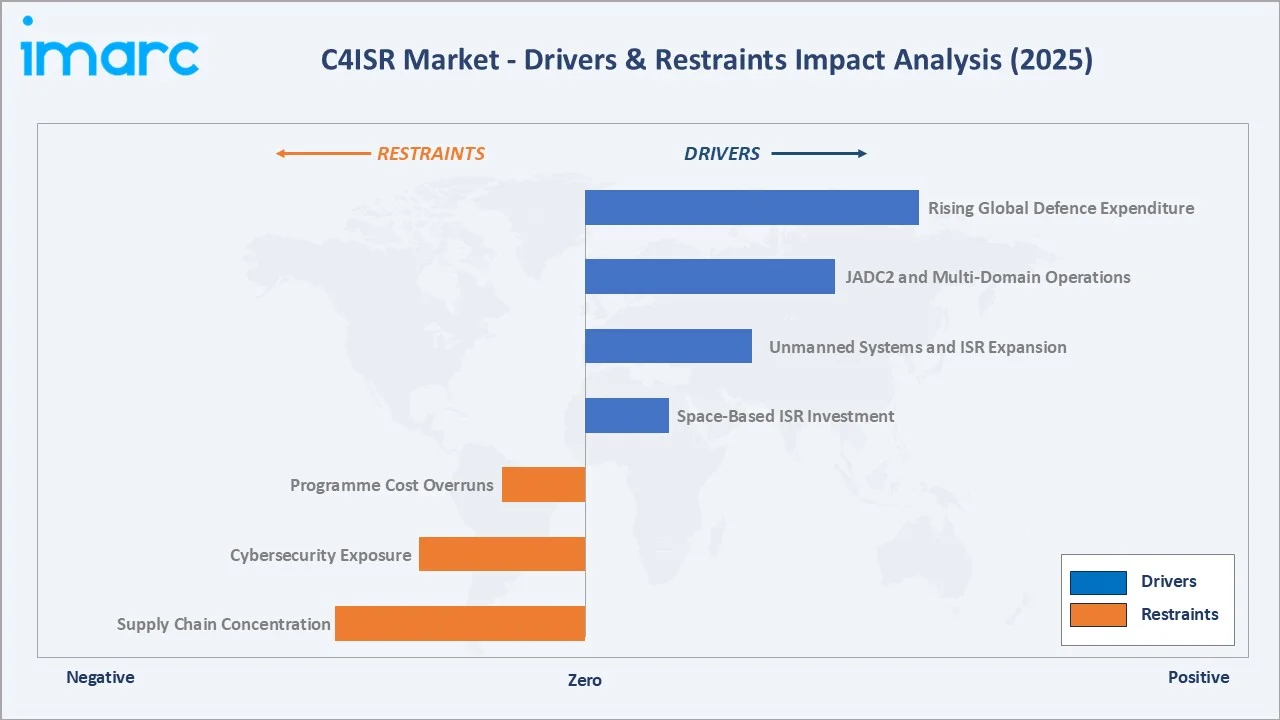

Market Drivers

- Rising Global Defence Expenditure: Global defence spending reached USD 2.44 Trillion in 2023 per SIPRI, the steepest real-terms rise since 2009, with 23 of 32 NATO members meeting the 2% of GDP benchmark in 2024.

- JADC2 and Multi-Domain Operations: The US DoD's JADC2 initiative connects sensors across all branches, with Army Project Convergence and Air Force ABMS representing multi-billion-dollar pipelines through 2034.

- Unmanned Systems and ISR Expansion: Global UAV procurement funding is set to increase from USD 14 Billion in 2024, with MQ-9-class platforms in over 35 nations, each pulling ISR payloads, satellite links, and ground-station C2.

- Space-Based ISR Investment: The US Space Development Agency has contracted over 400 satellites across Tranche 1 and 2, while allies build independent space-ISR capacity.

Market Restraints

- Programme Cost Overruns: Flagship C4ISR programmes frequently exceed planned budgets and timelines, diverting resources from parallel modernisation efforts across defence agencies.

- Cybersecurity Exposure: Increasingly networked C4ISR architectures expand attack surfaces, raising lifecycle hardening costs and introducing operational vulnerabilities across command and control systems.

- Supply Chain Concentration: Critical components such as advanced semiconductors, secure RF modules, and optical sensors remain sourced from a narrow supplier base, with export control frameworks further limiting cross-border integration.

Market Opportunities

- AI-Driven Decision Advantage: AI-enabled target recognition and intelligence fusion are being fielded at scale. Palantir's USD 480 Million Maven Smart System contract with the US Army in 2024 is the reference deployment.

- Proliferated LEO Communications: LEO constellations enable persistent, jam-resistant comms for deployed forces. The US Space Force has contracted over USD 13 Billion in LEO services through 2026.

- Indigenisation in Emerging Markets: Atmanirbhar Bharat, Saudi Vision 2030 offsets, and the UAE Tawazun Council create demand for local C4ISR production, opening JV and licensing streams for global primes.

Market Challenges

- Interoperability Across Allied Forces: Divergent communication standards, waveforms, and classification protocols across allied nations limit seamless data exchange, reducing the operational effectiveness of joint C4ISR investments.

- Legacy System Integration: Long equipment lifecycle cycles across defence ministries create significant technical complexity when integrating modern software-defined and IP-based capabilities alongside fielded legacy platforms.

- Cleared Talent Gaps: Persistent shortages of security-cleared professionals in AI, cryptography, and RF engineering constrain programme delivery timelines and slow the pace of C4ISR modernisation globally.

Emerging Market Trends

1. Joint All-Domain Command and Control (JADC2) as Architectural Reference

JADC2 is reframing C4ISR from platform-centric stovepipes to a service-mesh architecture linking every sensor to every shooter. The US Air Force's ABMS and the Army's Project Convergence 2024 fielded cross-domain kill chains at operational scale, with the UK and Australia adopting compatible reference models.

2. AI and Machine Learning at the Tactical Edge

AI is migrating from cloud-based analysis to on-platform inference. The Maven Smart System contract in 2024 crossed USD 480 Million, and NATO's DIANA accelerator is funding AI-for-defence start-ups, institutionalising AI as a C4ISR core capability.

3. Proliferated LEO Satellite Constellations

LEO constellations are reshaping ISR and communications economics. The SDA's Tranche 2 Transport Layer includes contracts for over 100 satellites and forms part of a broader proliferated LEO architecture designed to deliver resilient, low-latency global connectivity across transport and tracking layers.

4. Counter-UAS and Electronic Warfare Integration

Ukraine-war lessons since 2022 have driven a rapid EW refresh across NATO, with demand for directional jammers, RF-triangulation sensors, and counter-drone C2 integration rising sharply through 2026.

5. Software-Defined and Open-Architecture Systems

The US DoD's MOSA and the UK's Pyramid open-architecture initiatives mandate vendor-neutral interfaces, enabling faster upgrade cycles and reducing long-term sustainment costs.

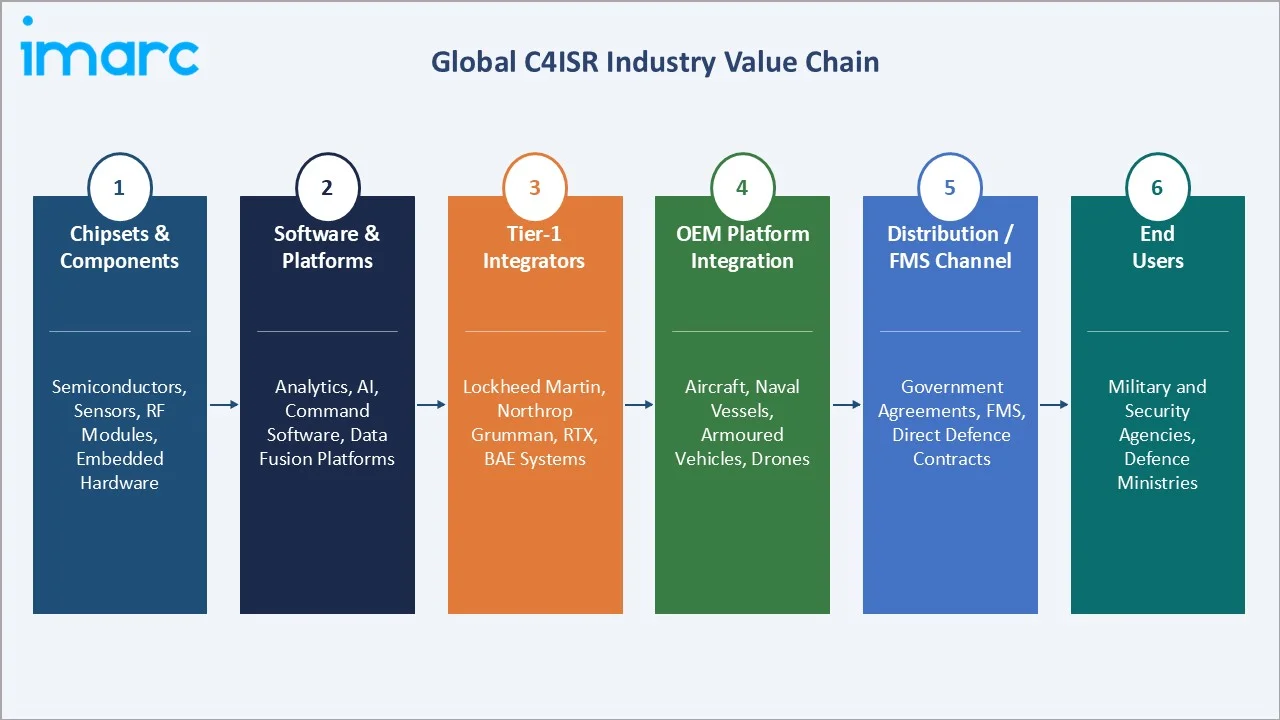

Industry Value Chain Analysis

The C4ISR value chain spans six integrated stages from component supply through fielded capability delivery, each with distinct competitive dynamics and margin profiles.

|

Stage |

Key Players / Examples |

|

Chipsets & Components |

Supplies semiconductors, sensors, RF modules, and embedded hardware that form the foundational building blocks of C4ISR systems. |

|

Software & Platforms |

Develops analytics, AI, command software, and data fusion platforms that convert raw data into actionable intelligence. |

|

Tier-1 Integrators |

Integrate hardware, software, and networks into complete C4ISR systems tailored to defense requirements. |

|

OEM Platform Integration |

Embeds C4ISR capabilities into end platforms such as aircraft, naval vessels, armored vehicles, and drones. |

|

Distribution / FMS Channel |

Facilitates procurement and international sales through government agreements, foreign military sales (FMS), and direct contracts. |

|

End Users |

Military and security agencies deploy and operate C4ISR systems for surveillance, decision-making, and mission execution. |

Prime integrators occupy the highest strategic value position, bundling sensors, software, and platforms into fielded C4ISR solutions. This position is increasingly contested by software-native entrants, Palantir, Anduril, Shield AI, and winning AI and autonomous-systems contracts.

Technology Landscape in the C4ISR Industry

AI, Machine Learning, and Automated Data Fusion

AI is the single most transformative technology across the C4ISR stack in 2026. Project Maven, expanded under Palantir's USD 480 Million Maven Smart System contract in 2024, automates target detection from ISR sensor feeds and compresses analysis time from hours to seconds.

Advanced Communications and Waveforms

The US Army's Integrated Tactical Network is fielding new software-defined radios, while LEO services, including Starshield, provide low-latency, jam-resistant beyond-line-of-sight links to deployed forces.

Space-Based ISR and Sensors

The US Space Development Agency has contracted over 400 satellites across Tranche 1 and 2. Allied programmes, France's Iris, the UK's ISTARI, and Japan's Michibiki expansion, are building redundant space-ISR capacity across the Indo-Pacific and Euro-Atlantic.

Cybersecurity and Zero-Trust Architectures

The US DoD's Zero Trust Reference Architecture mandates full implementation by 2027. Vendors are embedding continuous identity verification, microsegmentation, and encrypted inter-service traffic into every new C4ISR delivery.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Platform |

Land |

34.8% |

2025 |

|

Solution |

Products |

58.7% |

2025 |

|

End-Use Sector |

Defense |

🔒 |

2025 |

|

Application |

Electronic Warfare |

🔒 |

2025 |

|

Region |

North America |

38.6% |

2025 |

By Platform

Land platforms command a 34.8% majority share in 2025, reflecting ongoing ground-force modernisation, battlefield management systems, soldier digital-suite upgrades, and armoured vehicle C4 refits. The segment benefits from high-volume procurement, as armies are the largest uniformed services in every major defence nation.

To access detailed market analysis, Request Sample

Airborne holds 27.6% in 2025, supported by manned ISR aircraft (P-8, E-7, Rivet Joint) and rapid UAV fleet expansion. Naval at 21.3% is anchored by multi-year programmes such as the US Navy's Constellation-class frigate and Columbia-class submarine. Space at 16.3% is the fastest-growing platform, projected to expand above market CAGR through 2034 on LEO constellations and allied space-ISR programmes.

By Solution

Products dominate at 58.7% in 2025, reflecting capital-intensive C4ISR hardware: radios, sensors, radars, secure displays, ruggedised computing, and avionics. Product revenue is tied to platform build rates and mid-life upgrade cycles.

Services account for 41.3% in 2025 and are the faster-growing sub-segment. Drivers include software sustainment contracts, AI model training, managed cyber operations, and through-life support. The US DoD's shift toward outcome-based service contracts is structurally expanding the services share through the forecast period.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.6% |

US DoD C3I budget, JADC2, Space Development Agency, allied FMS demand |

|

Asia Pacific |

27.4% |

China PLA modernisation, India Atmanirbhar Bharat, Japan 2% of GDP target, AUKUS |

|

Europe |

21.2% |

NATO 2% benchmark, Russia-Ukraine response, EU European Defence Fund, UK ISTARI |

|

Middle East & Africa |

7.1% |

GCC modernisation, Saudi Vision 2030, Israel defence tech leadership, counter-insurgency |

|

Latin America |

5.7% |

Brazil F-39 Gripen ecosystem, Mexico border security, Colombia counter-narcotics ISR. |

North America commands a 38.6% revenue share in 2025, the most dominant regional position globally. The US DoD's FY2025 budget of USD 849.8 Billion includes a C3I allocation and Space Force funding of ~USD 29.4 Billion.

Asia Pacific at 27.4% in 2025 is the fastest-growing region, driven by rising defense modernization programs, expanding space and ISR capabilities, increasing indigenous procurement in China and India, Japan’s military normalization, and deepening strategic collaborations such as AUKUS Pillar 2.

Europe holds 21.2% in 2025, driven by heightened defense spending and capability upgrades in response to the Russia–Ukraine war, increased NATO readiness commitments, and EU-backed investments in C4ISR and cyber defense modernization. Middle East & Africa (MEA) at 7.1% is anchored by Gulf military modernization, growing investments in advanced surveillance and command systems, strong offset programs, and Israel’s leadership in indigenous C4ISR technologies. Latin America at 5.7% is led by expanding border-security initiatives, ISR deployments, and national modernization programs, particularly in Brazil and Mexico.

Competitive Landscape

|

Company Name |

Core Segment |

Market Position |

Core Strength |

| Lockheed Martin | Aegis, Sniper ATP | Leader | Integrated platforms, space, missile defence, AI-enabled ISR |

| Northrop Grumman | IBCS, E-2D, Global Hawk | Leader | Battle management, airborne ISR, space, classified systems |

| RTX | Raytheon Sentinel | Leader | Radars, EW, secure comms, space sensors, ISR payloads |

| BAE Systems | STORM EW, Link 16 | Leader | Electronic warfare, combat systems, secure comms, EW |

| L3Harris Technologies, Inc. | Falcon IV, WESCAM MX | Leader | Tactical radios, EO/IR sensors, airborne ISR, SIGINT |

| General Dynamics Corporation | WIN-T, MUOS | Challenger | Tactical communications, mission systems, IT services |

| Leonardo S.p.A. | OSPREY, SeaSpray | Challenger | Radars, airborne ISR, helicopters, EW |

| Elbit Systems Ltd. | DOMINATOR, SkyStriker | Challenger | Soldier systems, unmanned platforms, EW, UAS |

| Saab AB | GlobalEye AEW&C | Emerging | AI data fusion, software-defined C2, decision advantage |

| Anduril Industries | Lattice, Roadrunner | Emerging | Autonomous systems, AI-defined C2, counter-UAS |

The competitive landscape features a small core of global prime integrators dominating hardware-led programmes, complemented by a fast-rising cohort of software-native entrants, Palantir, Anduril, Shield AI, winning discrete AI and autonomous-systems contracts and increasingly competing directly with primes on flagship programmes.

Key Company Profiles

Lockheed Martin Corporation

Lockheed Martin is a leading global defense contractor specializing in advanced C4ISR systems, integrating sensors, communications, and command platforms across air, land, sea, space, and cyber domains.

- Product & Platform Portfolio: Aegis Combat System, Sniper ATP, PAC-3, TPY-4 radar, Next-Generation Interceptor, classified space payloads.

- Recent Developments: In April 2024, Lockheed Martin secured a ~USD 17 billion contract from the U.S. Missile Defense Agency to develop the Next Generation Interceptor (NGI), strengthening its role in next-generation homeland missile defense systems.

- Strategic Focus: Multi-domain integration, AI-enabled mission systems, space-based ISR, and next-generation hypersonic and classified intelligence systems.

Northrop Grumman

Northrop Grumman is a key provider of advanced C4ISR systems, leading strategic programs such as IBCS and contributing to next-generation platforms like the B-21 Raider.

- Product & Platform Portfolio: IBCS, E-2D Advanced Hawkeye, RQ-4 Global Hawk, MQ-4C Triton, B-21 Raider, SABR radar, space payloads.

- Recent Developments: In 2024, Northrop Grumman’s IBCS achieved live-fire integration milestones with Patriot and Sentinel radar systems, while the company expanded its open-architecture C2 footprint internationally, including deployments in Poland and broader engagement across European defense programs.

- Strategic Focus: Integrated air and missile defence C2, airborne and space ISR, unmanned systems, and JADC2-compatible architectures.

RTX

RTX is a major defense technology provider delivering radars, secure communications, electronic warfare systems, and space-based sensors through its Raytheon and Collins Aerospace businesses.

- Product & Platform Portfolio: Patriot, LTAMDS, SEWIP Block III, SPY-6, ARC-210 radios, AN/ALR-69A, LEO and GPS III payloads.

- Recent Developments: In 2024, RTX delivered the first LTAMDS radar to the US Army and scaled production of Patriot GEM-T interceptors under Ukraine-replenishment contracts.

- Strategic Focus: Next-generation radar, tactical and strategic secure communications, space sensors, and manufacturing scale-up.

Market Concentration Analysis

The global C4ISR market is moderately to highly concentrated. The top five players, Lockheed Martin, Northrop Grumman, RTX, BAE Systems, and L3Harris, collectively account for approximately 40-48% of global revenue.

The landscape is bifurcated. At the flagship tier, consolidation dominates: only the largest primes can sustain decade-long R&D and classified commitments for programmes such as JADC2, B-21, or GBSD. At the software and autonomous tier, fragmentation is rising: Palantir, Anduril, Shield AI, Applied Intuition, and Scale AI have collectively raised over USD 15 Billion in private capital since 2020, winning programme-of-record contracts and challenging traditional cost and time-to-field assumptions.

Investment & Growth Opportunities

Fastest-Growing Sub-Segments

Space-based ISR is the highest-growth sub-segment, anchored by LEO constellations and persistent-surveillance demand. AI-enabled C2 software is second-fastest, with Palantir's USD 480 Million Maven contract in 2024 indicating the scale now allocated to software-only C4ISR.

Emerging Market Expansion

India, Saudi Arabia, Poland, and Australia are the highest-potential emerging markets, driven by rising defense modernization, large-scale procurement programs, and strategic collaborations such as AUKUS Pillar 2, collectively creating substantial incremental demand for advanced C4ISR capabilities.

Venture & Private Investment Trends

Defence-tech private capital reached record levels in 2024, with major funding rounds for companies such as Anduril Industries, Shield AI, and Saronic highlighting strong investor interest in autonomous systems, AI, and next-generation defense platforms. Institutional initiatives like the NATO Innovation Fund and the Office of Strategic Capital are further accelerating structured investment into defence-tech ecosystems.

Future Market Outlook (2026-2034)

The global C4ISR market forecast projects expansion from USD 141.4 Billion in 2025 to USD 194.5 Billion by 2034 at a CAGR of 3.42%, driven primarily by software, space, and AI-enabled capability layers rather than incremental hardware.

Three structural discontinuities will reshape the industry through 2034. Software-defined, open-architecture C4ISR will displace platform-centric stovepipes, compressing upgrade cycles to sub-annual cadence. Space-based sensing and communications will migrate from premium overlay to baseline capability. AI-enabled decision support will shift from advisory to machine-speed C2, reshaping doctrine in contested scenarios.

By 2034, the industry will have partly transformed from a capital-equipment market to a hybrid hardware-software-services economy, with over 50% of incremental value captured by software, cloud, and AI-subscription streams.

Research Methodology

Primary Research

Primary research included 45+ structured interviews in 2024-2025 with programme directors at prime integrators, defence-ministry procurement leads across NATO and Indo-Pacific, software-defence executives, institutional defence-tech investors, and retired general officers. Interviews validated market sizing, segmentation, and competitive positioning.

Secondary Research

Secondary sources included SIPRI Military Expenditure Database, US DoD budget documents, NATO Financial and Economic Data, annual reports of listed primes, GAO defence assessments, Jane's Defence Weekly, IISS Military Balance, SAM.gov, UK DASA, and company 10-K filings through 2025.

Forecasting Models

Projections were derived using top-down and bottom-up models, cross-validated against government budget trajectories, programme-level procurement schedules, and historical patterns. Base, optimistic, and conservative scenarios were modelled to account for geopolitical and macroeconomic uncertainty.

C4ISR Market Report Coverage

|

Attribute |

Details |

|

Market Size (2025) |

USD 141.4 Billion |

|

Forecast Market Size (2034) |

USD 194.5 Billion |

|

CAGR (2026-2034) |

3.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation by Platform |

Land, Airborne, Naval, Space |

|

Segmentation by Solution |

Products, Services |

|

Regional Coverage |

North America, Asia Pacific, Europe, Middle East & Africa, Latin America |

|

Key Companies Profiled |

Lockheed Martin Corporation, Northrop Grumman, RTX, BAE Systems, L3Harris Technologies, Inc., General Dynamics Corporation, Leonardo S.p.A., Elbit Systems Ltd., Saab AB, and Anduril Industries |

|

Report Format |

PDF, Excel |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the C4ISR market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global C4ISR market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the C4ISR industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the C4ISR Market Report

The global C4ISR market was valued at USD 141.4 Billion in 2025, driven by rising defence budgets, multi-domain operations, and sustained investment in AI and space-based ISR.

The C4ISR market is projected to reach USD 194.5 Billion by 2034, growing at a CAGR of 3.42% during 2026-2034, led by JADC2 and space ISR.

Land platforms lead with a 34.8% share in 2025, driven by battlefield management systems, soldier modernisation, and armoured-vehicle C4 upgrades across global forces.

North America dominates with a 38.6% revenue share in 2025, anchored by the US DoD's FY2025 budget and dedicated C3I allocation exceeding USD 15 Billion.

Asia Pacific is the fastest-growing region, led by China's PLA modernisation, India's Atmanirbhar Bharat initiative, Japan's 2% GDP defence target, and AUKUS Pillar 2 collaboration.

Top companies include Lockheed Martin Corporation, Northrop Grumman, RTX, BAE Systems, L3Harris Technologies, Inc., General Dynamics Corporation, Leonardo S.p.A., Elbit Systems Ltd., Saab AB, and Anduril Industries.

Key drivers include rising global defence spending, JADC2 and multi-domain operations, unmanned-systems expansion, space-based ISR investment, and AI-enabled decision advantage across allied militaries.

Trends include JADC2 architecture, AI at the tactical edge, proliferated LEO constellations, counter-UAS and EW integration, and software-defined open-architecture system adoption.

Space-based ISR is growing rapidly due to proliferated LEO constellations, US Space Development Agency tranches, allied space programmes, and demand for persistent global coverage.

AI is automating target recognition, intelligence fusion, and predictive maintenance. Palantir's USD 480 Million Maven Smart System contract in 2024 exemplifies scaled AI deployment.

Products account for 58.7% of the market in 2025, reflecting capital-intensive hardware including radios, sensors, radars, ruggedised computing, secure displays, and avionics.

Challenges include programme cost overruns, cybersecurity exposure, supply-chain concentration, interoperability gaps, legacy system integration, and cleared defence-talent shortages across key markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)