Biodiesel Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition

Biodiesel Price Trend, Index and Forecast

Track real-time and historical biodiesel prices across global regions. Updated monthly with market insights, drivers, and forecasts.

Biodiesel Prices June 2026

| Region | Price (USD/KG) | Latest Movement |

|---|---|---|

| Northeast Asia | 1.16 | -0.9% ↓ Down |

| Europe | 1.39 | -14.7% ↓ Down |

| South America | 1.39 | -10.3% ↓ Down |

| North America | 1.48 | -6.3% ↓ Down |

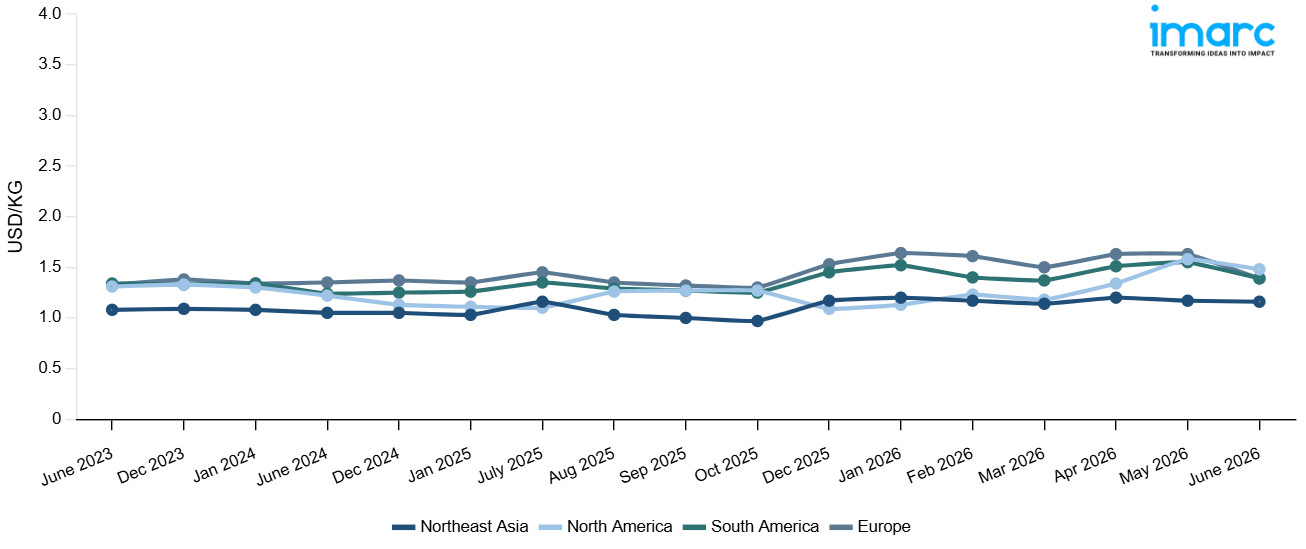

Biodiesel Price Index (USD/KG):

The chart below highlights monthly biodiesel prices across different regions.

Get Access to Monthly/Quarterly/Yearly Prices, Request Sample

Market Overview Q1 Ending March 2026

Northeast Asia: The biodiesel prices in Northeast Asia reached 1.14 USD/KG in March 2026. The downward pricing movement registered between December and March 2026 was 2.6%. Softening demand from the transportation fuel blending and industrial energy sectors reduced procurement activity and contributed to mild bearish conditions across Northeast Asian markets throughout the review period. Declining upstream vegetable oil and fatty acid methyl ester feedstock costs at regional production facilities reduced manufacturing expenses and placed modest downward pressure on prevailing regional biodiesel market rates during the quarter.

Europe: The biodiesel prices in Europe reached 1.50 USD/KG in March 2026. The downward pricing movement registered between December and March 2026 was 2.0%. The demand for biodiesel from the transportation fuel blending and renewable energy segments experienced a slight dip, which helped restrain buying activity and led to minor bearish sentiment prevailing in the European market landscape throughout the assessment period. A drop in upstream prices of raw material inputs, such as rapeseed oil and used cooking oil, at biodiesel manufacturing plants in the region helped reduce manufacturing costs and contributed to weakening the underlying price support in the quarter under review.

South America: The biodiesel prices in South America reached 1.37 USD/KG in March 2026. The downward pricing movement registered between December and March 2026 was 5.5%. Weakened demand from the transportation fuel blending and agricultural machinery sectors reduced procurement activity and contributed to bearish biodiesel market conditions across South American markets throughout the review period. Declining upstream soybean oil feedstock costs at regional production facilities reduced manufacturing expenses and eroded the cost floor supporting prevailing South American biodiesel market price levels during the quarter. Ample domestic biodiesel production from Brazilian and Argentine manufacturing facilities created a surplus supply and intensified competitive pricing pressure among regional producers.

North America: The biodiesel prices in North America reached 1.18 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 8.3%. Strong demand from the fuel blending, renewable diesel, and commercial fleets markets supported active biodiesel purchasing activities and maintained optimistic pricing trends in North American markets during the quarter under review. The rise in upstream prices for feedstocks such as soybean oil and animal fat feedstocks used in biodiesel production at local production facilities increased production costs and consistently propped up local market prices. The limited availability of local biodiesel production amid scheduled maintenance shutdowns at major biodiesel plants led to increased competition between fuel blending buyers across the region.

Market Overview Q4 Ending December 2025

Northeast Asia: The biodiesel prices in Northeast Asia reached 1.17 USD/KG in December 2025. The upward pricing movement registered between September and December 2025 was 17.0%. Strong demand from the transportation fuel blending industry, which boosted procurement activities in response to tightening government regulations requiring the use of renewable fuels throughout the region, was the main driver of the significant price increase. For local biodiesel producers, rising upstream feedstock costs for palm oil, soybean oil, and used cooking oil significantly increased production costs. Market quantities were further constrained by tighter supply conditions stemming from limited feedstock availability and capacity constraints at key transesterification facilities.

Europe: The biodiesel prices in Europe reached 1.53 USD/KG in December 2025. The upward pricing movement registered between September and December 2025 was 15.9%. The notable price appreciation was underpinned by firm regulatory demand driven by stringent renewable energy directive mandates requiring elevated biofuel blending ratios across the transportation sector. Escalating upstream rapeseed oil, used cooking oil, and waste fat feedstock costs significantly increased production expenses for regional biodiesel producers. Tightened supply conditions, driven by constrained waste oil collection volumes and capacity constraints at key production facilities, further limited regional availability.

South America: The biodiesel prices in South America reached 1.45 USD/KG in December 2025. The upward pricing movement registered between September and December 2025 was 14.2%. Strong domestic demand from the required fuel blending industry, especially since government mandated biodiesel incorporation rates maintained high consumption volumes across the region, was the main driver of the notable price gain. Due to conflicting demand from the food and export industries, rising upstream soybean oil feedstock costs led to a dramatic increase in regional firms' production costs. Available market volumes were further constrained by tighter supply due to capacity constraints at key transesterification facilities.

North America: The biodiesel prices in North America reached 1.09 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 14.2%. The significant price decline was attributed to weaker demand from the fuel blending sector amid uncertainty over regulatory conditions surrounding renewable fuel standard compliance requirements and blending credit valuations. Declining upstream soybean oil and waste cooking oil feedstock costs further eroded production cost support for domestic biodiesel manufacturers. Increased supply availability from expanded domestic production capacity and competitive import volumes exerted sustained downward pressure on prevailing market rates.

Market Overview Q3 Ending September 2025

Northeast Asia: On the supply side, feedstock availability improved modestly, putting pressure on producers to offer more competitive pricing. Logistics and shipping costs softened compared to prior quarters, easing freight burdens. Currency fluctuations also played a role, where local currencies strengthened versus the US dollar and import costs of feedstocks fell slightly, allowing downward repricing. Additionally, competition among regional producers seeking market share triggered discounting, particularly in export-oriented hubs. Regulatory or blending mandates remained largely stable, so demand support was limited. Overall, the combination of weaker downstream demand, improved supply conditions, and easing logistics pushed Northeast Asia’s biodiesel pricing lower over the quarter.

Europe: On the demand side, blending mandates and renewable fuel quotas remained stable but did not intensify, limiting strong upward pressure. Transportation and port handling costs increased slightly in Southern ports, but these were offset by strong intra-EU logistics networks. Moreover, currency stability within the eurozone moderated exchange cost volatility. Also, regulatory uncertainties, particularly debates over sustainability criteria and feedstock sourcing rules caused downstream buyers to delay incremental purchases, dampening immediate price support. Thus, constrained feedstock, cautious demand, and logistical cost interplay combined to nudge pricing modestly downward in Europe.

South America: South America saw a decline in biodiesel pricing. The region’s prices were influenced by strong local feedstock production, especially soybean oil in Brazil and Argentina, which provided ample supply and kept input costs relatively stable. Downstream demand remained moderate as transport and agricultural fuel use during the quarter did not expand sharply. On the cost side, domestic logistics, customs, and freight within South America remained manageable, especially for internal trade flows, reducing added cost burdens. Currency movements had mixed effects as some national currencies weakened slightly, raising the cost of imported inputs, but local sourcing mitigated that impact.

North America: Feedstock costs, particularly for soybean oil and used cooking oil, remained firm, enabling producers to pass on margins. Transportation and logistics costs saw moderate increases, especially for inland conveyors and rail shipment, adding marginal price pressure. Regulatory credit markets continued to provide support, creating incentives for procurement even as margins tightened. Currency effects were minimal, given the strong US dollar stability. Some seasonal demand upticks in the summer months also contributed to incremental upward pricing pressure.

Biodiesel Price Trend, Market Analysis, and News

IMARC's latest publication, “Biodiesel Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition,” presents a detailed examination of the biodiesel market, providing insights into both global and regional trends that are shaping prices. This report delves into the spot price of biodiesel at major ports and analyzes the composition of prices, including FOB and CIF terms. It also presents detailed biodiesel prices trend analysis by region, covering North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. The factors affecting biodiesel pricing, such as the dynamics of supply and demand, geopolitical influences, and sector-specific developments, are thoroughly explored. This comprehensive report helps stakeholders stay informed with the latest market news, regulatory updates, and technological progress, facilitating informed strategic decision-making and forecasting.

.webp)

Biodiesel Industry Analysis

The global biodiesel industry size reached USD 47.8 Billion in 2025. By 2034, IMARC Group expects the market to reach USD 65.5 Billion, at a projected CAGR of 3.47% during 2026-2034. The market is driven by the rising environmental awareness and demand for renewable fuels, government incentives and regulations promoting cleaner energy alternatives, and technological advancements improving production efficiency and feedstock availability.

Latest developments in the biodiesel industry:

- May 2025: Nippon Yuka Kogyo Co., Ltd. (“Nippon Yuka”), a subsidiary of the NYK Group specializing in chemical research, development, and production announced the launch of BioxiGuard, Japan’s first antioxidant formulated specifically for marine biodiesel fuel. This innovative product was developed to enhance the stability and performance of biofuels used in marine applications.

- March 2024: Bunge and Chevron collaborated to build a new oilseed processing plant next to its existing facility along the Gulf Coast in Destrehan, Louisiana. This plant will be operational in 2026, adding scale and efficiencies to Bunge Chevron Ag Renewables that will allow the company to better meet the market demands.

- June 2022: Cargill completed its first advanced biodiesel plant in Ghent, Belgium. This plant converts waste oils and residues into renewable fuel, aligning with the company’s aim to reduce GHG emissions and promote circular fuel possibilities.

Product Description

Biodiesel is a renewable and biodegradable fuel made from vegetable oils, animal fats, or recycled restaurant grease. It can be produced domestically and used in diesel engines without modification. Biodiesel offers comparable energy content to conventional diesel. Besides this, it is recognized for its superior lubricity, which can extend engine life and reduce maintenance costs, enhancing overall vehicle efficiency. With a higher flashpoint than petroleum diesel, biodiesel is safer to handle, store, and transport, reducing the risk of accidental ignitions. Its biodegradable nature ensures that it poses minimal risk to the environment in case of spills, aligning with safety and ecological considerations.

Biodiesel production promotes energy independence and reduces reliance on imported fossil fuels, thereby enhancing national energy security and supporting local economies through the creation of green jobs in agriculture and manufacturing.

Report Coverage

| Key Attributes | Details |

|---|---|

| Product Name | Biodiesel |

| Report Features | Exploration of Historical Trends and Market Outlook, Industry Demand, Industry Supply, Gap Analysis, Challenges, Biodiesel Price Analysis, and Segment-Wise Assessment. |

| Currency/Units | US$ (Data can also be provided in local currency) or Metric Tons |

| Region/Countries Covered | The current coverage includes analysis at the global and regional levels only. Based on your requirements, we can also customize the report and provide specific information for the following countries: Asia Pacific: China, India, Indonesia, Pakistan, Bangladesh, Japan, Philippines, Vietnam, Thailand, South Korea, Malaysia, Nepal, Taiwan, Sri Lanka, Hongkong, Singapore, Australia, and New Zealand Europe: Germany, France, United Kingdom, Italy, Spain, Russia, Turkey, Netherlands, Poland, Sweden, Belgium, Austria, Ireland, Switzerland, Norway, Denmark, Romania, Finland, Czech Republic, Portugal and Greece North America: United States and Canada Latin America: Brazil, Mexico, Argentina, Columbia, Chile, Ecuador, and Peru Middle East & Africa: Saudi Arabia, UAE, Israel, Iran, South Africa, Nigeria, Oman, Kuwait, Qatar, Iraq, Egypt, Algeria, and Morocco The list of countries presented is not exhaustive. Information on additional countries can be provided if required by the client. |

| Information Covered for Key Suppliers |

|

| Customization Scope | The report can be customized as per the requirements of the customer |

| Report Price and Purchase Option |

Plan A: Monthly Updates - Annual Subscription

Plan B: Quarterly Updates - Annual Subscription

Plan C: Biannually Updates - Annual Subscription

Includes: One PDF and Excel datasheet per Half, Post Purchase Analyst Support throughout the year |

| Post-Sale Analyst Support | 360-degree analyst support after report delivery |

| Delivery Format | PDF and Excel through email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report presents a detailed analysis of biodiesel pricing, covering global and regional trends, spot prices at key ports, and a breakdown of FOB and CIF prices.

- The study examines factors affecting biodiesel price trend, including input costs, supply-demand shifts, and geopolitical impacts, offering insights for informed decision-making.

- The competitive landscape review equips stakeholders with crucial insights into the latest market news, regulatory changes, and technological advancements, ensuring a well-rounded, strategic overview for forecasting and planning.

- IMARC offers various subscription options, including monthly, quarterly, and biannual updates, allowing clients to stay informed with the latest market trends, ongoing developments, and comprehensive market insights. The biodiesel price charts ensure our clients remain at the forefront of the industry.

Frequently Asked Questions About the Biodiesel Prices Report

The biodiesel prices in June 2026 were 1.16 USD/KG in Northeast Asia, 1.39 USD/KG in Europe, 1.39 USD/KG in South America, and 1.48 USD/KG in North America.

The biodiesel pricing data is updated on a monthly basis.

We provide the pricing data primarily in the form of an Excel sheet and a PDF.

Yes, our report includes a forecast for biodiesel prices.

The regions covered include North America, Europe, Asia Pacific, Middle East, and Latin America. Countries can be customized based on the request (additional charges may be applicable).

Yes, we provide both FOB and CIF prices in our report.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Inquire Before Buying

Inquire Before Buying

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Why Choose Us

IMARC offers trustworthy, data-centric insights into commodity pricing and evolving market trends, enabling businesses to make well-informed decisions in areas such as procurement, strategic planning, and investments. With in-depth knowledge spanning more than 1000 commodities and a vast global presence in over 150 countries, we provide tailored, actionable intelligence designed to meet the specific needs of diverse industries and markets.

1000

+Commodities

150

+Countries Covered

3000

+Clients

20

+Industry

Robust Methodologies & Extensive Resources

IMARC delivers precise commodity pricing insights using proven methodologies and a wealth of data to support strategic decision-making.

Subscription-Based Databases

Our extensive databases provide detailed commodity pricing, import-export trade statistics, and shipment-level tracking for comprehensive market analysis.

Primary Research-Driven Insights

Through direct supplier surveys and expert interviews, we gather real-time market data to enhance pricing accuracy and trend forecasting.

Extensive Secondary Research

We analyze industry reports, trade publications, and market studies to offer tailored intelligence and actionable commodity market insights.

Trusted by 3000+ industry leaders worldwide to drive data-backed decisions. From global manufacturers to government agencies, our clients rely on us for accurate pricing, deep market intelligence, and forward-looking insights.