Burn Care Market Size, Share, Trends and Forecast by Facility Type, Treatment Type, Burn Severity, Service Type, and Region, 2025-2033

Burn Care Market Size and Trends:

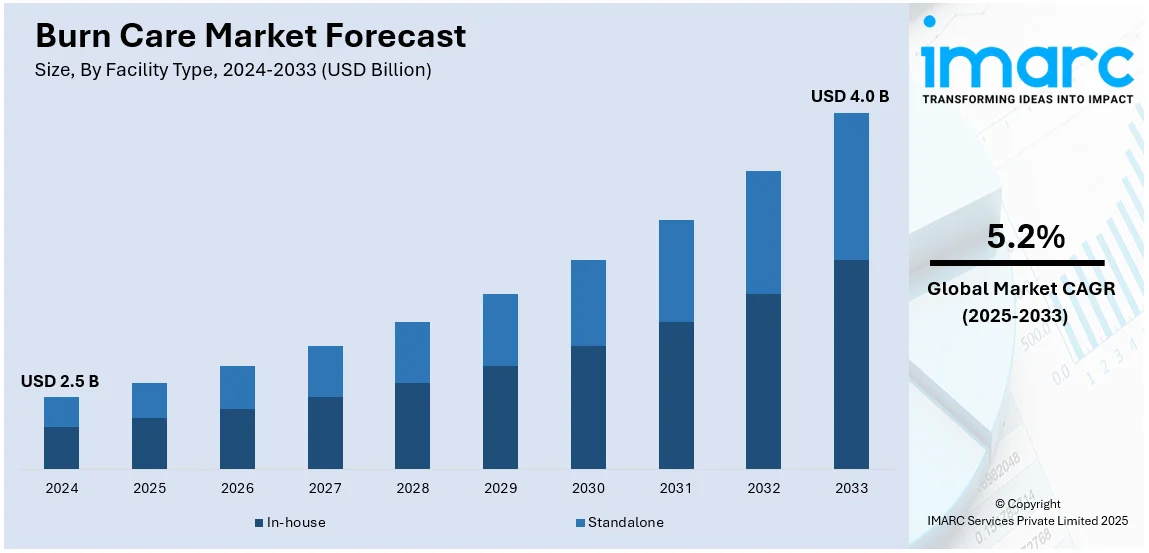

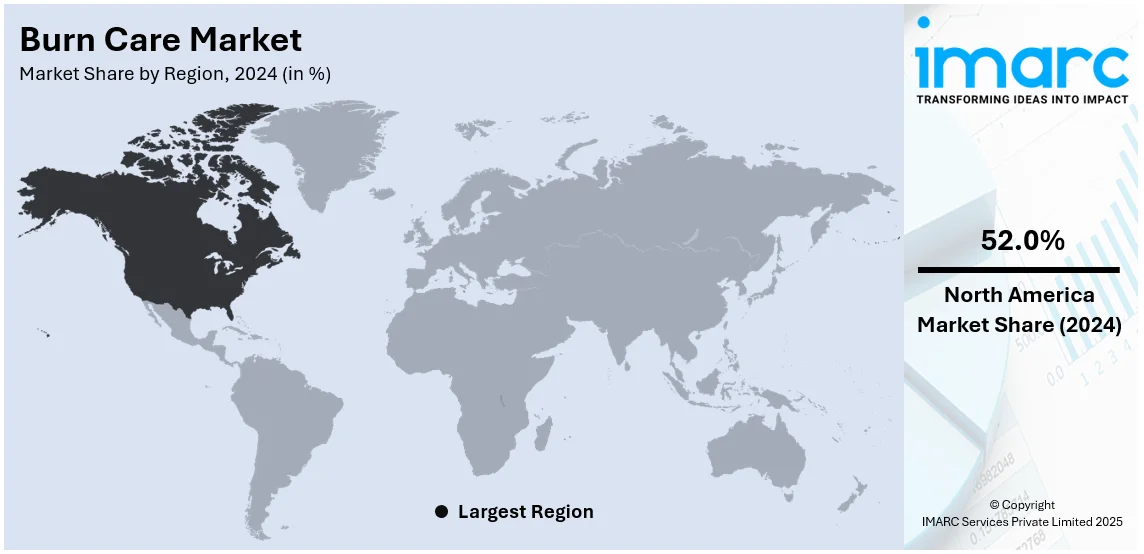

The global burn care market size was valued at USD 2.5 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 4.0 Billion by 2033, exhibiting a CAGR of 5.2% during 2025-2033. North America currently dominates the market, holding a significant market share of over 52.0% in 2024, due to well-established healthcare infrastructure, magnified adoption of advanced treatments, and escalating awareness about burn management.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 2.5 Billion |

|

Market Forecast in 2033

|

USD 4.0 Billion |

| Market Growth Rate (2025-2033) | 5.2% |

The global burn care market is mostly impacted by the heightening prevalence of burn injuries globally, mandating upgraded treatment solutions. Magnifying awareness regarding the critical need of proper wound management has boosted requirement for cutting-edge products, typically including enzymatic debridement agents, bioengineered skin substitutes, and antimicrobial dressing. Robust healthcare infrastructure, especially in developed economies, aids better availability to customized burn care. In addition to this, government programs and beneficial regulations also play a pivotal role in proliferating the market. Moreover, active innovations in technology and the ongoing launches of minimally invasive procedures have enhanced treatment outcomes significantly, further shaping a positive burn care market outlook.

The United States is a leading nation within the global burn care segment, mainly propelled by its resilient healthcare ecosystem, elevated utilization of leading-edge treatment technologies, and comprehensive network of specialized burn centers. A notable increase in burn injuries, combined with highly profitable reimbursement policies, guarantees easy availability of advanced care options. For instance, as reported by the American Burn Association, of the 3,800 fire and smoke inhalation-related fatalities each year, 3,010 occur due to structure fires, while 680 are attributed to vehicle fires. This equates to an average of one fire-related death every 2 hours and 17 minutes. Heavy investments in research and development projects and the establishment of leading manufacturers further improve the market’s prospects. Besides this, programs to enhance burn management as well as prevention, together with resilient clinical training initiatives for healthcare providers, establish the United States as a major hub for excellence and advancements in burn care.

Burn Care Market Trends:

Rising Adoption of Advanced Wound Care Products

The burn care market is witnessing a tremendous shift toward advanced wound care products, including hydrocolloid dressings, foam dressings, and bioengineered skin substitutes. These are developed to achieve faster healing times, minimal scarring, and lower infection risk than traditional dressings. Hydrocolloid dressings, for example, create an environment that allows tissue regeneration in a moist condition, while bioengineered skin substitutes resemble natural skin, thus ensuring better protection and complications. Studies have demonstrated that silver-containing dressings reduce infection rates in burn care by approximately 30-40%. The solutions have gained much popularity in hospital and homecare settings as increased awareness among the healthcare providers and patients regarding these solutions. Further, the increased incidence of burn injuries worldwide has also fueled demand for these innovative products. Advances in material science and biotechnology are also said to be influencing innovation in this area, with new products that will provide enhanced efficacy and ease of application, and thus, make the advanced wound care sector an important driver in expanding burn care market share.

Increased Focus on Burn Prevention Programs

Governments and healthcare organizations around the globe establish stringent prevention of burns through adequate training of communities on fire safety, first aid, and management of hazards at the workplace. According to the World Health Organization (WHO), an estimated 180,000 deaths annually are caused by burns, with most occurring in low- and middle-income countries. When targeting high-risk populations like children and industrial workers, campaigns encompass safe kitchen practices, the use of smoke alarms, and prevention and precautionary measures in hazardous environments. Industry reports reflect that these programs are significantly decreasing burn-related accidents, which promotes greater awareness and earlier medical attention when injuries do happen. Burn prevention promotion indirectly generates demand for products used in the care of burns because healthcare organizations prepare with necessary supplies in reserve. Organizations such as the World Health Organization (WHO) are highly involved in these activities, promoting uniform guidelines and availability of resources on burn prevention. This trend in priority towards prevention is also synchronizing with worldwide objectives of cost control in healthcare and betterment of patient outcomes, thereby elevating the burn care market demand.

Technological Advancements in Burn Treatments

Technological advancements in burn care technologies have changed the outlook for treatment and market scope. Recent advances such as stem cell therapies, 3D bioprinting, and tissue-engineered skin substitutes address many critical issues with the management of severe burns. Stem cell therapies possess regenerative potential that encourages rapid healing without leaving any noticeable scar on the skin. The development of customized grafts with the aid of 3D bioprinting can enhance acceptance rates in grafting, as well as diminish recovery times. Tissue-engineered solutions, made from biomaterials and cellular components, hold promise to offer a close reproduction of the structural and functional anatomy of natural skin. Industry reports indicate that some of the main players are placing significant investments into research and development in these sectors, thus helping to hasten the commercialization of high-end products. These advancements improve survival rates but also enhance the quality of life for burn victims, which gives a strong burn care market growth trajectory in the coming years.

Burn Care Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global burn care market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on facility type, treatment type, burn severity, and service type.

Analysis by Facility Type:

- In-house

- Standalone

In-house facilities dominate the global burn care market due to their comprehensive treatment capabilities and access to specialized medical resources. These facilities, including hospitals and advanced burn centers, offer integrated services such as emergency response, wound management, surgical interventions, and rehabilitation. Their ability to handle severe and complex burn cases ensures patient safety and optimal outcomes, making them the preferred choice for critical care. Additionally, in-house facilities often incorporate multidisciplinary teams comprising surgeons, wound care specialists, and physical therapists, providing a continuum of care under one roof. The increasing prevalence of burns, particularly in industrial and domestic settings, has amplified the need for well-equipped facilities. Furthermore, advancements in medical infrastructure and the implementation of government initiatives to improve healthcare accessibility are strengthening the role of in-house facilities as the primary segment by facility type in the global burn care market.

Analysis by Treatment Type:

- Wound Debridement

- Skin Graft

- Traction, Splints and Wound Care

- Respiratory Intubation and Ventilation

- OTC Pain Medications and Bandages

- Blood Transfusion

- Prophylactic Vaccinations and Inoculations

- Rehabilitation

Wound debridement holds the largest share in the burn care market by treatment type due to its critical role in managing burn injuries effectively. Debridement involves the removal of necrotic or damaged tissue, preventing infection and promoting faster healing. This treatment is particularly essential for moderate to severe burns, where dead tissue can hinder recovery and increase the risk of complications. Innovations in debridement techniques, such as enzymatic agents and hydro-surgical technologies, have further boosted its adoption. Moreover, healthcare providers emphasize this treatment as an initial and ongoing procedure in burn management protocols, ensuring a clean wound bed for subsequent therapies. Furthermore, the increasing awareness of advanced wound care products and growing investments in research and development are also driving the prominence of debridement in burn care. Its indispensable role in recovery positions it as a cornerstone treatment type in the market.

Analysis by Burn Severity:

- Minor Burns

- Partial Thickness Burns

- Full Thickness Burns

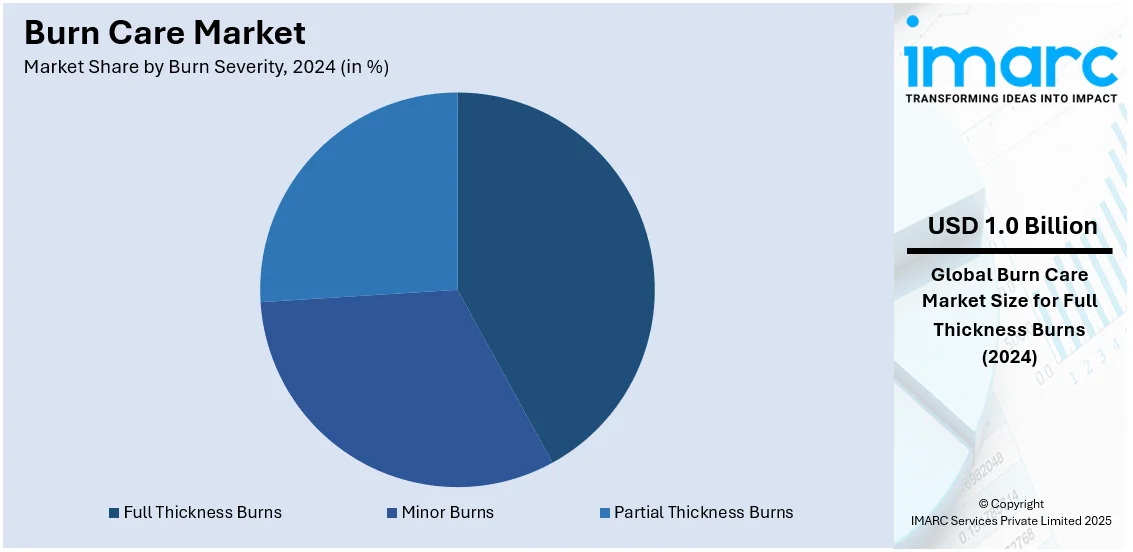

Full thickness burns lead the market with around 41.7% of market share in 2024, due to the extensive medical attention they require. These burns penetrate all layers of the skin, often necessitating complex treatments such as skin grafts, reconstructive surgery, and intensive wound care. Their severity leads to prolonged hospital stays and higher treatment costs, contributing significantly to market revenue. Specialized care, including pain management and rehabilitation, is essential for these cases, further emphasizing their economic and clinical impact. The rising incidence of severe burn injuries in industrial and residential settings has heightened the demand for advanced treatment solutions. Moreover, technological advancements in synthetic skin substitutes and bioengineered grafts are supporting improved outcomes for full-thickness burn patients. This segment’s complexity and demand for comprehensive care underscore its leading position by burn severity in the market.

Analysis by Service Type:

- Burns Inpatient

- Outpatient

- Rehabilitation

Burns inpatient services account for the largest share in the global burn care market by service type, owing to the intensive and prolonged care required for severe burn injuries. Inpatient care ensures round-the-clock monitoring, pain management, and access to advanced treatments, such as surgical interventions and infection control measures. The increasing number of severe burn cases requiring hospitalization, coupled with advancements in critical care infrastructure, has propelled this segment’s growth. Comprehensive inpatient services often include multidisciplinary approaches involving surgeons, physical therapists, and psychologists, addressing both physical and psychological recovery. Furthermore, the growing prevalence of severe burns in industrial and domestic settings underscores the need for specialized inpatient care. With healthcare providers increasingly focusing on improving patient outcomes and reducing mortality rates, the demand for dedicated inpatient burn care facilities continues to rise, solidifying their leading position in this market segment.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 52.0%. North America holds the largest share of the global burn care market, driven by advanced healthcare infrastructure, high awareness of burn care treatments, and substantial investment in research and development. The region benefits from the presence of leading manufacturers offering innovative wound care products, including dressings, skin substitutes, and surgical tools. The United States, as a major contributor, has a high prevalence of burn injuries and well-established burn centers, ensuring access to specialized care. For instance, as per industries reports, burn care addresses around 450,000 burn injuries annually in the U.S., resulting in approximately 45,000 hospitalizations. Favorable reimbursement policies and strong support from government initiatives further bolster market growth. In addition to this, the region’s focus on technological advancements and clinical studies has led to improved treatment outcomes, reinforcing North America's dominant position in the global burn care market.

Key Regional Takeaways:

United States Burn Care Market Analysis

The US burn care market is registering growth steadily owing to the prevalence of burn injuries increasing day after day and increasing better treatment alternatives. The American Burn Association reveals that about 450,000 people in the United States require annual treatment of their burn injuries while 40,000 receive medical attention since the injuries they sustain are considered major. The high prevalence of burns cases in industry and household accidents is raising the demand for effective burn care products. Rapid innovation in wound care technologies, including advanced dressings, skin substitutes, and regenerative medicine, is enhancing treatment outcomes among burn victims, thus stimulating market demand. In addition, the establishment of specialized burn centers and government funding for burn care programs, such as resource allocation to the National Institutes of Health for conducting burn research, contribute to market growth. Key market players, including Smith & Nephew, Mölnlycke Health Care, and 3M, continue to invest in R&D, which ensures continuous development and availability of cutting-edge solutions for burn care.

Europe Burn Care Market Analysis

The European burn care market is registering growth due to increased cases of burn injuries as well as availability of specialized care. A systemic review published in *Burns* journal shows that the average incidence of serious burns in Europe annually ranges between 0.2 to 2.9 per 10,000 inhabitants, where there is an indication of a reduction with time. This means 100,000 to 150,000 annual cases of severe burns in Europe. Advances in regenerative medicine, such as skin grafts and tissue engineering, are also supporting the market. Germany is a leader in research and development. The European market is also shifting toward more sustainable, bioactive dressings for wound healing. The European Burn Association puts emphasis on burn prevention while indicating that those injuries caused through burns, fires, and flames are the fourth leading injury death cause of people aged 65 years old and above, although they accounted for less than 5 percent of all kinds of injuries. With new government-backed policies introduced for the improvement of burn care services, as well as tie-ups between local manufacturers and companies around the world, market growth seems inevitable. Innovations in the formation of novel burn management solutions have led European manufacturers to take center stage in capturing the global markets.

Asia Pacific Burn Care Market Analysis

The market for burn care is growing rapidly in the Asia Pacific primarily due to the rising cases of burns injuries and higher levels of awareness among people about advanced treatment methods. According to the World Health Organization, Asia has a huge share of global burn injuries, with countries such as India, China, and Indonesia having very high numbers. By 2023, national general public budget expenditure in China had risen to about RMB 28.2 trillion (USD 4 trillion), of which the health sector accounted for a sum of approximately RMB 2.239 trillion (USD 320 billion), as per reports. Such investments are critical to the development of healthcare infrastructure that includes burn care centers and more specialized treatment modalities. Finally, the market also benefits from new products that involve advanced burn care products, like biological dressings and synthetic skin substitutes. Furthermore, growing disposable incomes in the region are increasing accessibility to quality treatments. R&D spends with global company investments from the likes of Johnson & Johnson and 3M would increase market prospects. Improving accessibility to care and betterment of treatment standards would increase the demand for burn care solutions over time.

Japan Burn Care Market Analysis

Japan's burn care market is accelerating because of the advances in technology, geriatric population, and boosting investment in specialized wound care. The country's well-established healthcare system ensures access to advanced burn treatments, including biologic dressings, negative pressure wound therapy (NPWT), and bioengineered skin substitutes.

Regenerative medicine and tissue engineering have focused the attention of Japan on great developments in the skin grafting technique. In stem cell therapy and collagen-based wound healing products, research has been accelerating innovations in burn care. The government is supporting initiatives in wound healing and reconstructive surgery, both for acute and chronic burn patients. Despite these developments, high treatment costs and a relatively smaller burn incidence rate compared to other Asian markets limit widespread market growth. However, the increasing adoption of home-based wound care solutions and technological integration in hospital burn units continue to support market expansion.

China Burn Care Market Analysis

Improving healthcare infrastructure, escalating levels of disposable income, and advances in wound care technologies are further fueling the burn care market in China. The incidence of burn injuries is rather high in industrial as well as domestic settings and hence continues to spur a strong demand for innovative treatments to burns. The support of the government towards specialized burn centers and regenerative medicine research is giving impetus to skin substitutes, bioengineered grafts, and hydrogel-based wound dressings. The pharmaceutical and biotechnology sectors in China are also engaging in active investments in stem cell therapy and tissue engineering solutions that improve burn recovery.

This market is likely to benefit from greater awareness of burn prevention and first-aid care and rising adoption of AI-based wound assessment tools. Strategic partnerships between global and domestic manufacturers of wound care will further accelerate technological advancement and availability.

India Burn Care Market Analysis

India's burn care market is intensifying due to of the high rate of burns incidence, amplifying healthcare awareness, and new medical treatments. The country annually reports a significant number of burn injuries, mostly in rural areas, where specialized care access is still low. Advanced wound care products, including hydrocolloid dressings, skin grafts, and silver-based antimicrobial products, are the primary demand shaping the market.

Government programs, such as Ayushman Bharat and state-level burn treatment programs are improving access to affordable burn care. Private healthcare sector and burn centers are investing in modern ways of treatments, laser therapy, and skin substitutes to improve patient outcomes. However, problems with financial availability and infrastructural inadequacies in the hospital facilities of the rural setup are the prime factors. The rising multinational wound care companies with the heightening awareness regarding burn first aid and treatment protocols is also expected to encourage further growth in the industry of burn care in India.

Latin America Burn Care Market Analysis

The Latin America burn care market is on an expansion, thanks to the relatively high rate of burn injuries within the region as well as higher investments in the healthcare sector. According to WHO, the estimated global deaths by burn are 180,000 yearly with most being within the low-and middle-income economies, a high number in most countries in the region. Burn injuries form a major proportion of trauma casualties in Brazil. An estimated 2 million accidents and 2,500 deaths occur each year, and a lot is in dire need to be done through effective burn care solutions. It is reported that the region, including Brazil, which leads, as well as Mexico and Argentina, focuses on burn center improvements. The government-backed initiatives along with partnerships with multi-national companies are introducing innovative products such as bioengineered skin and advanced wound dressings that are improving treatment outcomes. These developments, along with ever increasing spending on health care, establish Latin America as an emerging market for burn care products and services.

Middle East and Africa Burn Care Market Analysis

This regional market for burns care is moving gradually due to increased investment in healthcare infrastructure in the region along with the upsurge incidence rate of burn injury. In the year 2023, it was reported by Sheikh Shakhbout Medical City (SSMC) in United Arab Emirates, that 263 patients were given treatment for suffering from burn injury. Countries like Saudi Arabia and South Africa are also pushing for specialized burn care units while increasing the delivery of more refined therapies, which include bioengineered skin substitutes and advanced wound care products. The region's challenges also included limited healthcare access in rural setups, thus significantly affecting the quick management of burns cases. However, government-led initiative and international support from healthcare providers seem to fill that gap. Advances in burn care technology, along with a focus on education and prevention programs, will drive the market even more in the future.

Kuwait Burn Care Market Analysis

The burn care market in Kuwait is growing due to government healthcare investments, rising awareness of advanced wound care, and increasing cases of burn injuries. The country's healthcare sector is well-developed, with specialized burn units and modern treatment facilities in leading hospitals. The Ministry of Health initiatives are on improving the accessibility of burn treatment and emergency care. High adoption of biologic dressings, antimicrobial hydrocolloids, and laser therapy is driving market expansion. The prevalence of occupational burn injuries in the oil and gas sector is also amplifying demand for specialized burn treatments.

Competitive Landscape:

The global burn care industry is intensely competitive, with leading companies prioritizing innovation, forging strategic partnerships, and broadening their product ranges to enhance their market positioning. Companies such as Smith & Nephew, Mölnlycke Health Care, and 3M dominate the market through advanced wound care solutions and robust distribution networks. For instance, in the third quarter, Smith & Nephew reported a revenue of USD 1,412 million, a 4.0% increase from USD 1,357 million in Q3 2023. The company expects a notable rise in its trading profit margin by 2025, aiming for a range of 19.0% to 20.0%. The market also sees active participation from regional players offering cost-effective alternatives, catering to local demand. Rising investments in research and development have resulted in the launch of innovative products, such as hydrogel dressings, biological skin substitutes, and antimicrobial therapies. Additionally, partnerships between manufacturers and healthcare providers enhance access to advanced burn care solutions, further intensifying competition within this rapidly growing market.

The report provides a comprehensive analysis of the competitive landscape in the burn care market with detailed profiles of all major companies, including:

- Burn and Reconstructive Centers of America

- Chelsea & Westminster Hospital

- National Burn Center (India)

- North Bristol NHS Trust

- Pediatric Burn Care Center (The General Hospital Corporation)

- The MetroHealth System

- University of Rochester Medical Center

- University of Washington.

Latest News and Developments:

- October 2024: South West burns specialists report an increase in hot drink scalds among children. In 2023, there were 149 cases, while over the past decade, the figure was 1,830. National Burn Awareness Day focuses on prevention and appropriate first aid, particularly for hot water bottle injuries, which increased by 43% during the last winters.

- August 2024: A study in Rehabilitation Psychology analyzing 939 burn patients identifies three recovery trajectories—recovering, static, and weakened—highlighting the need for early screening and intensive rehabilitation for low HRQOL cases.

- November 2023: MetroHealth's Comprehensive Burn Care Center recently achieved re-verification by the American Burn Association as an adult and pediatric burn center through October 2026. The center is known to provide the best care possible, taking on approximately 1,700+ new burn injuries every year, providing burn education for first responders, and offering extensive patient and community support.

Burn Care Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Facility Types Covered | In-house, Standalone |

| Treatment Types Covered | Wound Debridement, Skin Graft, Traction, Splints and Wound Care, Respiratory Intubation and Ventilation, OTC Pain Medications and Bandages, Blood Transfusion, Prophylactic, Vaccinations and Inoculations, Rehabilitation |

| Burn Severities Covered | Minor Burns, Partial Thickness Burns, Full Thickness Burns |

| Service Types Covered | Inpatient, Outpatient, Rehabilitation |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Burn and Reconstructive Centers of America, Chelsea & Westminster Hospital, National Burn Center (India), North Bristol NHS Trust, Pediatric Burn Care Center (The General Hospital Corporation), The MetroHealth System, University of Rochester Medical Center, University of Washington, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the burn care market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global burn care market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the burn care industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The burn care market was valued at USD 2.5 Billion in 2024.

IMARC estimates the burn care market to reach USD 4.0 Billion by 2033, exhibiting a CAGR of 5.2% during 2025-2033.

The market is driven by the magnifying cases of burn injuries, escalating awareness regarding advanced wound management, proliferating need for enhanced products encompassing bioengineered skin substitutes, and resilient government aid through reimbursement policies and ventures. Innovations in treatment methodologies further facilitate market expansion.

The global burn care market report covers primary segments including facility type, treatment type, burn severity, and service type, providing a comprehensive analysis of market dynamics and treatment advancements.

North America currently dominates the burn care market, accounting for a share exceeding 52.0%. This dominance is fueled by its well-structured healthcare infrastructure, elevated awareness, and heavy investment in leading-edge treatments.

Some of the major players in the burn care market include Burn and Reconstructive Centers of America, Chelsea & Westminster Hospital, National Burn Center (India), North Bristol NHS Trust, Pediatric Burn Care Center (The General Hospital Corporation), The MetroHealth System, University of Rochester Medical Center, University of Washington, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)