Brazil Data Center Market Size, Share, Trends and Forecast by Data Center Size, Tier Type, Absorption, and Region 2026-2034

Brazil Data Center Market Size, Share, Trends & Forecast (2026-2034)

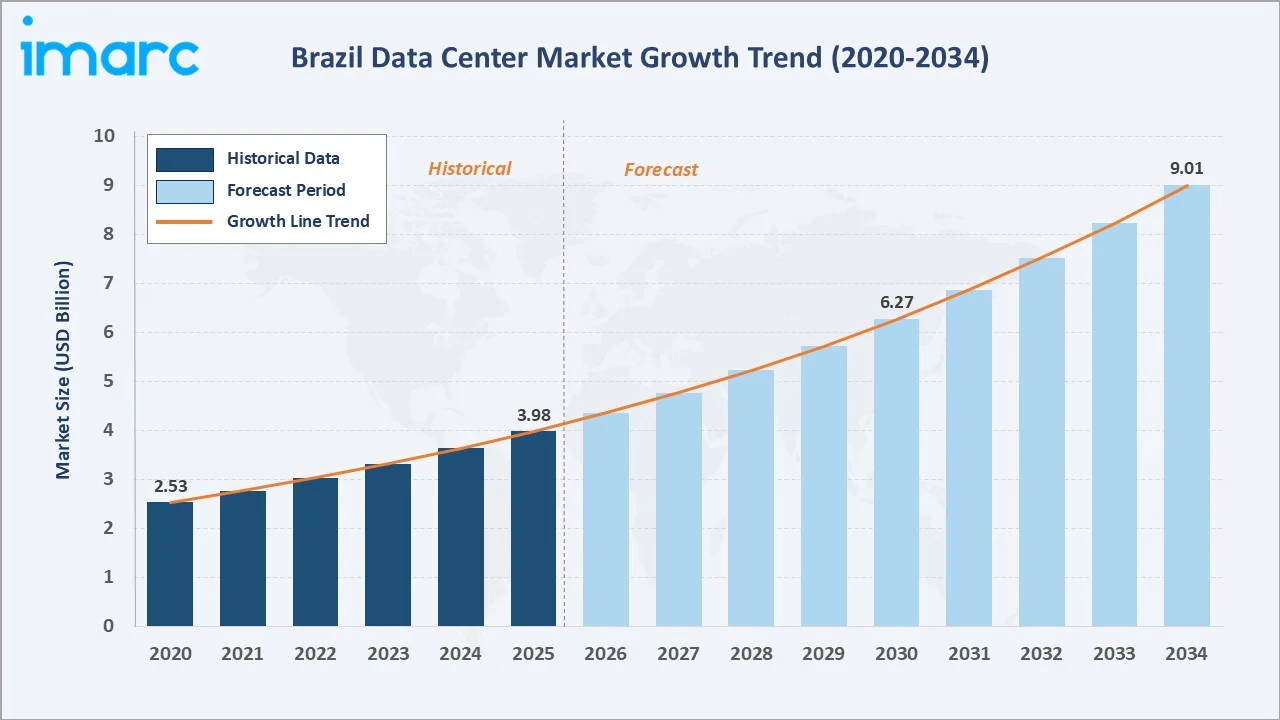

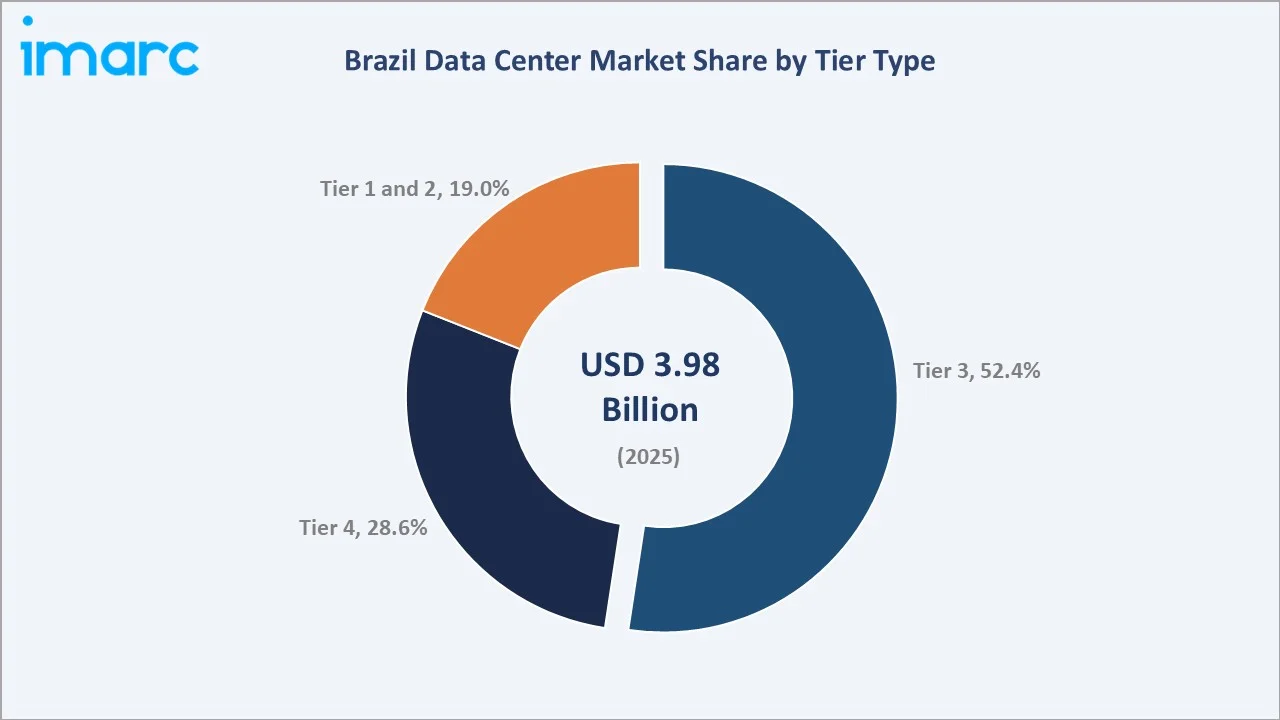

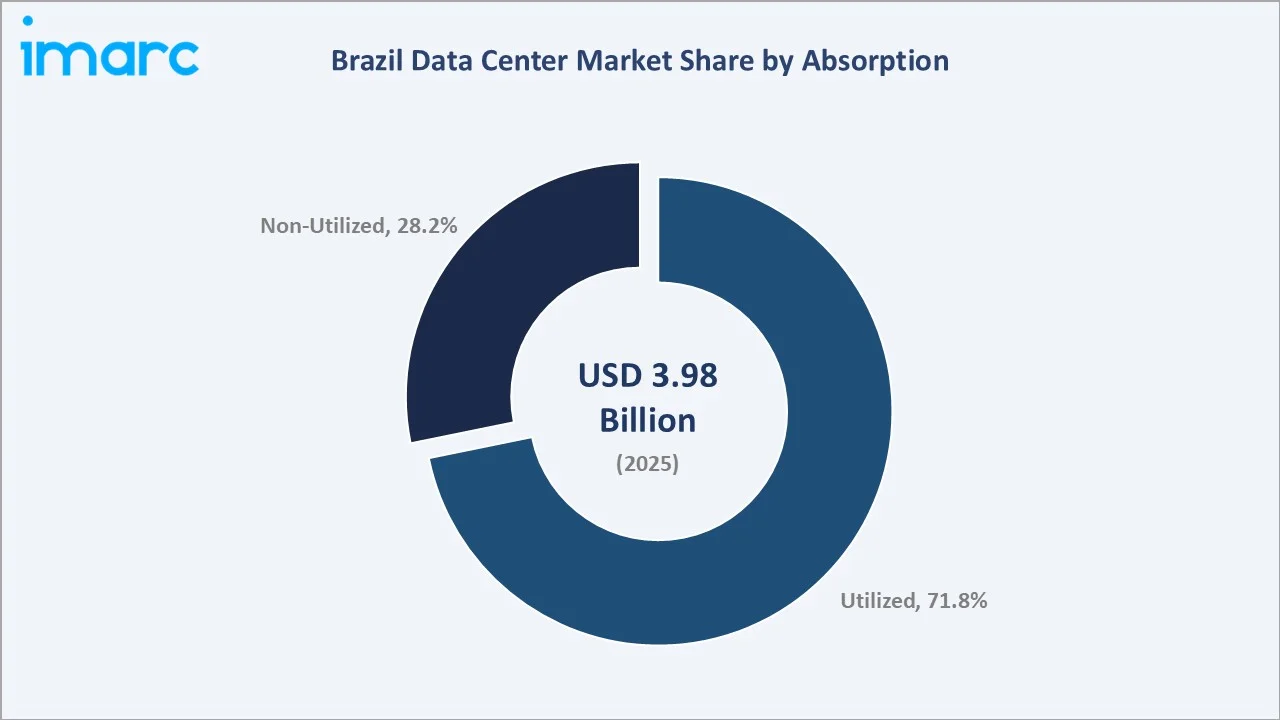

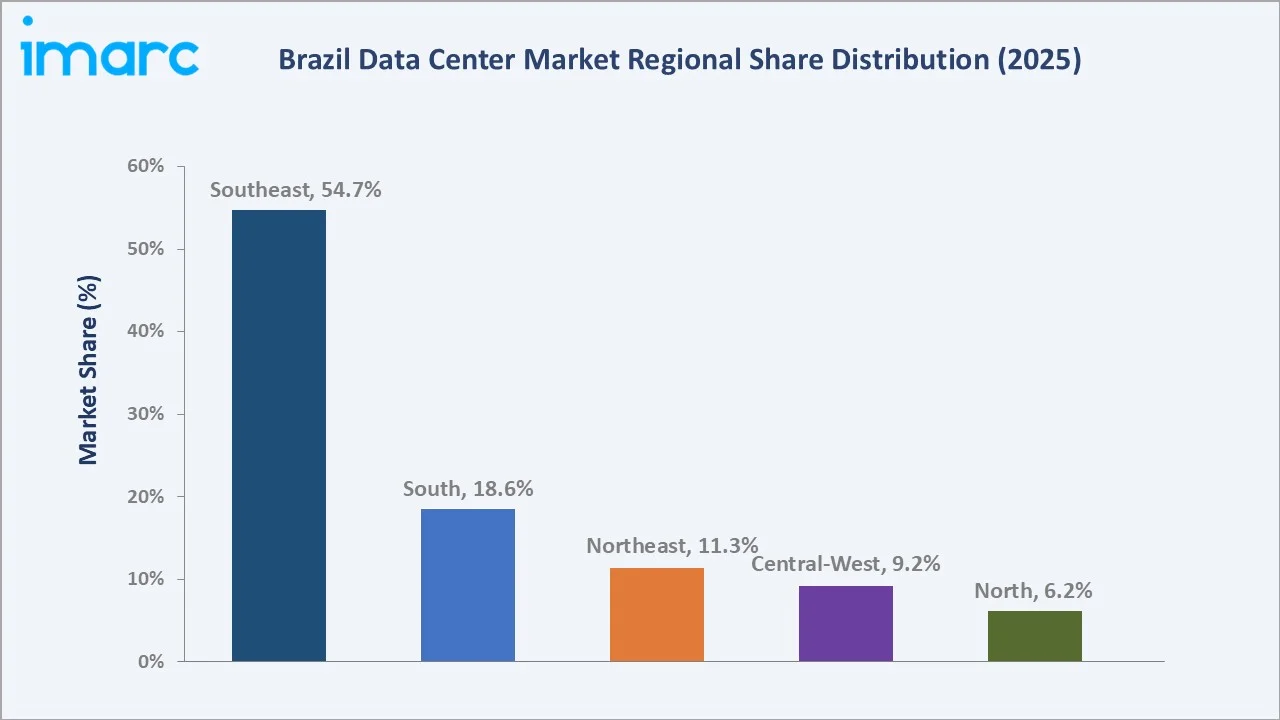

The Brazil data center market size was valued at USD 3.98 Billion in 2025 and is projected to reach USD 9.01 Billion by 2034, exhibiting a CAGR of 9.50% during the forecast period 2026-2034. Surging cloud adoption among Brazilian enterprises, rapid fintech and e-commerce expansion, the rollout of 5G networks in over 450 cities by the end of 2025, and accelerated hyperscaler investment from AWS, Microsoft Azure, and Google Cloud are driving the Brazil data center market growth. Tier 3 leads the tier type segment at 52.4% in 2025, while Utilised capacity dominates the absorption segment at 71.8%. The Southeast region accounts for 54.7% of national revenue in 2025, anchored by São Paulo's position as Latin America's largest interconnection hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.98 Billion |

|

Forecast Market Size (2034) |

USD 9.01 Billion |

|

CAGR (2026-2034) |

9.50% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (54.7% share, 2025) |

|

Fastest Growing Region |

Northeast (CAGR ~11.8%) |

|

Leading Tier Type |

Tier 3 (52.4%, 2025) |

|

Leading Absorption |

Utilized (71.8%, 2025) |

To get more information on this market, Request Sample

The Brazil data center market growth trajectory from 2020 through 2034, expressed in USD Billion, reflects consistent historical capacity build-out followed by a sharply steeper forecast curve powered by hyperscaler investment, submarine cable landings, and accelerating enterprise cloud migration.

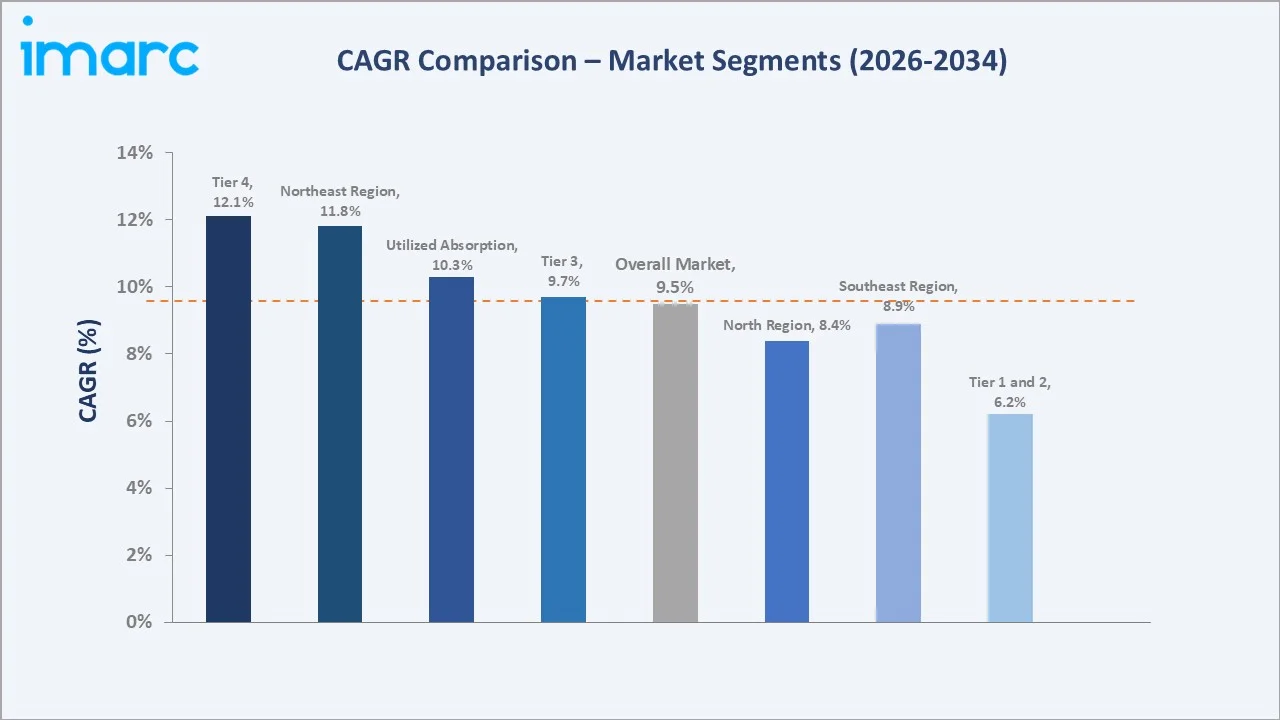

Segment-level CAGR comparisons highlight Tier 4 facilities and the Northeast region as the fastest-expanding sub-categories within the Brazil data center industry analysis through 2034.

Executive Summary

The Brazil data center market is undergoing a structural shift driven by hyperscaler investment, sovereign cloud demand, and accelerating enterprise digitalization. Valued at USD 3.98 Billion in 2025, the market is forecast to reach USD 9.01 Billion by 2034 at a CAGR of 9.50%.

Tier 3 commands the dominant tier share at 52.4% in 2025, driven by colocation providers supporting mid-to-large enterprise workloads. Tier 4 holds 28.6% and is the fastest-expanding tier, fuelled by banking and hyperscale cloud regions. Utilized capacity dominates at 71.8% in 2025, underscoring tight supply across São Paulo and Rio de Janeiro metros.

The Southeast leads with 54.7% national revenue share in 2025, anchored by São Paulo's Tamboré and Barueri corridors, which host Latin America's largest interconnection concentration. South (18.6%) and Northeast (11.3%) follow, with Fortaleza's subsea cable landings linking Brazil directly to Europe and Africa.

Key Market Insights

|

Insight |

Data |

|

Largest Tier Type |

Tier 3 - 52.4% share (2025) |

|

Leading Absorption Type |

Utilized - 71.8% share (2025) |

|

Leading Region |

Southeast - 54.7% revenue share (2025) |

|

Second Region |

South - 18.6% revenue share (2025) |

|

Top Companies |

Ascenty, Equinix Inc., Scala Data Centers, Cirion Technologies, EdgeUno, HostDime Global Corp., and Quântico Data Center |

Key analytical observations supporting the above data are summarized below.

- Tier 3 Leadership: Tier 3's 52.4% dominance in 2025 reflects industry-wide preference for concurrently maintainable facilities delivering 99.982% uptime for enterprise colocation and cloud on-ramp workloads.

- Supply Constraint: Utilized capacity at 71.8% signals a structurally tight market where newly commissioned megawatts are absorbed within 12-18 months, particularly in São Paulo.

- Regional Concentration: The Southeast's 54.7% share is anchored by São Paulo metro, which alone hosts over 500 MW of installed IT capacity and Brazil's primary cloud availability zone.

- Hyperscaler Pipeline: Hyperscaler leasing accelerated in 2024-2025, with AWS, Azure, Google Cloud, and Oracle collectively expanding Brazilian capacity by over 350 MW of pre-leased commitments.

- Tier 4 Momentum: Tier 4 at 28.6% in 2025 is the fastest-growing tier, driven by banking fault-tolerance requirements and hyperscale build-to-suit campuses above 100 MW.

Brazil Data Center Market Overview

Data centers in Brazil are purpose-built facilities housing servers, storage, network equipment, and power-cooling infrastructure that underpin the country's digital economy. They support cloud services, financial transaction processing, streaming, e-commerce, enterprise IT, and increasingly AI inference workloads for Latin America.

Applications span banking and payments, telecom, government digitalization, retail e-commerce, media, healthcare, and industrial IoT platforms. Brazil's position as Latin America's largest economy and its LGPD regulatory framework make it the preferred onshore hub for regional data residency.

Macroeconomic enablers include a population above 215 million, internet penetration, mobile broadband subscriptions, and a federal push toward digital public services under the Gov.br platform.

Market Dynamics

To evaluate market opportunities, Request Sample

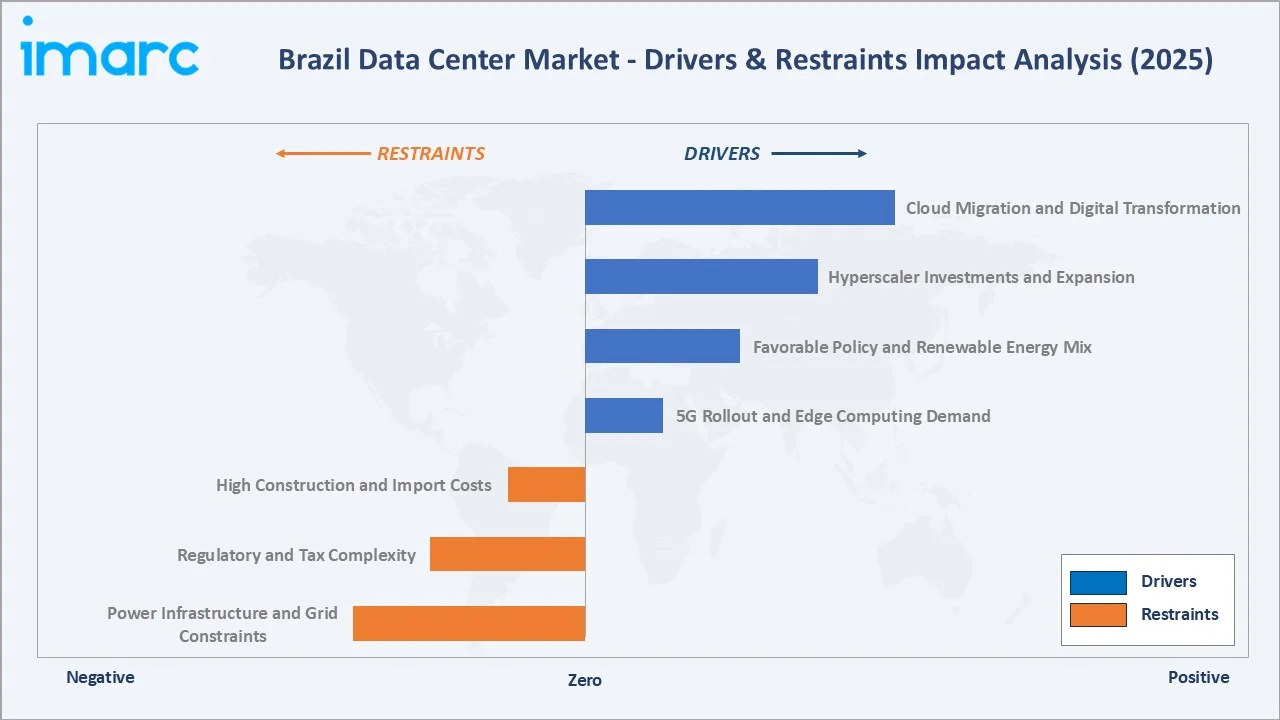

Market Drivers

- Hyperscale Cloud Adoption: AWS, Azure, and Google Cloud all operate São Paulo regions, collectively expanding capacity by over 300 MW in 2024 to absorb Brazilian enterprise cloud migration.

- Digital Payments & Fintech: The Central Bank's PIX platform processed over 64 billion transactions in 2024 while Nubank crossed 100 million customers, pushing workloads onshore.

- 5G Rollout: Anatel reported 5G coverage across 452 Brazilian cities by September 2024, creating edge compute demand in tier-2 urban centers.

- Data Sovereignty: LGPD enforcement by the ANPD has raised cross-border data transfer costs, favouring onshore colocation and sovereign cloud deployments.

Market Restraints

- Power Cost Pressure: Brazilian industrial power tariffs rank among the highest in the Americas, with São Paulo averaging USD 0.11-0.13 per kWh in 2024.

- Permitting Delays: Permitting timelines for new São Paulo campuses frequently exceed 18-24 months, slowing greenfield supply additions.

- Currency Volatility: BRL volatility against the USD complicates equipment procurement and investor return modelling for foreign capital.

Market Opportunities

- AI Infrastructure: Brazilian banks, retailers, and government agencies are piloting LLM-based applications requiring high-density GPU colocation with liquid cooling readiness.

- Edge & Tier-2 Cities: Secondary metros, including Fortaleza, Recife, Porto Alegre, and Brasília, offer lower land and power costs than São Paulo.

- Subsea Cable Hubs: Fortaleza's EllaLink, Monet, and South Atlantic Cable System landings create opportunity for international connectivity-anchored campuses.

Market Challenges

- Talent Shortages: Specialist data center talent, including critical facility engineers and high-voltage electricians, remains scarce in Brazil, raising execution risk.

- Water Stress: Water-cooled facilities face scrutiny in drought-affected Southeast regions, pushing operators toward air-cooled and evaporative designs.

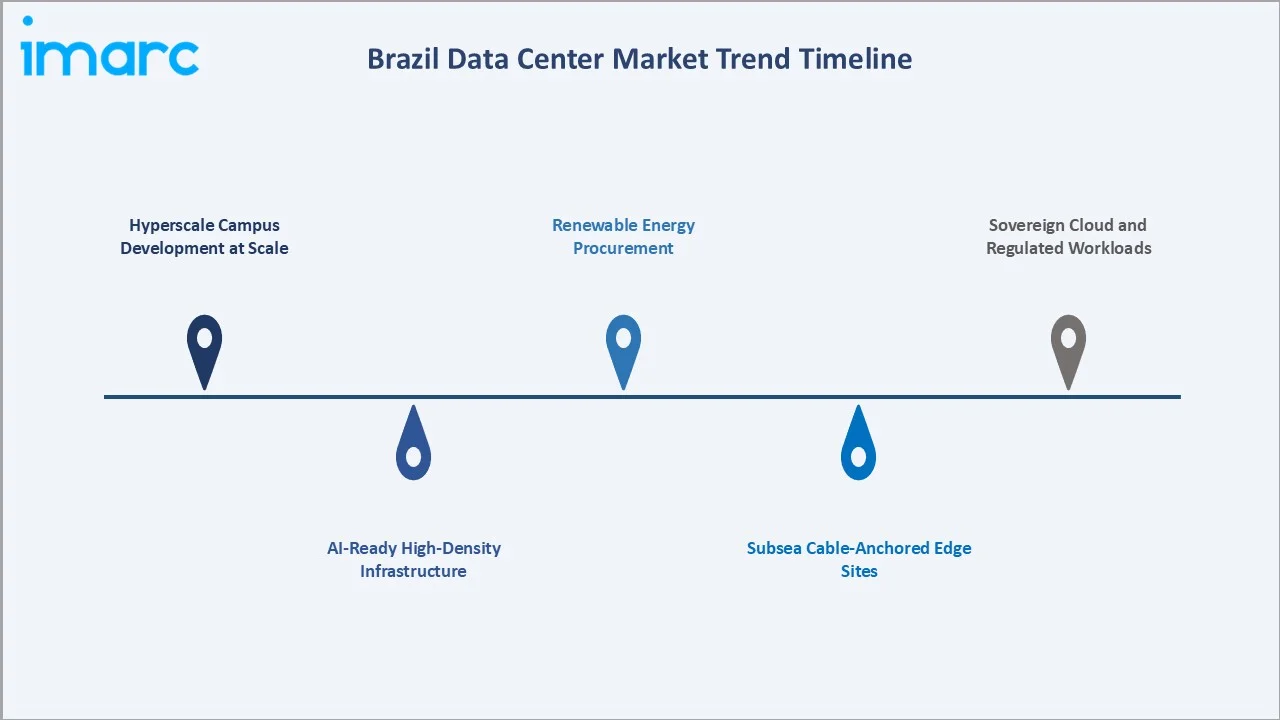

Emerging Market Trends

1. Hyperscale Campus Development at Scale

Brazilian data center inventory is shifting from sub-20 MW retail colocation to 50-200 MW hyperscale campuses. Scala announced a 4.7 GW buildout plan in 2024, while ODATA and Ascenty each commissioned campuses exceeding 60 MW in the São Paulo metro.

2. AI-Ready High-Density Infrastructure

Rack power densities above 40 kW are becoming standard for AI-inference colocation deployments. Liquid cooling adoption is accelerating, with Equinix, Scala, and Ascenty introducing liquid-to-chip and rear-door heat exchanger offerings in 2024-2025.

3. Renewable Energy Procurement

Brazilian operators are aggressively contracting wind and solar PPAs to meet hyperscaler sustainability mandates. Scala operates on 100% renewable energy, while Ascenty signed multi-hundred-MW solar PPAs in 2024.

4. Subsea Cable-Anchored Edge Sites

Fortaleza's emergence as the primary Brazilian trans-Atlantic cable landing hub, supporting EllaLink and Monet systems, is driving new interconnection-focused data center builds in Ceará state.

5. Sovereign Cloud and Regulated Workloads

Public sector digitalization under Gov.br, combined with BACEN Resolution 4893 cybersecurity requirements, is creating a durable sovereign cloud workload layer anchored in Brazilian Tier 3 and Tier 4 facilities.

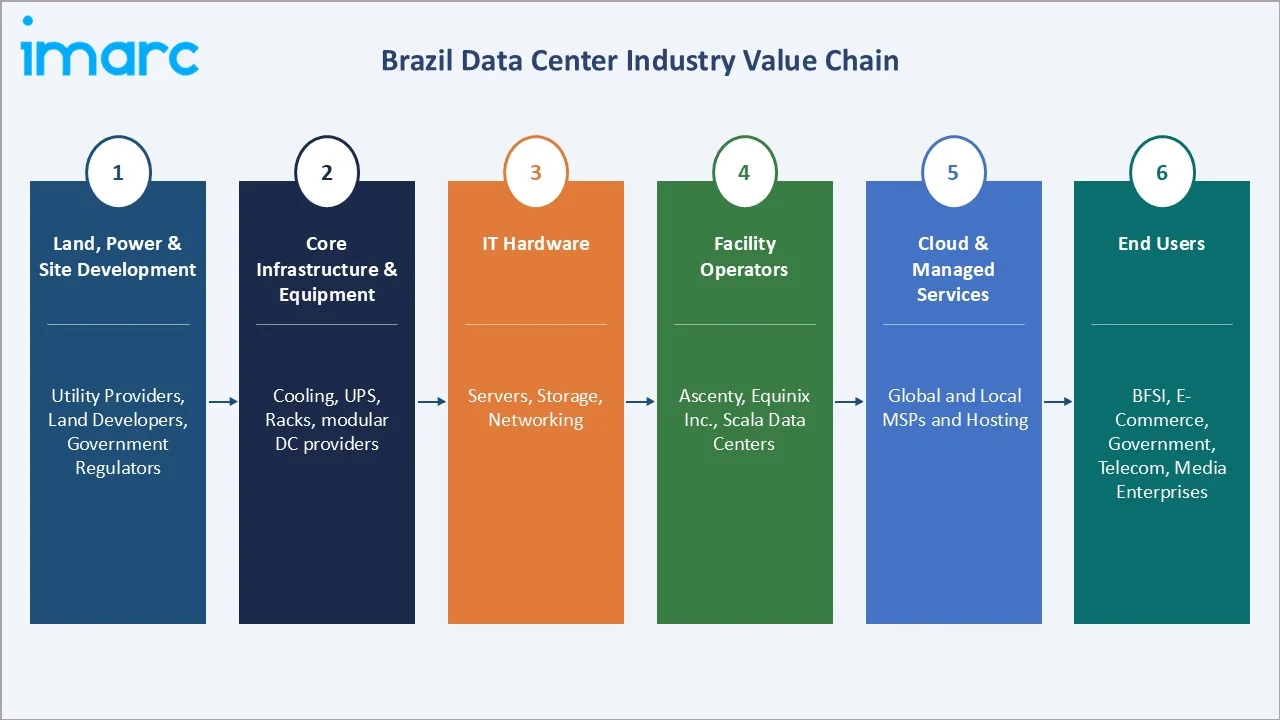

Industry Value Chain Analysis

The Brazil data center value chain spans five integrated stages from infrastructure supply through end-user service delivery. Each stage carries distinct margin profiles and competitive dynamics within the broader Brazil data center industry analysis.

|

Stage |

Key Players / Examples |

|

Infrastructure & Equipment |

Supply power, cooling, and mechanical systems |

|

Design, Build & Engineering |

Manage construction and commissioning. |

|

Colocation & Wholesale |

Own and lease data center capacity. |

|

Cloud & Managed Services |

Deliver compute and software as a service. |

|

End Users |

Consume capacity for workloads and compliance. |

Colocation and wholesale operators occupy the highest-value position in the Brazilian chain, capturing long-duration lease contracts from hyperscalers while retaining retail enterprise customers at higher margins.

Technology Landscape in the Brazil Data Center Industry

Power Infrastructure and Renewable Integration

Brazilian facilities increasingly deploy medium-voltage UPS systems, lithium-ion battery storage, and direct renewable PPAs. Scala and Ascenty lead in sourcing 100% renewable energy, reflecting hyperscaler sustainability mandates from 2023 onward.

Advanced Cooling Systems

Rising rack densities are pushing operators from CRAC/CRAH chilled water designs toward rear-door heat exchangers, direct-to-chip liquid cooling, and immersion cooling. Equinix and Scala launched liquid cooling offerings in 2024 for AI workloads.

Connectivity and Interconnection Fabrics

Brazilian Tier 3 and Tier 4 facilities are increasingly interconnected via cloud exchange fabrics such as Equinix Fabric and Ascenty Connect, enabling direct private connectivity to AWS, Azure, Google Cloud, and Oracle Cloud regions.

Automation, DCIM, and AIOps

DCIM platforms combined with AI-driven operations tooling are reducing unplanned downtime and optimizing PUE. Brazilian operators report PUE improvements from 1.7 toward 1.35-1.45 across newer builds commissioned in 2023-2025.

Market Segmentation Analysis

By Tier Type

To access detailed market analysis, Request Sample

Tier 3 commands a 52.4% majority share in 2025, reflecting its position as the sweet spot for Brazilian enterprise colocation. Concurrently maintainable infrastructure with N+1 redundancy delivers 99.982% uptime at attractive price points relative to Tier 4.

Tier 4 holds 28.6% in 2025, driven by mission-critical banking workloads from Itaú, Bradesco, Santander Brasil, and Banco do Brasil, plus hyperscaler build-to-suit campuses where 2N redundancy is mandatory.

Tier 1 and 2 collectively account for 19.0% in 2025, concentrated in smaller enterprises on-premise deployments, tier-2 city regional facilities, and legacy telco central offices that have not been upgraded.

By Absorption

Utilized capacity dominates at 71.8% in 2025, signalling one of the tightest absorption rates in the Americas. São Paulo metro in particular operates above 85% utilization, with newly commissioned megawatts absorbed within 12-18 months of delivery.

Non-Utilized capacity at 28.2% in 2025 largely represents pre-leased or ramp-phase inventory in new hyperscale campuses that will convert to utilized within 24 months of energization, based on binding offtake agreements.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

54.7% |

São Paulo cloud region, fintech density, and interconnection hub |

|

South |

18.6% |

Agribusiness IT, manufacturing workloads, Porto Alegre edge sites |

|

Northeast |

11.3% |

Fortaleza subsea cables, lower power costs, and federal incentives |

|

Central-West |

9.2% |

Brasília government workloads, sovereign cloud, Gov.br demand |

|

North |

6.2% |

Manaus free-trade zone, industrial IoT, edge telecom |

The Southeast commands 54.7% of national revenue in 2025. São Paulo state anchors the region, with over 500 MW of installed IT capacity concentrated in Tamboré, Barueri, and Santana de Parnaíba. Rio de Janeiro adds media, energy, and federal workloads.

South

The South holds 18.6% in 2025, supported by Porto Alegre, Curitiba, and Florianópolis. The region serves manufacturing clusters in Paraná and Santa Catarina, agribusiness in Rio Grande do Sul, and edge connectivity for Mercosur commerce flows.

Northeast

The Northeast accounts for 11.3% in 2025and is the fastest-growing region at an estimated CAGR of 11.8%. Fortaleza's subsea cable landings and lower industrial power tariffs drive international connectivity-anchored builds.

Central-West

The Central-West holds 9.2% in 2025, led by Brasília. Federal government digitalization under Gov. BR, sovereign cloud mandates, and proximity to ministerial clients drive Tier 3 and Tier 4 capacity additions in the region.

North

The North represents 6.2% in 2025, concentrated in Manaus within the Zona Franca free-trade zone. Industrial IoT from electronics manufacturing and telecom edge deployments for the Amazon region drives localized data center demand.

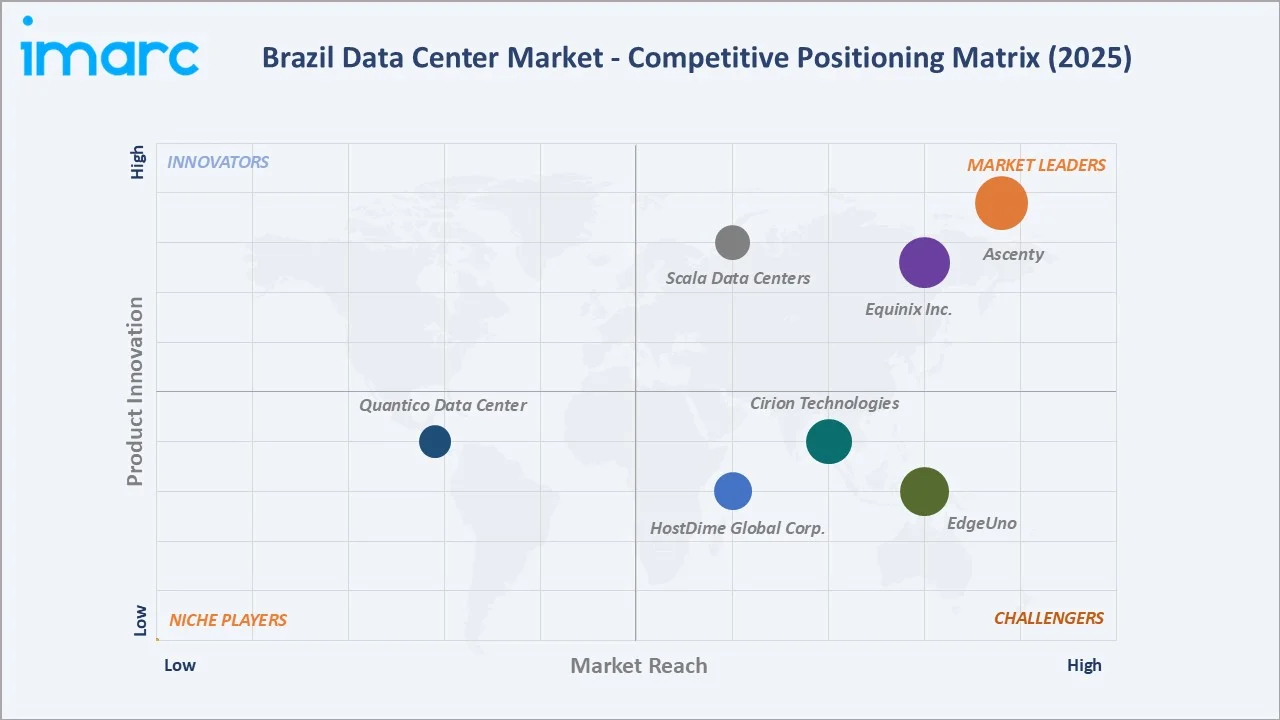

Competitive Landscape

|

Company Name |

Key Platform / Offerings |

Market Position |

Core Strength |

|

Ascenty |

Data Centers Ascenty |

Leader |

Largest national footprint, Digital Realty backing |

|

Equinix Inc. |

Equinix IBX data centers |

Leader |

Global interconnection, cloud on-ramps |

|

Scala Data Centers |

Data Centers |

Leader |

100% renewable, 4.7 GW pipeline |

|

Cirion Technologies |

SAO1 (São Paulo), RIO1 (Rio de Janeiro), and CUR1 (Curitiba)) |

Challenger |

Network-rich facilities, CDN, SD-WAN |

|

EdgeUno |

Data Centers |

Challenger |

Edge colocation, LATAM-wide |

|

HostDime Global Corp. |

Brazil Data Center |

Challenger |

Dedicated hosting, SMB colocation |

|

Quântico Data Center |

Quântico Data Center |

Emerging |

Regional Southeast colo, hybrid cloud |

The Brazil data center competitive landscape is characterized by a concentrated leader tier dominated by international and regional wholesale operators, alongside challengers competing on interconnection and edge specialization, with domestic emerging players targeting niche regional workloads.

Key Company Profiles

Ascenty

Ascenty, a joint venture between Digital Realty (49%) and Brookfield Infrastructure (49%), with founder Chris Torto retaining 2%. It is the data center operator in Latin America by installed capacity, with 34+ facilities across Brazil, Chile, Mexico, and Colombia.

- Services Offered: Wholesale and retail colocation, private cloud connect, dark fibre, and interconnection across a 5,000+ km proprietary fibre network.

- Recent Developments: In July 2025, Ascenty announced the construction of a new data center in the São Paulo region, marking 15 years of operating in the Latin American market.

- Strategy: Focus on large-scale campuses (São Paulo, Campinas clusters) targeting AWS, Microsoft, and Google demand.

Equinix Inc.

Equinix is the global interconnection leader with 10+ IBX data centers across São Paulo and Rio de Janeiro, anchoring Equinix Fabric connectivity to AWS, Azure, Google Cloud, and Oracle Cloud.

- Services Offered: Retail colocation, cloud exchange, platform interconnection, and managed network services across SP1-SP5 and RJ1-RJ2 IBX campuses.

- Recent Developments: In April 2026, Equinix launched its latest data center in São Paulo, Brazil. The company has begun operations at SP6, a new data center located in Santana de Parnaíba, in the São Paulo metropolitan area.

- Strategy: Position Brazil as LATAM’s digital hub with dense ecosystems (finance, cloud, networks).

Scala Data Centers

Scala, backed by DigitalBridge, is a pure-play hyperscale platform with a 4.7 GW development pipeline across Latin America, announced in 2024, operating on 100% renewable energy.

- Services Offered: Hyperscale build-to-suit, wholesale colocation, and renewable-powered data center campuses for cloud and AI customers.

- Recent Developments: In May 2025, Scala Data Centers announced that Brazil's Ministry of Mines and Energy (MME) had authorized the 5 GW ramp-up connection of Scala AI City to the National Interconnected System (SIN). This marks one of the largest energy authorizations ever granted by the Executive Branch and the most significant approval to date for a data-center project in Brazil.

- Strategy: Build mega campuses (100–300 MW+) aligned with AI/cloud growth trends.

Market Concentration Analysis

The Brazil data center market exhibits moderate-to-high concentration among the top four operators. Ascenty, Equinix Inc., Scala Data Centers, and Cirion Technologies collectively control an estimated 55-62% of national colocation and wholesale revenue in 2025.

Concentration is most pronounced in the hyperscale wholesale segment, where Ascenty and Scala capture the majority of pre-leased hyperscaler capacity in the São Paulo metro. Retail colocation remains comparatively fragmented, with Equinix leading.

The market is consolidating further through platform-level M&A, exemplified by Aligned Data Centers' 2023 acquisition of ODATA and Digital Realty's continued Ascenty ownership. Domestic operators compete through regional focus and niche specialization.

Investment & Growth Opportunities

Fastest-Growing Segments

Tier 4 capacity is the highest-growth tier sub-segment at ~12.1% CAGR through 2034. AI-dedicated liquid-cooled high-density colocation is emerging as the fastest-growing workload, driven by hyperscaler GPU deployments and enterprise LLM adoption.

Emerging Regional Expansion

The Northeast, anchored by Fortaleza's subsea cable landings, is the fastest-growing region at ~11.8% CAGR through 2034. Secondary metros, including Recife, Porto Alegre, and Brasília, offer attractive land and power economics relative to São Paulo.

Venture & Private Capital Trends

Brazilian data center capital inflows exceeded USD 3 billion in 2024, led by DigitalBridge's backing of Scala, Aligned's ODATA acquisition, and continued Digital Realty investment in Ascenty. Brookfield and GIC remain active Brazilian infrastructure investors.

Future Market Outlook (2026-2034)

The Brazil data center market forecast projects steady value expansion from USD 3.98 Billion in 2025 to USD 9.01 Billion by 2034 at a CAGR of 9.50%, more than doubling in value across nine years. Growth will be driven by hyperscaler capacity, AI workloads, and sovereign cloud.

Three structural shifts will reshape the Brazilian data center industry through 2034. First, AI-driven high-density colocation will require wholesale adoption of liquid cooling by 2027-2028. Second, hyperscale campuses above 100 MW will become the dominant supply unit.

Third, regional decentralization will accelerate, with the Northeast and Central-West capturing a rising share of new supply as São Paulo metro approaches power and land constraints. By 2034, the Brazil data center market will have transformed into a hyperscale-anchored, AI-ready, renewable-powered platform economy.

Research Methodology

Primary Research

Primary research included structured interviews in 2024-2025 with data center operators, hyperscaler cloud regional leads, enterprise CIOs across Brazilian banking, retail, and telecom, EPC contractors, power utilities, and institutional infrastructure investors. Primary inputs validated capacity estimates and tier mix.

Secondary Research

Secondary sources include Anatel telecom reports, Brazilian Central Bank (BACEN) payment statistics, ANPD regulatory publications, IDC Brazil cloud and IT spending data, Uptime Institute tier certification databases, company annual reports, and trade publications covering the Latin American data center sector.

Forecasting Models

Market size estimates and growth projections were derived using a combined top-down and bottom-up model, incorporating Brazilian GDP growth, enterprise IT spending, cloud adoption rates, hyperscaler capacity commitments, and metro-level supply-demand balances. Scenario analysis covered base, optimistic, and conservative cases.

Brazil Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Data Center Sizes Covered | Large, Massive, Medium, Mega, Small |

| Tier Types Covered | Tier 1 and 2, Tier 3, Tier 4 |

| Absorptions Covered | Non-Utilized, Utilized |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Ascenty, Equinix Inc., Scala Data Centers, Cirion Technologies, EdgeUno, HostDime Global Corp., Quântico Data Center, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil data center market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil data center market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil data center industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Data Center Market Report

The Brazil data center market was valued at USD 3.98 Billion in 2025, driven by hyperscaler expansion, fintech workloads, and accelerating enterprise cloud adoption.

The market is projected to reach USD 9.01 Billion by 2034, growing at a CAGR of 9.50% during 2026-2034, supported by AI workloads and sovereign cloud demand.

Tier 3 leads with a 52.4% share in 2025, driven by concurrently maintainable N+1 architecture balancing enterprise-grade reliability with attractive colocation pricing.

Utilized capacity dominates with 71.8% in 2025, reflecting tight supply where newly commissioned megawatts are absorbed within 12-18 months of delivery.

The Southeast leads with a 54.7% share in 2025, anchored by São Paulo's Tamboré and Barueri corridors hosting Latin America's largest interconnection hub.

Key drivers include hyperscale cloud expansion, PIX payments exceeding 64 billion in 2024, 5G rollout across 452 cities, and LGPD-driven data sovereignty.

The Northeast is the fastest-growing region at an estimated 11.8% CAGR, driven by Fortaleza's subsea cable landings and favourable power economics.

Leading companies include Ascenty, Equinix Inc., Scala Data Centers, Cirion Technologies, EdgeUno, HostDime Global Corp., and Quântico Data Center.

LGPD enforcement raises cross-border transfer costs, favouring onshore colocation and sovereign cloud workloads in Brazilian Tier 3 and Tier 4 facilities.

Tier 4 accounts for 28.6% of the Brazil data center market in 2025, driven by banking fault-tolerance needs and hyperscale build-to-suit campuses with 2N redundancy.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)