Boom Lifts Market Size, Share, Trends and Forecast by Engine Type, Product Type, End Use, and Region, 2026-2034

Global Boom Lifts Market Size, Share, Trends & Forecast (2026-2034)

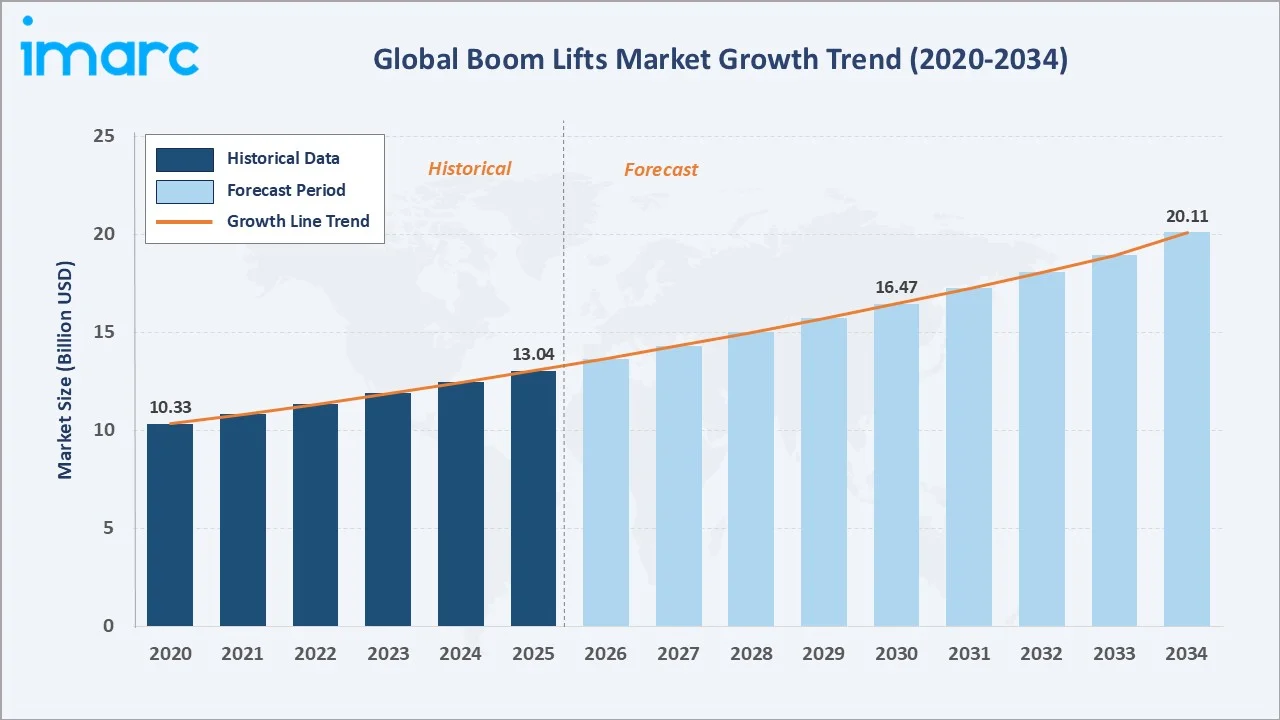

The global boom lifts market size was valued at USD 13.04 Billion in 2025 and is projected to reach USD 20.11 Billion by 2034, exhibiting a CAGR of 4.78% during the forecast period 2026-2034. Rising construction activity, stringent occupational safety regulations, and growing adoption of electric and hybrid aerial work platforms are driving boom lifts market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 13.04 Billion |

|

Forecast Market Size (2034) |

USD 20.11 Billion |

|

CAGR (2026-2034) |

4.78% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

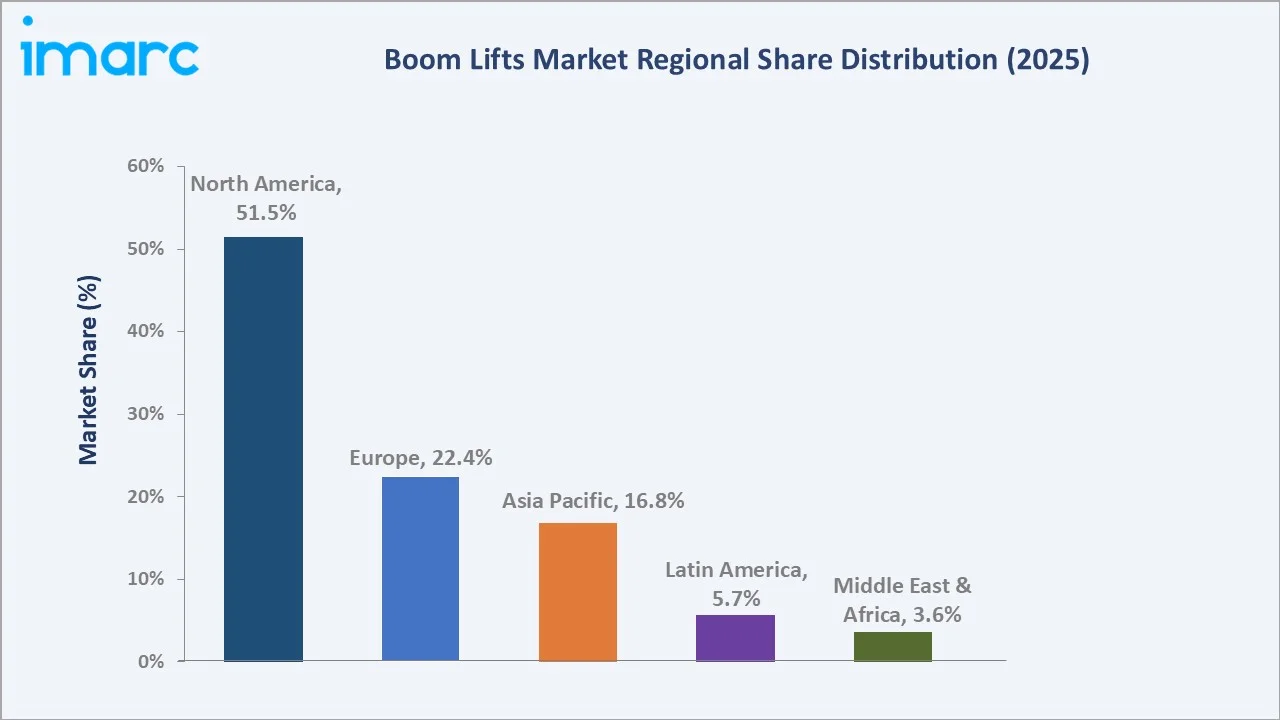

North America (51.5%, 2025) |

|

Fastest Growing Region |

Asia Pacific (~7.4% CAGR, 2026-2034) |

|

Largest Engine Type |

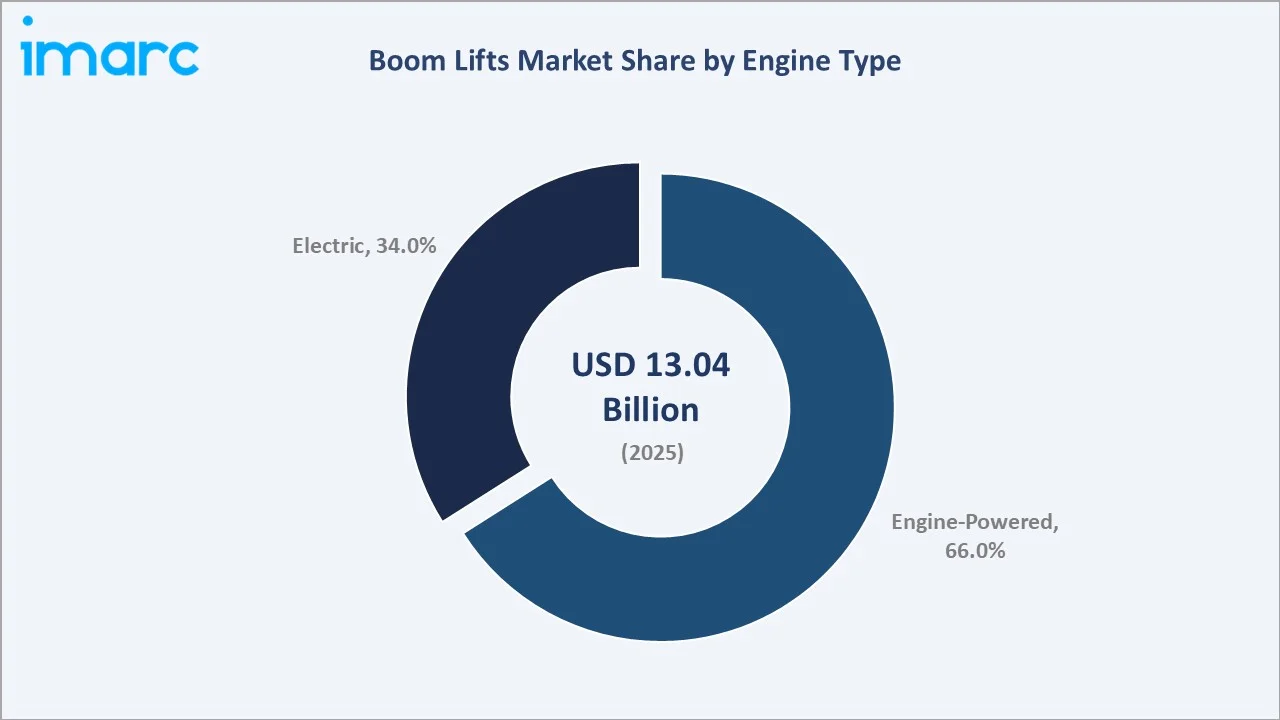

Engine-Powered (66.0%, 2025) |

|

Largest End Use Segment |

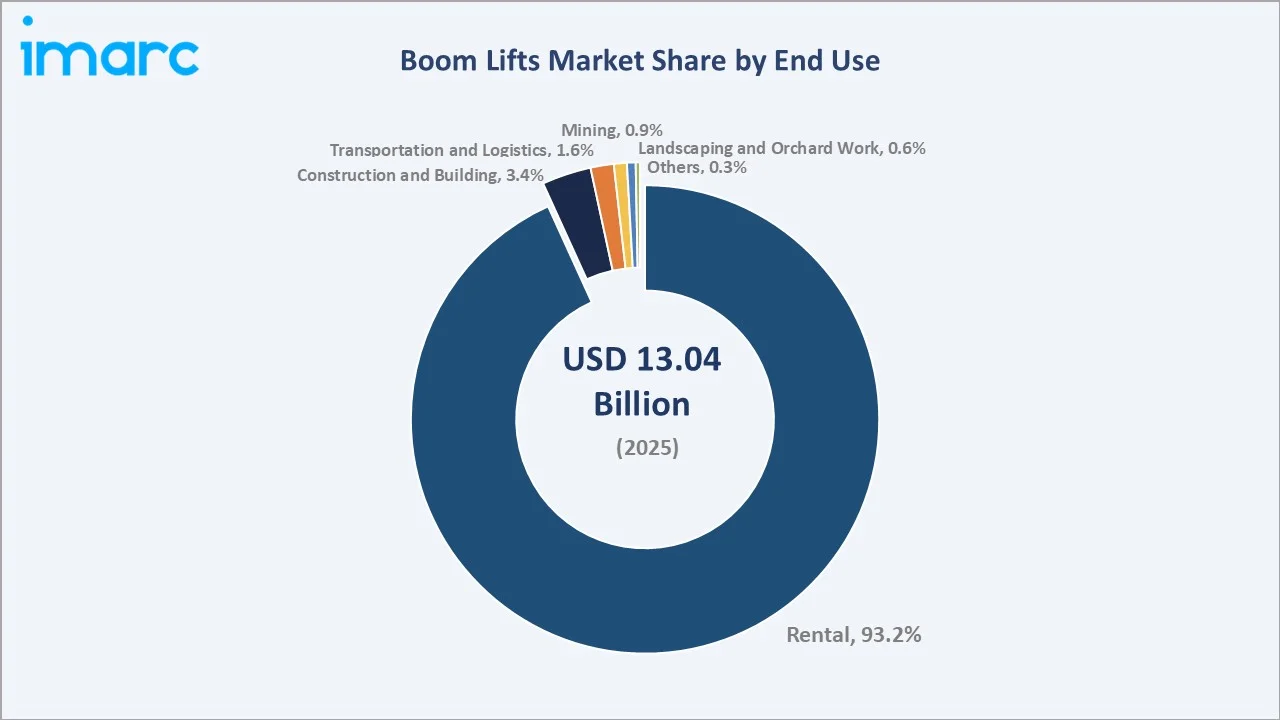

Rental (93.2%, 2025) |

The chart below illustrates the boom lifts market growth trajectory from 2020 through 2034, contrasting the historical expansion period against the sustained forecast curve powered by construction activity, safety compliance mandates, and aerial work platform adoption globally.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight the electric engine type and Construction and Building end use as the fastest-growing sub-categories within the global boom lifts market forecast through 2034.

Executive Summary

The global boom lifts market is undergoing steady expansion, underpinned by accelerating infrastructure investment, growing regulatory mandates for worker height safety, and wide-scale adoption of aerial work platforms. Valued at USD 13.04 Billion in 2025, the market is projected to reach USD 20.11 Billion by 2034 at a CAGR of 4.78% from 2026 to 2034. The market grew from USD 10.33 Billion in 2020, reflecting consistent demand across the historical period.

Engine-powered boom lifts command 66.0% of the engine type segment in 2025 due to superior performance in heavy outdoor applications. The electric segment at 34.0% is the fastest-growing sub-category, driven by zero-emission zone mandates and corporate ESG decarbonization commitments. The rental channel retains 93.2% dominance of end-use demand, reflecting the high capital cost of ownership and preference for operational flexibility. Construction and building at 3.4%, Transportation and Logistics at 1.6%, and Mining at 0.9% represent emerging growth avenues.

North America leads all regions with 51.5% revenue share in 2025. Europe holds 22.4% while Asia Pacific accounts for 16.8% and is projected to be the fastest-growing region at approximately 7.4% CAGR through 2034. The boom lifts market outlook remains positive as electrification, telematics integration, and emerging market rental expansion converge to drive multi-year growth.

Key Market Insights

|

Insight |

Data |

|

Largest Engine Type |

Engine-Powered – 66.0% share (2025) |

|

Second Engine Type |

Electric – 34.0% share (2025) |

|

Largest End Use |

Rental – 93.2% share (2025) |

|

Fastest Growing End Use |

Construction and Building (~5.3% CAGR, 2026-2034) |

|

Leading Region |

North America – 51.5% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – ~7.4% CAGR (2026-2034) |

|

Top Companies |

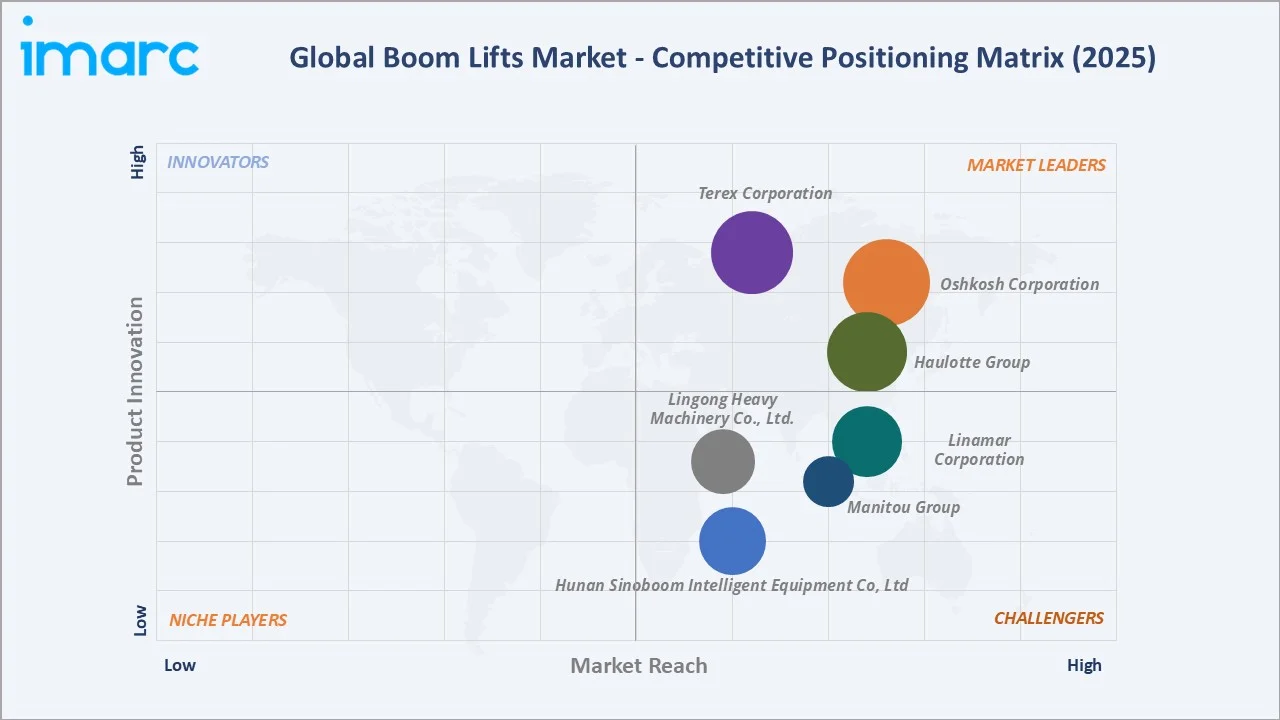

Terex Corporation, Oshkosh Corporation, Haulotte Group, Manitou Group, Linamar Corporation, Lingong Heavy Machinery Co., Ltd., Hunan Sinoboom Intelligent Equipment Co, Ltd |

|

Market Opportunity |

Electric & hybrid lift fleet transition |

Key Analytical Observations Supporting the Above Data:

- Engine-Powered's 66.0% dominance in 2025 reflects unmatched capability in heavy-duty outdoor applications - bridge construction, large industrial maintenance, and terrain-intensive civil works - where diesel power and extended reach are non-negotiable.

- Electric boom lifts at 34.0% are growing faster than the overall market at approximately 6.1% CAGR. EU Ecodesign Regulation requirements effective 2023, zero-emission zone mandates in major cities, and corporate ESG commitments are collectively driving fleet electrification timelines.

- Rental's 93.2% share is the highest channel concentration in the aerial work platform category, reflecting the prohibitive capital cost of ownership and the preference for operational flexibility among construction contractors.

- North America's 51.5% leadership is supported by the U.S. construction industry at approximately USD 2.1 trillion in 2024 and reinforced by OSHA height-work safety mandates that standardize boom lift usage in multi-story construction and utility maintenance.

- Asia Pacific's ~7.4% CAGR reflects accelerating construction in China, India's PMAY-Urban housing initiative targeting over 11.2 million affordable homes and expanding infrastructure investment across Southeast Asia and Australia.

- The electric segment's ~6.1% CAGR is the fastest within the engine type category, driven by hybrid model launches such as LGMG's AR65JE-H (April 2024) which integrates intelligent clutch control for seamless electric-hybrid mode transitions.

Global Boom Lifts Market Overview

Boom lifts are self-propelled or trailer-mounted aerial work platforms designed to elevate personnel and equipment to heights ranging from 20 to 185+ feet with precision and stability. Product variants include articulating boom lifts, telescopic boom lifts, trailer-mounted configurations, vehicle-mounted platforms, and crawler or spider boom variants. Applications span construction, infrastructure maintenance, industrial operations, utility work, landscaping, and transportation logistics.

The industry operates at the intersection of construction demand, occupational safety regulation, environmental compliance, and technological innovation. Macroeconomic drivers include accelerating urbanization - with over half the global population now residing in urban areas per UN estimates - rising government infrastructure expenditure, and increasingly stringent worker safety frameworks such as OSHA, EU-OSHA, and equivalent standards globally. Smart connectivity, IoT telematics, and fleet electrification are structurally reshaping product development and procurement strategies through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Construction and Urbanization Growth: Global construction is the primary boom lift demand lever. The U.S. construction industry reached approximately USD 2.1 trillion in 2024. UN data confirms more than half the global population now lives in urban areas, sustaining multi-year construction pipelines across residential, commercial, and public infrastructure.

- Occupational Safety Regulations: OSHA, EU-OSHA, and equivalent bodies mandate aerial work platform usage at height. The UN Global Compact links work-related causes to 2.78 million annual fatalities globally, driving regulatory pressure for certified height-access equipment over conventional ladders and scaffolding.

- Technological Advancements: EU Ecodesign standards effective from 2023 require new aerial platforms to reduce energy consumption. IoT-enabled lifts provide real-time operational data and predictive maintenance alerts, reducing unplanned downtime and extending equipment service life.

- Rental Market Expansion: The rental channel commands 93.2% of end-use demand in 2025. Growing investment by major rental fleet operators - United Rentals, and Sunbelt Rentals - expands equipment availability and supports market penetration in tier-2 and emerging construction markets globally.

Market Restraints

- High Capital and Maintenance Costs: Acquisition cost for telescopic boom lifts is substantial per unit, limiting direct ownership to large contractors and major fleet operators. Ongoing maintenance and certification costs further constrain penetration in price-sensitive markets.

- Regulatory Certification Complexity: Complying with ANSI A92, EN 280, and regional certification standards requires significant investment. Smaller manufacturers face disproportionate compliance burdens.

- Skilled Operator Shortage: Operating boom lifts requires certified training. Workforce shortages in skilled construction trades across North America and Europe are creating fleet utilization bottlenecks.

Market Opportunities

- Electric and Hybrid Fleet Transition: Zero-emission mandates in urban construction zones are creating a high-value fleet replacement cycle. LGMG's AR65JE-H hybrid model and similar launches are accelerating electrification timelines across rental fleets.

- Emerging Market Infrastructure Build-Out: India targets over 11.2 million affordable urban homes under PMAY, generating sustained demand for construction-grade aerial access equipment. Vietnam, Indonesia, and Sub-Saharan Africa also offer significant volume growth potential.

- IoT and Telematics Services: Smart connectivity platforms delivering predictive maintenance, fleet utilization analytics, and remote diagnostics are creating new value-added revenue streams for rental operators and OEMs.

Market Challenges

- Component Supply Chain Volatility: Steel, hydraulic components, and electronic sensor availability are subject to geopolitical disruptions, impacting production timelines and inflating manufacturing costs.

- Engine Type Transition Risk: The structural shift from engine-powered to electric requires significant R&D reinvestment and battery supply chain development, posing transition risk for manufacturers heavily dependent on diesel platforms.

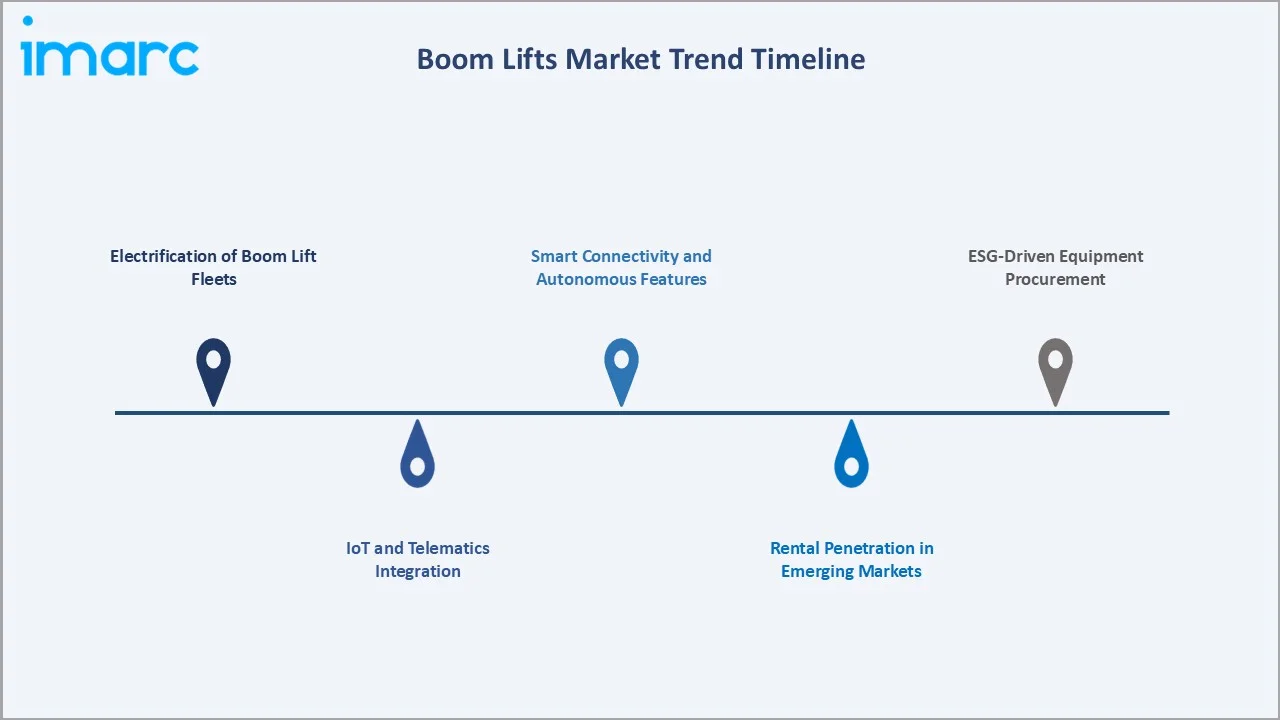

Emerging Market Trends

1. Electrification of Boom Lift Fleets

Electric boom lifts at 34.0% in 2025 are projected to grow at approximately 6.1% CAGR through 2034 - the fastest sub-category within the engine type segment. Urban zero-emission zone mandates in Europe, corporate sustainability reporting requirements, and declining lithium-ion battery costs are collectively accelerating fleet electrification. Hybrid models bridging the performance gap are gaining rapid traction, as demonstrated by LGMG's AR65JE-H launch in April 2024.

2. IoT and Telematics Integration

Modern boom lift fleets are increasingly equipped with IoT sensors, GPS tracking, and cloud-based telematics platforms. These systems enable predictive maintenance scheduling, real-time utilization monitoring, and remote diagnostics. Rental fleet operators report significant reductions in unplanned downtime with IoT-enabled fleet management, making telematics adoption a competitive differentiator.

3. Smart Connectivity and Autonomous Features

Leading manufacturers are integrating semi-autonomous positioning, automated self-leveling, and load-sensing safety systems into mid- to premium-tier platforms. These features reduce operator error, improve job site productivity, and support compliance with evolving safety certifications. Voice-command and augmented-reality-guided operation interfaces represent near-term product differentiation frontiers.

4. Rental Penetration in Emerging Markets

Rental penetration in Asia Pacific and Latin America remains significantly below the global average. As urban construction accelerates in India, Vietnam, and Brazil, organized rental operators are investing in regional fleet deployment. Regulatory formalization of height-work safety standards is expected to catalyze rapid rental adoption in these markets through 2034.

5. ESG-Driven Equipment Procurement

Large contractors and infrastructure project owners are embedding ESG criteria into equipment procurement frameworks. Preference for low-emission, noise-reduced, and operator-safety-certified boom lifts is translating into procurement specifications that favor electric and certified hybrid platforms over conventional diesel equipment across European and North American job sites.

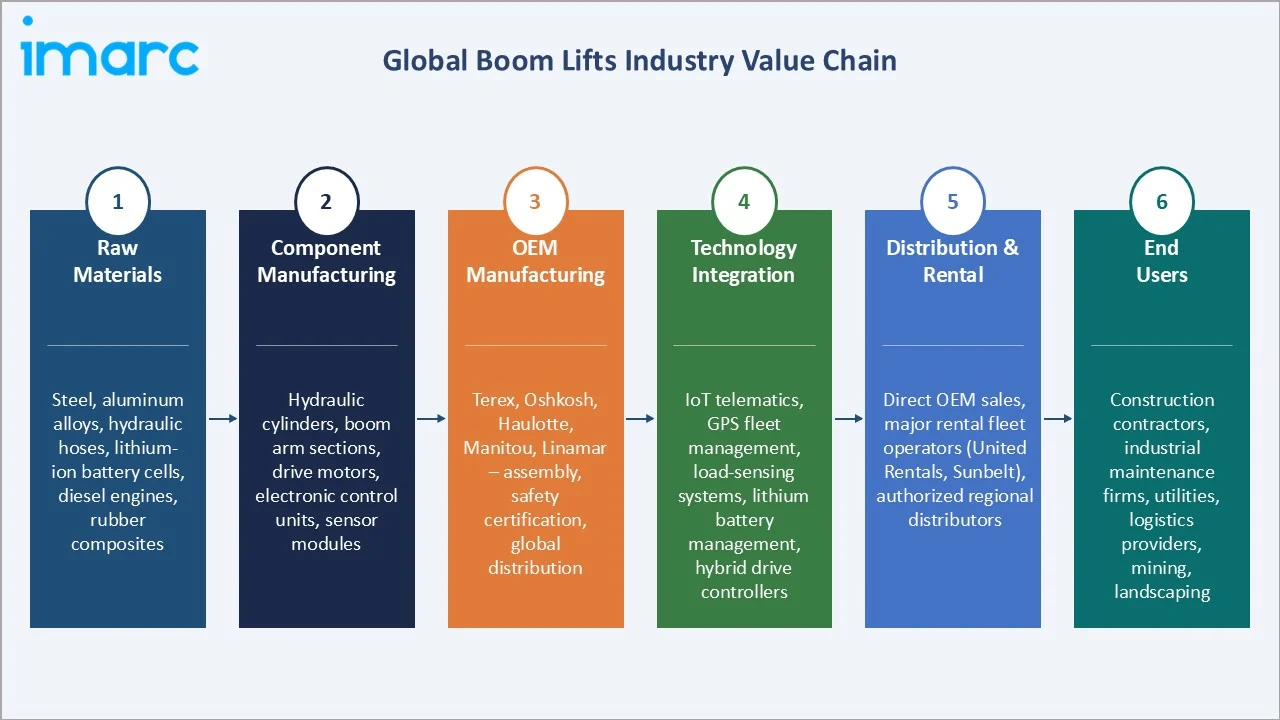

Industry Value Chain Analysis

The global boom lifts industry value chain spans five integrated stages from raw material supply through end-user deployment, each presenting distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall boom lifts market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Steel, high-strength aluminum alloys, hydraulic hose assemblies, lithium-ion battery cells, diesel engines, rubber composites |

|

Component Manufacturing |

Hydraulic cylinders, boom arm sections, drive motors, electronic control units, sensor modules – produced by Tier-2/3 suppliers in China, Germany, USA, and South Korea |

|

OEM Manufacturing |

Terex Corporation, Oshkosh Corporation, Haulotte Group, Manitou Group, Linamar Corporation – full assembly, safety certification, global distribution |

|

Technology Integration |

IoT telematics systems, GPS fleet management, load-sensing systems, lithium battery management units, hybrid drive controllers |

|

Distribution & Rental |

Direct OEM sales, major rental fleet operators (United Rentals, Sunbelt) authorized regional distributors |

|

End Users |

Construction contractors, industrial maintenance firms, utilities operators, logistics providers, mining companies, landscaping operators |

OEMs hold the highest margin position by integrating components, advanced drive systems, and safety certifications into turnkey solutions. The rental channel commands over 93.2% of end-use demand, concentrating procurement decisions among major fleet operators with significant bargaining power over OEM pricing.

Technology Landscape in the Boom Lifts Industry

Electric and Hybrid Drive Systems

Lithium-ion battery technology is replacing lead-acid systems in electric boom lifts, delivering higher energy density, faster charging, and longer service intervals. Hybrid platforms integrating intelligent clutch control - as demonstrated by LGMG's AR65JE-H in April 2024 - enable seamless transitions between electric and engine-powered modes.

IoT Telematics and Fleet Management

Cloud-connected telematics platforms enable real-time monitoring of equipment health, operator behavior, location tracking, and predictive maintenance alerts. Integration with ERP and fleet management software is standardizing data-driven asset lifecycle management across large construction and rental organizations.

Advanced Safety Systems

Load-sensing systems, automatic stabilizer deployment, tilt detection, and proximity sensors are becoming standard across mid- to premium-tier platforms. Semi-autonomous positioning features reduce reliance on skilled operators while improving safety compliance. OSHA and EN 280 certification requirements are standardizing safety feature specifications across all boom lift product tiers globally.

Materials and Structural Innovation

High-strength steel and lightweight aluminum alloy boom arm structures enable greater reach heights without corresponding weight increases. Composite materials are being explored for non-load-bearing components to further reduce platform weight and improve transportability, particularly for trailer-mounted and spider boom configurations.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Engine Type |

Engine-powered |

66.0% |

2025 |

|

Product Type |

Vehicle Mounted Booms |

🔒 |

2025 |

|

End Use |

Rental |

93.2% |

2025 |

|

Region |

North America |

51.5% |

2025 |

By Engine Type

To access detailed market analysis, Request Sample

Engine-powered boom lifts lead the engine type segment with a 66.0% share in 2025. High-capacity diesel and gasoline engines provide the power necessary to handle heavy loads and challenging terrains, making them indispensable for outdoor construction, mining, and infrastructure maintenance. Key markets include North America and the Middle East, where outdoor construction activity is highest and zero-emission restrictions have yet to reach full adoption.

By End Use

Rental is the overwhelmingly dominant end-use segment at 93.2% of the global market in 2025. The rental model enables SMEs, project-based contractors, and utilities operators to access high-cost aerial work platforms without capital expenditure commitments. Major rental fleet operators - including United Rentals, Sunbelt Rentals, and Loxam - drive the vast majority of global boom lift procurement volumes.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

51.5% |

U.S. construction, OSHA safety mandates, strong rental fleet operators, infrastructure investment |

|

Europe |

22.4% |

EU Ecodesign standards, zero-emission zone mandates, electric fleet transition, aging infrastructure maintenance |

|

Asia Pacific |

16.8% |

China construction pipeline, India PMAY housing, ASEAN urbanization, growing safety regulations |

|

Latin America |

5.7% |

Brazil and Colombia construction, rental market formalization, expanding middle class |

|

Middle East & Africa |

3.6% |

GCC mega-projects, oil & gas maintenance, growing urban infrastructure |

North America

North America commands 51.5% of global revenue in 2025, making it the dominant boom lifts region. The United States anchors the market with a construction industry estimated at approximately USD 2.1 trillion in 2024. OSHA-enforced height-work safety regulations standardize aerial work platform usage across building construction and utility maintenance. Major rental fleet operators such as United Rentals and Sunbelt Rentals drive procurement volumes. Canada contributes through infrastructure investment in energy and public works sectors.

Competitive Landscape

|

Company Name |

Brand |

Market Position |

Core Strength |

|

Terex Corporation |

Genie |

Leader |

Widest portfolio, global distribution, strong North America & Europe presence |

|

Oshkosh Corporation |

JLG |

Leader |

Premium telescopic/articulating booms, ClearSky telematics, military/industrial |

|

Haulotte Group |

Haulotte |

Leader |

European market leader, strong electric HAC product line, localized manufacturing |

|

Manitou Group |

Manitou |

Challenger |

Versatile lift range, construction and agricultural market strength |

|

Linamar Corporation |

Skyjack |

Challenger |

Focused boom & scissor portfolio, strong North America and Europe rental fleet |

|

Lingong Heavy Machinery Co., Ltd. |

LGMG |

Challenger |

Fast-growing Chinese OEM, hybrid AR65JE-H, expanding international footprint |

|

Hunan Sinoboom Intelligent Equipment Co, Ltd |

Sinoboom |

Challenger |

Cost-competitive Chinese OEM, growing rental presence in Asia Pacific |

The global boom lifts competitive landscape is moderately consolidated. Chinese manufacturers are rapidly gaining international market share through cost-competitive platforms and increasingly sophisticated product portfolios.

Key Company Profiles

Terex Corporation

Terex Corporation is a U.S.-based global manufacturer of industrial equipment, with a strong presence in aerial work platforms, including boom lifts. Headquartered in Norwalk, Connecticut, the company operates across North America, Europe, Asia-Pacific, and other international markets.

- Product Portfolio: Terex Corporation offers, through its brand Genie, a comprehensive portfolio that includes telescopic boom lifts (S-Boom series), articulating boom lifts (Z-Boom series), trailer-mounted platforms, and vehicle-mounted configurations. Flagship models such as the S-65 TraX and S-85 XC deliver high reach capabilities and robust outdoor performance.

- Recent Developments: In 2025, Terex has launched its new TRX Series of telescopic aerial devices at the Utility Expo 2025, featuring a lightweight boom design combined with heavy-duty performance. The range includes four models with improved payload capacity, enhanced articulation via a new Ranger jib, and simplified maintenance through common components and fiberglass boom construction.

- Strategic Focus: Terex Corporation’s strategy focuses on maintaining portfolio breadth across all height segments, expanding telematics-enabled fleet management services, and accelerating rental fleet customers' transition toward electric and hybrid platforms.

Oshkosh Corporation

Oshkosh Corporation is a leading U.S.-based industrial manufacturer specializing in purpose-built vehicles and equipment for critical applications. Founded in 1917 and headquartered in Oshkosh, Wisconsin, the company serves global markets with operations and sales spanning over 150 countries.

- Product Portfolio: Oshkosh Corporation offer through it division JLG, a comprehensive portfolio that includes the 1850SJ – the world's tallest self-propelled boom lift at 185 feet – the T Series electric boom lifts, and articulating ultra-boom configurations for demanding industrial applications.

- Recent Developments: In 2025, Oshkosh Corporation announced at CES 2026 that it will showcase advanced AI, robotics, connectivity, and electrification technologies across its equipment portfolio, including innovations in aerial work platforms. A key highlight is the JLG Boom Lift with Robotic End Effector, which has received top honors in the CES Innovation Awards.

- Strategic Focus: Oshkosh Corporation’s strategy centers on maintaining premium positioning, growing ClearSky digital platform adoption among rental customers, and expanding its electric product line globally to address evolving emissions compliance requirements.

Haulotte Group

Haulotte Group is a France-based global manufacturer specializing in aerial work platforms and people lifting equipment. Headquartered in Lorette, France, the company is recognized as a leading global player and the largest European manufacturer in the access equipment industry.

- Product Portfolio: Haulotte's boom lift portfolio includes the HA articulating series, HT telescopic series, and the HAC electric boom range – Europe's first fully connected electric articulating boom lift range with lithium battery systems.

- Recent Developments: Haulotte Group announced that its subsidiary Haulotte Ibérica received the “Best Equipment” award for the HA20 E articulating boom lift. The recognition highlights the machine’s strong performance, electric efficiency, and suitability for modern job sites.

- Strategic Focus: Haulotte's strategy focuses on electric product leadership in Europe, telematics services expansion, and growing its presence in emerging markets through localized manufacturing in China and Brazil.

Market Concentration Analysis

The global boom lifts market exhibits moderate consolidation. The top five players - Terex Corporation, Oshkosh Corporation, Haulotte Group, Manitou Group, Linamar Corporation - collectively account for an estimated 55–65% of global revenue in 2025. This consolidation reflects the significant capital requirements for global manufacturing, OEM safety certification compliance, and rental fleet infrastructure investment necessary to compete effectively at scale.

The market is experiencing a bifurcated competitive dynamic. At the premium OEM tier, consolidation is strengthening around technology platforms, telematics capabilities, and electric product leadership. Simultaneously, Chinese manufacturers are rapidly gaining international market share through cost-competitive offerings, intensifying price competition across mid-tier boom lift segments globally through 2034.

Strategic acquisitions and joint ventures are reshaping regional market positions. Oshkosh Corporation's ongoing integration of JLG's digital services capabilities and Haulotte's localized manufacturing investments in China and Brazil illustrate the dual growth strategies of premium positioning and emerging market penetration that define the competitive evolution of the boom lifts market.

Investment & Growth Opportunities

Fastest-Growing Segments

The electric boom lift sub-segment, projected to grow at approximately 6.1% CAGR through 2034, represents the most compelling technology investment opportunity. EU zero-emission mandates, expanding urban construction activity in emission-restricted zones, and declining lithium-ion battery costs are collectively driving fleet electrification timelines ahead of previous projections.

Emerging Market Expansion

Asia Pacific, with an estimated 7.4% CAGR through 2034, represents the highest-growth regional opportunity. India's PMAY-Urban housing initiative targeting over 11.2 million affordable homes, Vietnam and Indonesia's accelerating urban construction pipelines, and Latin America's rental market formalization offer significant volume growth opportunities for organized rental operators and OEMs.

Venture and Strategic Investment Trends

Strategic investment is concentrating in three primary areas: electric and hybrid drivetrain development, IoT telematics and fleet management platform build-out, and emerging market distribution infrastructure expansion. Battery technology partnerships and supply chain agreements for lithium-ion cell procurement are emerging as critical strategic priorities for major OEMs targeting fleet electrification timelines through 2030.

Future Market Outlook (2026-2034)

The global boom lifts market forecast projects steady value expansion from USD 13.04 Billion in 2025 to USD 20.11 Billion by 2034 at a CAGR of 4.78%. An intermediate milestone of USD 16.47 Billion is projected for 2030, reflecting consistent mid-cycle growth driven by construction activity and fleet renewal cycles globally.

Technological disruptions - primarily fleet electrification and IoT platform integration - will reshape competitive positioning over the forecast horizon. OEMs that invest early in electric product portfolios, telematics-enabled service models, and emerging market distribution networks are positioned to outperform the overall market CAGR through 2034.

The rental channel is expected to maintain structural dominance of end-use demand through 2034. Electric and hybrid boom lifts are projected to account for a significant share of new unit shipments by the early 2030s. Asia Pacific's share is forecast to expand steadily by 2034, narrowing the regional gap with Europe while North America maintains its overall leadership position.

Research Methodology

Primary Research

The primary research phase involved structured interviews with industry stakeholders including boom lift OEMs, rental fleet operators, construction contractors, procurement managers, and industry associations. Primary inputs validated quantitative market estimates, corroborated qualitative trend assessments, and provided ground-level perspective on evolving end-user demand dynamics.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, SEC/regulatory filings, industry association publications, trade press, government construction expenditure data, and regulatory frameworks including OSHA, EU Ecodesign, and ANSI standards. Market data from 2020 through 2025 formed the historical baseline for all sizing and segmentation analyses.

Forecasting Models

Market forecasts were developed using a combination of bottom-up demand modeling from end-use segment analysis, top-down supply-side validation through OEM shipment and rental fleet data, and regression-based scenario modeling. The base case forecast of 4.78% CAGR reflects a moderate growth scenario balancing infrastructure investment tailwind against macroeconomic headwinds including interest rate sensitivity in construction spending.

Boom Lifts Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Engine Types Covered | Electric, Engine-Powered |

| Product Types Covered | Trailer Mounted Booms, Vehicle Mounted Booms, Crawler/Spider Booms |

| End Uses Covered | Rental, Construction and Building, Mining, Transportation and Logistics, Landscaping and Orchard Work, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Terex Corporation, Oshkosh Corporation, Haulotte Group, Manitou Group, Linamar Corporation, Lingong Heavy Machinery Co., Ltd., Hunan Sinoboom Intelligent Equipment Co, Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the boom lifts market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global boom lifts market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the boom lifts industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Boom Lifts Market Report

The global boom lifts market size was valued at USD 13.04 Billion in 2025, growing from USD 10.33 Billion in 2020.

The boom lifts market is projected to grow at a CAGR of 4.78% from 2026 to 2034.

Engine-powered boom lifts lead with a 66.0% market share in 2025, driven by superior performance in heavy-duty outdoor construction applications.

Electric boom lifts at 34.0% in 2025 are the fastest-growing sub-segment at approximately 6.1% CAGR, driven by emission regulations and fleet decarbonization mandates.

The rental segment dominates with a 93.2% share in 2025, reflecting the high capital cost of ownership and contractor preference for operational flexibility.

North America holds 51.5% of the boom lifts market in 2025, driven by the approximately USD 2.1 trillion U.S. construction industry and OSHA safety mandates.

Asia Pacific is the fastest-growing region at approximately 7.4% CAGR through 2034, led by China's construction pipeline and India's PMAY-Urban housing initiative.

Key players include Terex Corporation, Oshkosh Corporation, Haulotte Group, Manitou Group, Linamar Corporation, Lingong Heavy Machinery Co., Ltd., and Hunan Sinoboom Intelligent Equipment Co, Ltd.

Key drivers include rising global construction activity, stringent OSHA and EU occupational safety regulations, technological advancements in electric platforms, and rental market expansion.

The global boom lifts market is projected to reach USD 16.47 Billion by 2030, growing steadily toward the 2034 forecast of USD 20.11 Billion at 4.78% CAGR.

The Construction and Building end-use segment hold 3.4% of the boom lifts market in 2025, representing direct-ownership procurement by large-scale construction contractors.

Key boom lifts market trends include fleet electrification, IoT telematics integration, ESG-driven procurement, rental expansion in emerging markets, and hybrid model innovation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)