Aviation Cyber Security Market Size, Share, Trends and Forecast by Solution Type, Deployment Type, Application, and Region, 2025-2033

Aviation Cyber Security Market Size and Share:

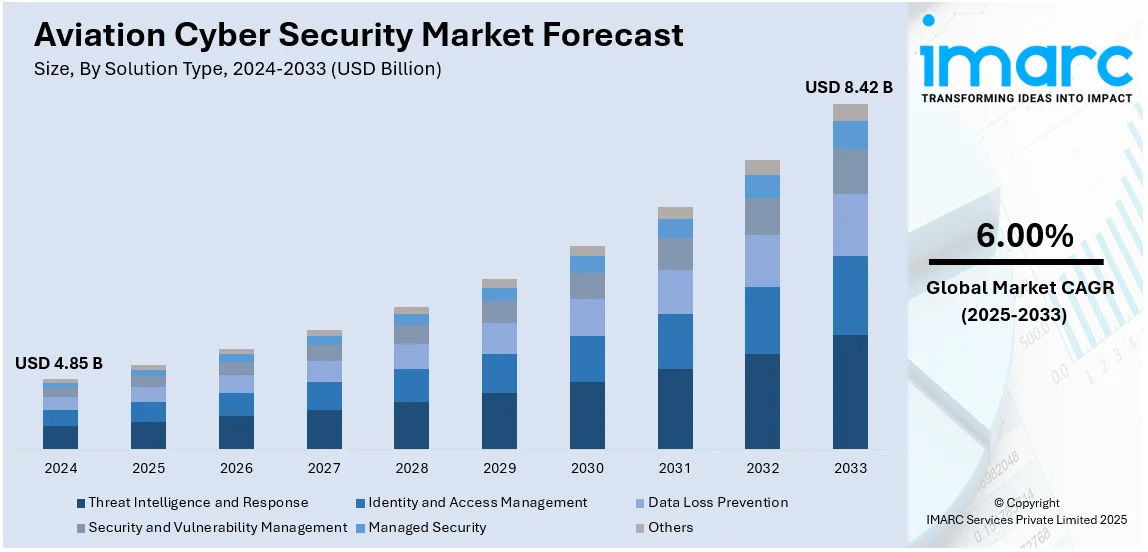

The global aviation cyber security market size was valued at USD 4.85 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 8.42 Billion by 2033, exhibiting a CAGR of 6.00% during 2025-2033. North America currently dominates the market, holding a significant market share of over 33.7% in 2024. The rising cyber threats, digital transformation, increasing adoption of AI and IoT, regulatory compliance, and increasing passenger traffic are some of the major factors fueling the aviation cyber security market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 4.85 Billion |

|

Market Forecast in 2033

|

USD 8.42 Billion |

| Market Growth Rate 2025-2033 | 6.00% |

The market for aviation cybersecurity is influenced by the increasing frequency and sophistication of cyber threats targeting airports, airlines, and air traffic control systems. As the aviation industry undergoes rapid digital transformation, the adoption of IoT, AI, and cloud-based solutions has expanded, creating a greater need for robust cybersecurity measures. Regulatory compliance, including strict government mandates from organizations like the FAA and TSA, further pushes investments in advanced security solutions. Rising passenger numbers together with airport operational automation create numerous security points that require significant data protection initiatives. Additionally, the integration of biometric authentication, blockchain, and AI-driven threat detection enhances security. Rising airline expansions, cross-border air travel, and the need for real-time monitoring also contribute to the growing demand for aviation cybersecurity solutions.

The market for aviation cybersecurity in the United States is driven by rising cyber threats targeting airlines, airports, and air traffic management systems. Increasing digitalization, IoT adoption, and cloud-based operations have expanded cybersecurity vulnerabilities, necessitating advanced protection solutions. Strict government regulations from the FAA, TSA, and DHS mandate robust cybersecurity frameworks, driving market growth. For instance, in August 2024, the US Federal Aviation Administration (FAA) announced a proposal for new regulations regarding the cyber security of airplanes and their equipment. The FAA states that the updated regulations are being implemented due to aviation equipment increasingly linking to both internal and external data networks, such as satellite communications and Internet-enabled devices. Growing passenger traffic and automated airport operations further increase the demand for data security. AI-driven threat detection, biometric authentication, and blockchain technology are increasingly used to enhance security. Additionally, the expansion of airline networks and rising defense aviation activities contribute to the need for comprehensive cybersecurity solutions.

Aviation Cyber Security Market Trends:

Rising Cyber Threats and Attacks

The increasing frequency and sophistication of cyberattacks targeting the aviation industry drive the demand for robust cybersecurity solutions. According to the International Telecommunication Union (ITU), in 2023, the security of over 8 Billion records was compromised, with approximately 68% of organizations globally experiencing a cyberattack. Airlines, airports, and air traffic management systems are prime targets for hackers attempting to disrupt operations, steal sensitive passenger data, or launch ransomware attacks. Cyber threats, including phishing, malware, and advanced persistent threats (APTs), have intensified with the digitalization of aviation infrastructure. As a result, aviation companies are investing in AI-driven threat detection, endpoint security, and real-time monitoring to prevent breaches. The rising need for proactive defense strategies fuels market growth and accelerates the adoption of cybersecurity technologies.

Growing Digital Transformation and IoT Integration

The aviation industry is undergoing rapid digital transformation, with increased adoption of IoT, cloud computing, and AI-driven automation, creating a positive aviation cyber security market outlook. Smart airports, connected aircraft, and real-time data exchange between systems enhance efficiency but also introduce new cybersecurity vulnerabilities. IoT devices used in aircraft maintenance, baggage handling, and passenger services can become entry points for cyber threats. For instance, in February 2025, The Noida International Airport (NIA) announced that it has collaborated with Kyndryl, the leading global provider of IT infrastructure services, to oversee its contemporary technology landscape and offer 24/7 assistance. Through this partnership, Kyndryl will utilize its thirty years of expertise in overseeing and modernizing airport and airline IT systems worldwide. The collaboration seeks to provide NIA with modern frameworks, innovative delivery services, and strong governance methods to guarantee smooth, technology-enhanced airport operations. To counteract these risks, aviation companies are deploying advanced cybersecurity frameworks, encryption protocols, and network segmentation. The need to secure interconnected systems and ensure uninterrupted operations is a key factor driving investments in aviation cybersecurity solutions.

Stringent Regulatory Compliance and Government Initiatives

Regulatory bodies, such as the Transportation Security Administration (TSA), the Federal Aviation Administration (FAA), and the European Union Aviation Safety Agency (EASA), have introduced strict cybersecurity guidelines for the aviation industry. Governments worldwide mandate compliance with cybersecurity frameworks to protect national security and passenger safety. New regulations require airlines and airport operators to implement comprehensive cybersecurity measures, including risk assessments, incident response protocols, and data protection strategies. Compliance with these regulations drives increased spending on cybersecurity solutions, pushing market growth. The continuous evolution of cybersecurity policies ensures that aviation stakeholders prioritize security investments. For instance, in February 2025, Thales, a worldwide leader in high technology, and Sopra Steria, a significant contributor to the European Tech industry, announced a new multiyear collaboration aimed at driving the digital transformation of the Air Traffic Management (ATM) sector in Europe. The two players will merge their industrial and digital knowledge in ATM to provide Thales’ OpenSky Platform, a secure digital platform, alongside related services to enhance sustainable aviation and modernize European ATMs. With its specialized aerospace division, Aeroline, Sopra Steria will aid Air Navigation Service Providers (ANSPs) in overcoming digital transformation obstacles.

Aviation Cyber Security Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global aviation cyber security market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on solution type, deployment type, and application.

Analysis by Solution Type:

- Threat Intelligence and Response

- Identity and Access Management

- Data Loss Prevention

- Security and Vulnerability Management

- Managed Security

- Others

Managed security stands as the largest solution type in 2024, holding around 68.6% of the market. Managed security holds the largest share of the market due to the growing complexity of cyber threats and the need for continuous monitoring and protection. Airlines, airports, and aviation authorities increasingly rely on managed security services to safeguard critical infrastructure, passenger data, and operational systems. These services provide incident response, real-time threat detection, and compliance management, reducing cybersecurity risks. Additionally, managed security providers offer expertise, advanced threat intelligence, and cost-effective solutions, making them an attractive choice for the aviation industry. As cyberattacks on aviation increase, the demand for managed security services continues to rise, ensuring comprehensive protection.

Analysis by Deployment Type:

- Cloud-Based

- On-Premises

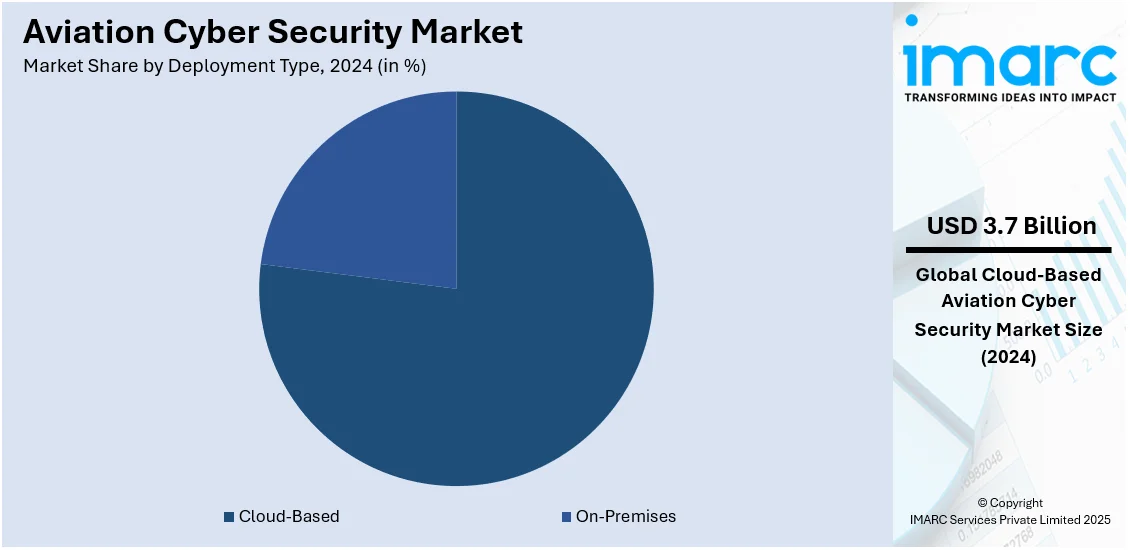

Cloud-based leads the market with around 76.8% of market share in 2024. Cloud-based solutions hold the largest share in the market due to their scalability, cost efficiency, and advanced threat detection capabilities. The aviation industry relies on real-time data processing for flight operations, passenger management, and security protocols, making cloud-based cybersecurity essential for seamless protection. These solutions offer centralized monitoring, AI-driven threat analysis, and automated incident response, enhancing security across distributed networks. Additionally, cloud-based cybersecurity enables airlines and airports to comply with stringent regulations while reducing infrastructure costs. As cyber threats grow more sophisticated, the demand for flexible, always-updated cloud security solutions continues to rise, driving market dominance.

Analysis by Application:

- Airline Management

- Air Cargo Management

- Airport Management

- Air Traffic Control Management

Airport management holds the largest share of the market due to the critical need to protect airport operations, passenger data, and air traffic systems from cyber threats. Airports handle vast amounts of sensitive information, including flight schedules, security protocols, and traveler details, making them prime targets for cyberattacks. Cybersecurity solutions in airport management safeguard critical infrastructure, communication networks, and automated systems from potential breaches. The demand for robust cybersecurity measures has grown with increasing digitalization, AI-driven security, and IoT-based airport operations. Compliance with stringent aviation security regulations further drives investment in cybersecurity, ensuring the safety and efficiency of airport management

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 33.7%. The aviation cyber security demand in North America is influenced by rising cyber threats, stringent regulatory requirements, and the rapid digitalization of the aviation industry. Growing cyberattacks on airports, airlines, and air traffic control systems necessitate advanced security solutions. The adoption of cloud-based services, IoT, and AI-driven analytics further boosts demand for cybersecurity measures. Government initiatives, such as TSA and FAA regulations, mandate strict cybersecurity compliance, encouraging investments in threat detection and response solutions. Additionally, the rise in passenger traffic and automated airport operations increases the need for robust data protection. Expanding defense and commercial aviation sectors further fuel market growth.

Key Regional Takeaways:

United States Aviation Cyber Security Market Analysis

In 2024, the United States accounted for over 91.10% of the aviation cyber security market in North America. The United States aviation cybersecurity market is primarily driven by the increasing incidence of cyber threats, stringent regulatory requirements, and the rising reliance on digital technologies in aviation operations. Airlines, airports, and air traffic control systems are becoming highly interconnected through advanced communication networks, cloud computing, and Internet of Things (IoT) devices, making them more vulnerable to cyberattacks. The rise in ransomware attacks, data breaches, and hacking incidents targeting the aviation sector is driving the demand for robust cybersecurity solutions. As such, the United States cybersecurity market is growing at a CAGR of 8.20% from 2024-2032 and is expected to reach USD 172.65 Billion by 2032, according to a report published by the IMARC Group. Regulatory bodies such as the Transportation Security Administration (TSA) and the Federal Aviation Administration (FAA) are enforcing strict cybersecurity guidelines to protect critical aviation infrastructure. The growing adoption of machine learning (ML) and artificial intelligence (AI) in aviation security is further enhancing threat detection and response capabilities. Additionally, increasing investments in secure satellite communication, aviation software, and next-generation air traffic management systems are strengthening the market. The expansion of cloud-based aviation operations and the shift toward remote aircraft monitoring and predictive maintenance are also fueling the need for advanced cybersecurity measures. As cyber threats evolve, the U.S. aviation sector is prioritizing cybersecurity solutions to safeguard passenger safety and operational integrity.

Asia Pacific Aviation Cyber Security Market Analysis

The Asia Pacific aviation cyber security market is expanding due to the growing reliance on digital infrastructure and the need to safeguard increasingly complex aviation ecosystems. Rapid urbanization and the expansion of air travel in countries such as China and India are leading to greater digital integration in airports and airlines, creating new vulnerabilities. As per industry reports, 52.9% of the population of Asia lived in urban areas in 2024, equating to about 2,545,230,547 individuals. Additionally, as airports, airlines, and air traffic control systems increasingly adopt technologies such as IoT, AI, and cloud computing, the risk of cyber threats has grown, prompting a stronger focus on cybersecurity. It has been reported that in 2021, around 4.5 million records might have been exposed in this significant security breach involving Air India. The incident included certain personal information recorded from August 2011 to February 2021. Other than this, the region's increasing integration into the global aviation supply chain further heightens the importance of safeguarding data and communication systems, driving the market growth for advanced cybersecurity solutions tailored to the aviation sector.

Europe Aviation Cyber Security Market Analysis

The Europe aviation cyber security market is witnessing rapid growth, propelled by the growing frequency and sophistication of cyber-attacks targeting the aviation sector, which has raised significant concerns about the security of systems and data. As airlines, airports, and air traffic control systems rely on digital technologies, they are becoming more vulnerable to cyber threats such as ransomware, data breaches, and hacking attempts. Among the recent cyberattacks on the aviation industry, a UK-based airline lost 9 million customer records to hackers. Additionally, the growing adoption of digital systems and the Internet of Things (IoT) in aviation operations has also expanded the attack surface, making comprehensive cybersecurity protocols essential. Furthermore, the increasing integration of cloud computing and artificial intelligence (AI) into aviation operations presents both opportunities and risks, necessitating robust cybersecurity infrastructures. However, the need for real-time threat detection and response to mitigate potential damage has driven investments in advanced security solutions like machine learning (ML) and artificial intelligence (AI) for cybersecurity. According to industry reports, the artificial intelligence market in Europe reached USD 28.6 Billion in 2024 and is projected to grow at a CAGR of 24.3% during 2025-2033. Besides this, stringent regulatory frameworks, including those set by the European Union Aviation Safety Agency (EASA), have compelled aviation stakeholders to invest in advanced cybersecurity measures to comply with new safety standards, supporting overall industry expansion.

Latin America Aviation Cyber Security Market Analysis

The Latin America aviation cyber security market is driven by the increasing digitization of aviation systems and a growing number of cyber threats. As the air travel industry in the region expands, airlines, airports, and air traffic control systems are becoming more connected, creating new vulnerabilities for cyber-attacks. For instance, during the first six months of 2024, Brazil witnessed approximately 3.6 Million foreign tourists, who generated over R$20.9 Billion for the country. Additionally, the rise in mobile technology usage and online services for booking and customer management has heightened the risk of data breaches. Governments and regulatory authorities are also strengthening cybersecurity mandates to protect vital aviation infrastructure. Moreover, the growing use of IoT and automation in aviation operations is adding complexity, increasing the need for advanced security solutions to ensure system integrity.

Middle East and Africa Aviation Cyber Security Market Analysis

The Middle East and Africa aviation cyber security market is driven by rapid technological advancements and growing air traffic in the region. For instance, according to the International Air Transport Association, in 2023, 54% of all origin-destination (O-D) flights from Saudi Arabia were due to international air travel. Moreover, about 446,000 flights were operated in the first half of 2024 in Saudi Arabia, recording a rise of 12% in comparison to the same period in 2023. Similarly, 100% of the UAE's origin-destination (O-D) departures were made by international aircraft in 2023. As aviation infrastructure becomes more interconnected with digital systems, the risk of cyber threats increases, prompting a greater need for robust security solutions. The region's significant investment in smart airports, cloud computing, and IoT technologies is also expanding attack surfaces, propelling the need for enhanced cybersecurity measures.

Competitive Landscape:

The aviation cybersecurity market is highly competitive, with key players focusing on advanced threat detection, AI-driven security, and cloud-based solutions. Major companies such as Raytheon Technologies, Thales Group, Honeywell, IBM, and Cisco dominate the market, offering integrated cybersecurity solutions for airlines, airports, and air traffic management systems. Emerging startups are leveraging AI, blockchain, and machine learning to enhance cybersecurity resilience. Regulatory compliance, government contracts, and strategic partnerships drive market dynamics. Increasing cyber threats, digital transformation, and the adoption of IoT in aviation further intensify competition. Companies invest heavily in research, innovation, and managed security services to maintain a competitive edge.

The report provides a comprehensive analysis of the competitive landscape in the aviation cyber security market with detailed profiles of all major companies, including:

- Airbus SE

- BAE Systems Plc

- Booz Allen Hamilton Holding

- Cisco Systems Inc.

- Fortinet Inc.

- General Dynamics Corporation

- Honeywell International Inc.

- International Business Machines Corporation

- Lockheed Martin Corporation

- Palo Alto Networks Inc.

- SITA N.V.

- Thales Group

- Unisys Corporation

Latest News and Developments:

- February 2025: The Stress Aerospace and Defense (StressAD), a division of Stress Engineering Services Inc. (SES), attained the Cybersecurity Maturity Model Certification (CMMC) Level 2. This accreditation highlights the dedication of StressAD to protecting Controlled Unclassified Information (CUI) and upholding the strictest cybersecurity regulations in the government, military, and aviation industries.

- February 2025: The AI-powered cybersecurity education and instruction platform, Meta1st, revealed that it will fully assist the aerospace sector in fulfilling the Part-IS regulatory standards set forth by the European Aviation Safety Agency (EASA). The Part-IS, which is scheduled to go into force in October 2025, calls for substantial information security protocols with a significant emphasis on security knowledge and instruction in order to reduce cyber risks and safeguard aviation operations.

- January 2025: SITA, a leading international provider of aviation technologies, entered into a strategic partnership with Palo Alto Networks, a global pioneer in cybersecurity, in order to provide robust cybersecurity solutions for essential airport functions. SITA's CyberSOC will be used for administration and logistics. This integration of Palo Alto Networks' AI-driven cybersecurity technologies into SITA's CyberSecurity assortment represents a significant turning point for the company.

- September 2024: SITA launched the SITA Managed NAC (Network Access Control), a new cybersecurity strengthening system. This cutting-edge technology is intended to protect the essential infrastructure of airlines and airports while meeting the increasing need for safe and dependable accessibility for consumers. With extra levels of identity verification and network division, SITA Managed NAC provides unmatched safety for Local Area Networks (LAN), as well as Wireless LAN traffic.

- September 2024: Airbus Defence Space successfully acquired Infodas, a provider of IT and cybersecurity solutions based in Germany. This acquisition represents a significant step forward for Airbus, supporting the company’s goal of expanding its cybersecurity offerings for European and international clients.

Aviation Cyber Security Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solution Types Covered | Threat Intelligence and Response, Identity and Access Management, Data Loss Prevention, Security and Vulnerability Management, Managed Security, Others |

| Deployment Types Covered | Cloud-Based, On-Premises |

| Applications Covered | Airline Management, Air Cargo Management, Airport Management, Air Traffic Control Management |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Airbus SE, BAE Systems Plc, Booz Allen Hamilton Holding, Cisco Systems Inc., Fortinet Inc., General Dynamics Corporation, Honeywell International Inc., International Business Machines Corporation, Lockheed Martin Corporation, Palo Alto Networks Inc., SITA N.V., Thales Group, Unisys Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aviation cyber security market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global aviation cyber security market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aviation cyber security industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The aviation cyber security market was valued at USD 4.85 Billion in 2024.

The aviation cyber security market is projected to exhibit a CAGR of 6.00% during 2025-2033, reaching a value of USD 8.42 Billion by 2033.

The aviation cyber security market is driven by rising cyber threats, digital transformation, increasing passenger traffic, and stringent regulatory requirements. The adoption of AI, cloud computing, and IoT in aviation necessitates robust security solutions. Government initiatives, growing airline networks, and automation in airport operations further fuel the demand for advanced cybersecurity measures and threat protection.

North America currently dominates the aviation cyber security market due to rising cyber threats, digital transformation, regulatory compliance, AI adoption, cloud security, IoT integration, government initiatives, airline expansion, and automation.

Some of the major players in the aviation cyber security market include Airbus SE, BAE Systems Plc, Booz Allen Hamilton Holding, Cisco Systems Inc., Fortinet Inc., General Dynamics Corporation, Honeywell International Inc., International Business Machines Corporation, Lockheed Martin Corporation, Palo Alto Networks Inc., SITA N.V., Thales Group and Unisys Corporation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)