Biological Skin Substitutes Market Report by Type (Human Donor Tissue-Derived Products, Acellular Animal-Derived Products), Application (Acute Wounds, Chronic Wounds), End User (Hospitals, Outpatient Facilities, Research and Manufacturing), and Region 2026-2034

Market Overview:

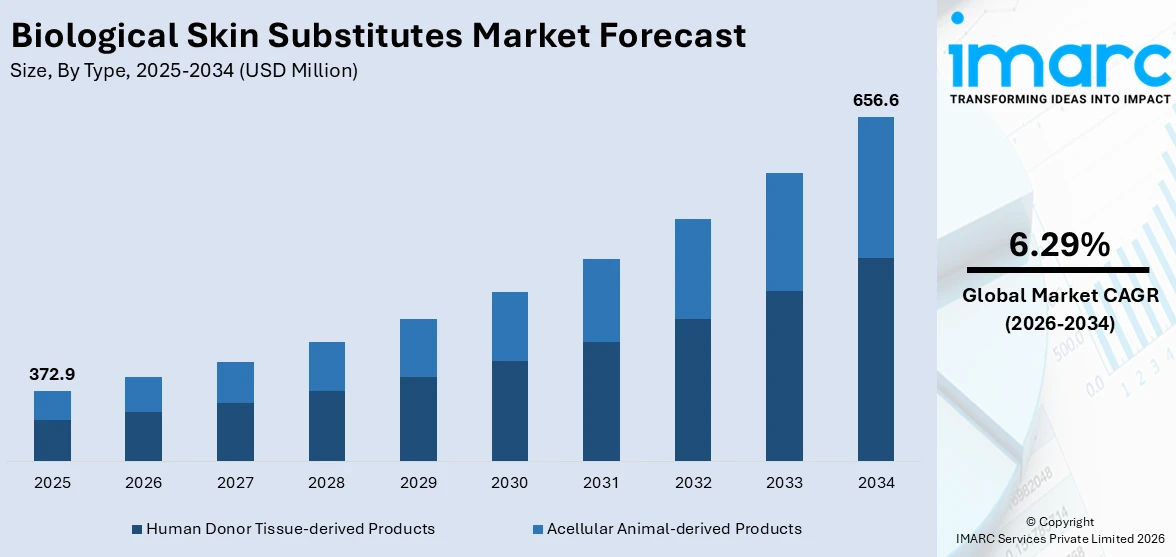

The global biological skin substitutes market size reached USD 372.9 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 656.6 Million by 2034, exhibiting a growth rate (CAGR) of 6.29% during 2026-2034. The growing incidence of chronic wounds and diabetes, the accelerating costs and complexities of treating chronic wounds, and the improved insurance coverage for treatments involving biological skin substitutes are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 372.9 Million |

| Market Forecast in 2034 | USD 656.6 Million |

| Market Growth Rate (2026-2034) | 6.29% |

Biological skin substitutes play a crucial role in the field of wound care and tissue engineering. They are lab-grown alternatives made from natural, biocompatible materials like collagen or cultured skin cells. Designed to closely mimic the structure and function of natural human skin, these substitutes aid in the healing process of severe skin injuries, such as burns, ulcers, and surgical wounds. Biological skin substitutes not only provide immediate relief by covering the exposed wound but also promote the natural regeneration of skin tissues. They are commonly used in cases where traditional treatments, like skin grafts from the patient or donors, are not viable options. This technology has been especially beneficial in treating patients with extensive wounds or those with conditions like diabetes, where healing is often slow and complicated.

To get more information on this market Request Sample

One of the primary market drivers for the biological skin substitutes industry is the escalating incidence of chronic wounds and diabetes worldwide. Additionally, chronic conditions such as venous leg ulcers and pressure ulcers also contribute to the increasing need for effective wound care solutions. As healthcare systems continue to grapple with the accelerating costs and complexities of treating chronic wounds, the demand for biological skin substitutes is expected to grow. Along with this, the growing aging global population coupled with increased life expectancy is significantly supporting the market. Older individuals are more susceptible to skin-related issues, including slower healing rates, making them ideal candidates for advanced wound care solutions. In addition, the rising popularity of cosmetic and reconstructive surgeries is positively influencing the market. Biological skin substitutes are finding applications beyond wound healing, including in procedures for scar revision and aesthetic enhancements. Apart from this, improved insurance coverage for treatments involving biological skin substitutes makes these options more accessible to a broader population. Thus, this is contributing to the market. Moreover, the accelerating number of partnerships between academic institutions, research labs, and private companies is creating a positive market outlook.

Biological Skin Substitutes Market Trends/Drivers:

Regulatory Support and Funding

The biological skin substitutes industry is also being propelled by supportive regulatory frameworks and increased funding. Agencies have been encouraging innovation in this field by expediting the approval process for products that show promise in treating life-threatening or severely debilitating conditions. Along with this, government grants, private investments, and public-private partnerships are providing essential financial support for research and product development. This influx of resources helps companies to accelerate the development timeline and to conduct comprehensive clinical trials, thereby ensuring the safety and efficacy of new products. Moreover, the favorable regulatory and financial landscape, therefore, plays a crucial role in driving market expansion.

Growing Awareness and Accessibility in Emerging Markets

The awareness about the benefits of biological skin substitutes is growing, especially in emerging markets. These markets are witnessing a rapid improvement in healthcare infrastructure, bolstered by increasing GDP and healthcare spending. Moreover, localized initiatives and educational programs are spreading knowledge about advanced wound care solutions among healthcare providers. The expanding distribution channels, including online platforms and healthcare centers, have made it easier for clinicians in emerging markets to access these advanced products. This increased accessibility coupled with growing awareness is opening new avenues for the industry, thereby acting as a substantial market driver. As these markets continue to mature, the demand for biological skin substitutes is expected to rise, offering lucrative opportunities for industry expansion.

Advancements in Tissue Engineering Technology

Technological advancements in the field of tissue engineering have acted as a significant market driver for the biological skin substitutes industry. In addition, the growing investment in research and development has led to the creation of more effective, biocompatible, and cost-efficient products. Early substitutes had limitations such as lower durability and reduced integration with native tissue. In confluence with this, the widespread use of stem cells, bioactive molecules, and advanced polymers has enriched the functionality and reliability of these substitutes. These innovations have not only increased the efficacy of biological skin substitutes but also expanded their application in diverse clinical settings, thus driving market growth.

Biological Skin Substitutes Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global biological skin substitutes market report, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on type, application, and end user.

Breakup by Type:

- Human Donor Tissue-derived Products

- Acellular Animal-derived Products

Human donor tissue-derived products dominate the market

The report has provided a detailed breakup and analysis of the market based on the type. This includes human donor tissue-derived products and acellular animal-derived products. According to the report, human donor tissue-derived products represented the largest segment.

The biological skin substitutes industry is experiencing significant growth, driven by the increasing prevalence of chronic wounds, such as diabetic ulcers and burns, which require advanced treatment options. Technological advancements in tissue engineering have enabled the development of more efficient and reliable human donor tissue-derived products. These products offer better wound healing and reduced scarring, making them increasingly favored in clinical settings. In addition, a rise in healthcare expenditure and growing awareness among patients and clinicians are propelling the demand for these advanced substitutes. Regulatory support for biocompatible and safe products is also an enabling factor, ensuring quality and effectiveness in treatment outcomes.

On the other hand, the cost-effectiveness of animal-derived products makes them an attractive option for healthcare providers. They offer a viable alternative to more expensive human donor tissue-derived or synthetic options. Additionally, technological advancements have improved the safety, efficacy, and biocompatibility of these products. An aging population, more prone to chronic conditions like diabetic ulcers and pressure sores, is also increasing the demand for effective wound care solutions. Regulatory bodies are further supporting market growth by setting stringent yet achievable quality standards. Overall, these drivers contribute to the rising adoption and expansion of acellular animal-derived products in the biological skin substitutes market.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

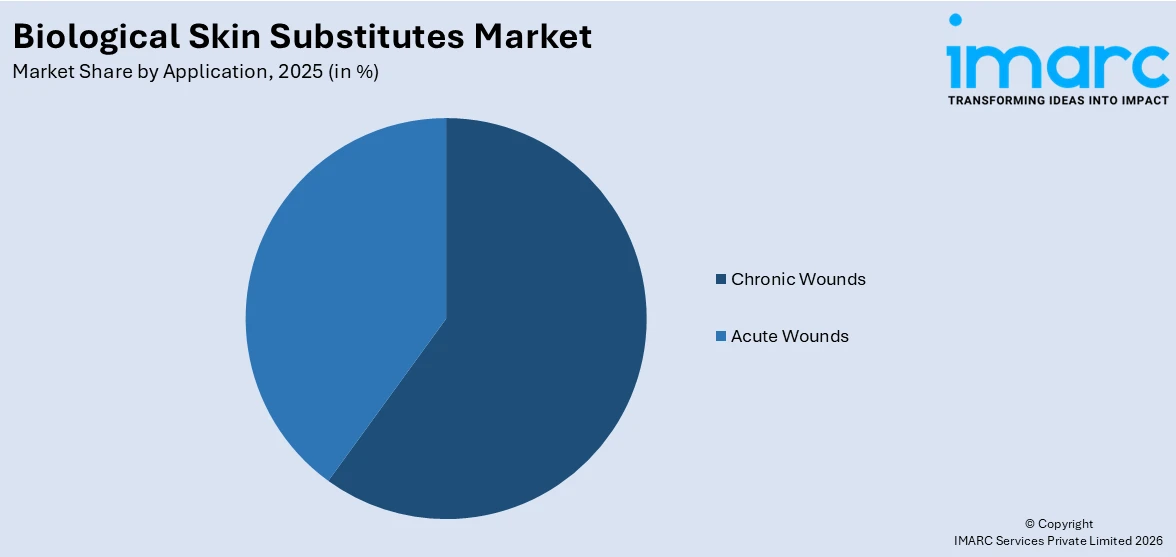

- Acute Wounds

- Chronic Wounds

Chronic wounds hold the largest share in the market

A detailed breakup and analysis of the market based on the application has also been provided in the report. This includes acute wounds and chronic wounds. According to the report, chronic wounds accounted for the largest market share.

A significant driver is the escalating prevalence of chronic conditions such as diabetes and obesity, which are often associated with complex, non-healing wounds. Biological skin substitutes offer enhanced healing capabilities and are increasingly recommended for chronic wounds, such as diabetic ulcers and venous leg ulcers. Additionally, an aging global population, more susceptible to chronic conditions, expands the patient base requiring specialized wound care. There's also growing awareness among healthcare professionals about the efficacy of biological skin substitutes, further fueling demand. Moreover, regulatory agencies are streamlining approval processes for clinically effective products, thereby supporting the market's expansion.

On the contrary, the acute wounds segment in the biological skin substitutes industry is experiencing robust growth due to the rising incidence of accidents and trauma cases that necessitate immediate and effective wound treatment. Biological skin substitutes offer quick healing and reduced infection risks, making them ideal for acute wounds. Additionally, advancements in surgical procedures are leading to an increase in surgeries, where biological substitutes can play a vital role in post-operative care. In confluence with this, heightened awareness among healthcare providers about the benefits of these advanced treatments contributes to market adoption. Regulatory frameworks that encourage the use of safe and effective medical products are also supporting market growth.

Breakup by End User:

- Hospitals

- Outpatient Facilities

- Research and Manufacturing

Hospitals dominates the market

The report has provided a detailed breakup and analysis of the market based on the end user. This includes hospitals, outpatient facilities, and research and manufacturing. According to the report, hospitals represented the largest segment.

The hospital end user in the biological skin substitutes industry is experiencing significant growth, due to multiple market drivers. Additionally, hospitals are often the first point of care for severe injuries and chronic wounds, necessitating advanced treatment options. Along with this, the increasing availability of specialized wound care units within hospitals boosts the adoption of these products. Furthermore, hospitals are more likely to adopt new technologies, backed by medical staff who are often at the forefront of research and training. Regulatory support in the form of reimbursements for proven-effective treatments also incentivizes hospitals to incorporate these substitutes. Moreover, an increase in healthcare spending provides the financial backing needed for adopting advanced treatments.

On the other hand, the role of outpatient facilities as an end user in the biological skin substitutes industry is growing, due to the shift towards minimally invasive treatments and shorter hospital stays, making outpatient facilities an ideal setting for ongoing wound care. These facilities are more accessible for routine follow-ups, crucial for the effective application of biological skin substitutes, especially for chronic wounds. In confluence with this, outpatient settings often offer cost-effective treatment, appealing to both healthcare providers and patients. The accelerated prevalence of chronic conditions also boosts the number of patients requiring outpatient wound care.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest biological skin substitutes market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represented the largest segment.

The North America market for biological skin substitutes is witnessing substantial growth, prompted by the high prevalence of lifestyle-related chronic conditions such as diabetes and obesity, which contribute to complex wound issues. The region also benefits from advanced healthcare infrastructure and higher healthcare expenditure, enabling quicker adoption of cutting-edge technologies. Furthermore, there is strong support from regulatory agencies, including the FDA, which has streamlined approval processes for biologically-derived products that demonstrate safety and efficacy. An aging population, more susceptible to chronic and acute wounds, additionally widens the consumer base. Moreover, increased awareness among both clinicians and patients about the benefits of these products propels market growth.

On the contrary, the Asia Pacific region is experiencing rapid growth, fueled by the region's increasing healthcare expenditure, making advanced treatments more accessible. Technological advancements and growing interest in medical research within countries like China, India, and Japan further encourage the adoption of innovative products such as biological skin substitutes. The expanding healthcare infrastructure, including hospitals and outpatient facilities, provides an additional platform for market growth. Furthermore, local regulatory bodies are increasingly supportive of safe and effective wound care products, which contributes to a favorable market environment.

Competitive Landscape:

The market is experiencing significant growth due to the introduction of more effective and affordable products that provide superior wound healing and reduced complications. Partnerships and collaborations with academic institutions are also common to foster innovation. Many companies are seeking regulatory approvals for new products and expanding their product portfolios through acquisitions and mergers to strengthen their market position. Another focal area is global expansion. Companies are entering emerging markets, such as Asia-Pacific, where healthcare infrastructure is improving and the prevalence of conditions requiring wound care is rising. In addition, marketing and awareness campaigns are being run to educate healthcare providers and patients on the advantages of biological skin substitutes over traditional treatments. Some companies are also working on developing personalized solutions that cater to individual patient needs for more effective treatment outcomes. Furthermore, key players are investing in quality control and manufacturing processes to ensure product safety and efficacy. This is crucial for gaining regulatory approvals and establishing trust among end-users.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Integra LifeSciences

- Mallinckrodt Pharmaceuticals

- MIMEDX Group Inc.

- Organogenesis Holdings Inc.

- Smith & Nephew PLC

- Stryker Corporation

- Tissue Regenix Group

- Vericel Corporation

Biological Skin Substitutes Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Human Donor Tissue-Derived Products, Acellular Animal-Derived Products |

| Applications Covered | Acute Wounds, Chronic Wounds |

| End Users Covered | Hospitals, Outpatient Facilities, Research and Manufacturing |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Integra LifeSciences, Mallinckrodt Pharmaceuticals, MIMEDX Group Inc., Organogenesis Holdings Inc., Smith & Nephew PLC, Stryker Corporation, Tissue Regenix Group. Vericel Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global biological skin substitutes market performed so far, and how will it perform in the coming years ?

- What are the drivers, restraints, and opportunities in the global biological skin substitutes market ?

- What is the impact of each driver, restraint, and opportunity on the global biological skin substitutes market ?

- What are the key regional markets ?

- Which countries represent the most attractive biological skin substitutes market ?

- What is the breakup of the market based on the type ?

- Which is the most attractive type in the biological skin substitutes market ?

- What is the breakup of the market based on the application ?

- Which is the most attractive application in the biological skin substitutes market ?

- What is the breakup of the market based on the end user ?

- Which is the most attractive end user in the biological skin substitutes market ?

- What is the competitive structure of the global biological skin substitutes market ?

- Who are the key players/companies in the global biological skin substitutes market ?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the biological skin substitutes market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global biological skin substitutes market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the biological skin substitutes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)