Automotive Upholstery Market Size, Share, Trends and Forecast by Upholstery Materials, Fabric Type, Vehicle Type, Sales Channel, Application, and Region, 2026-2034

Global Automotive Upholstery Market Size, Share, Trends & Forecast (2026-2034)

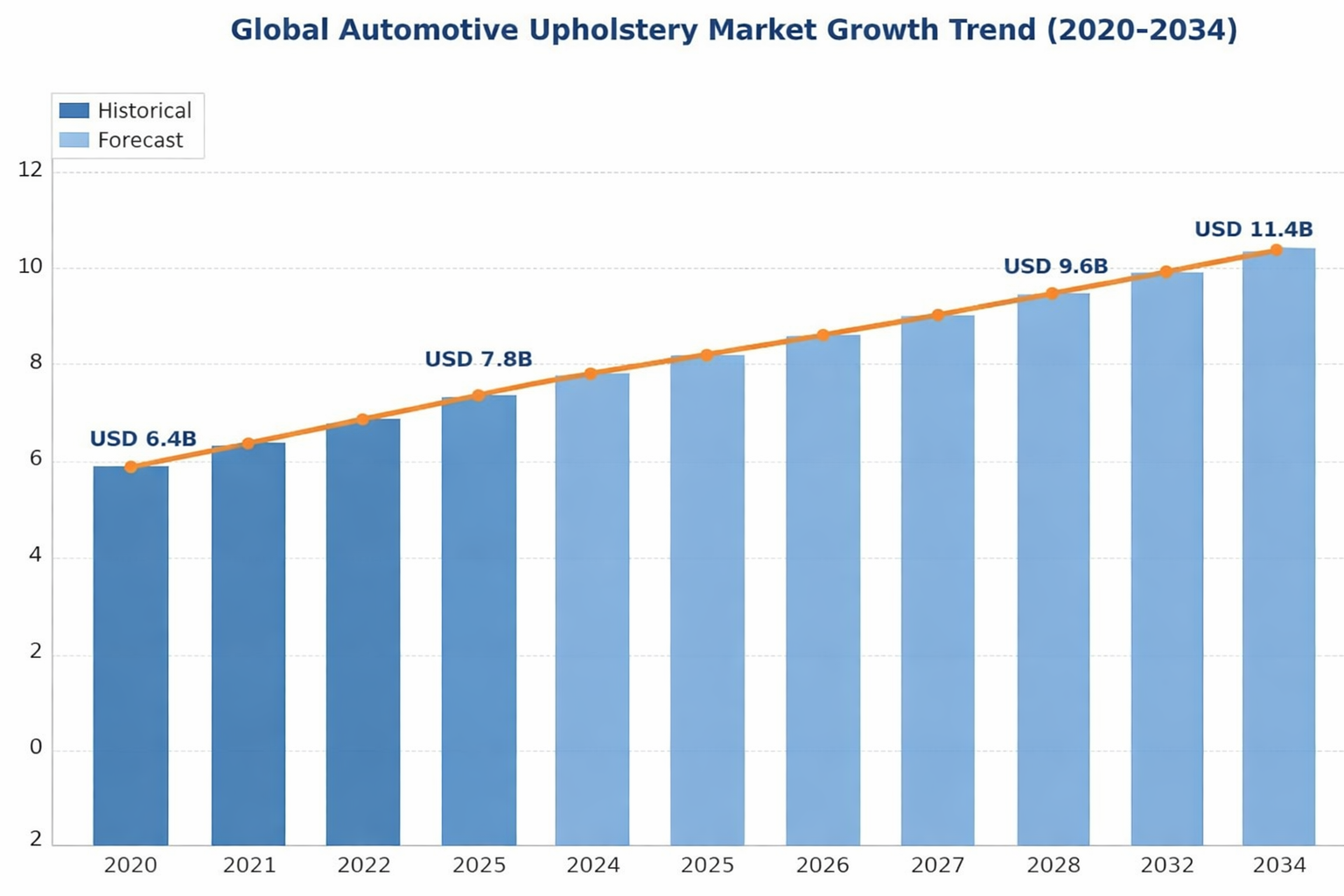

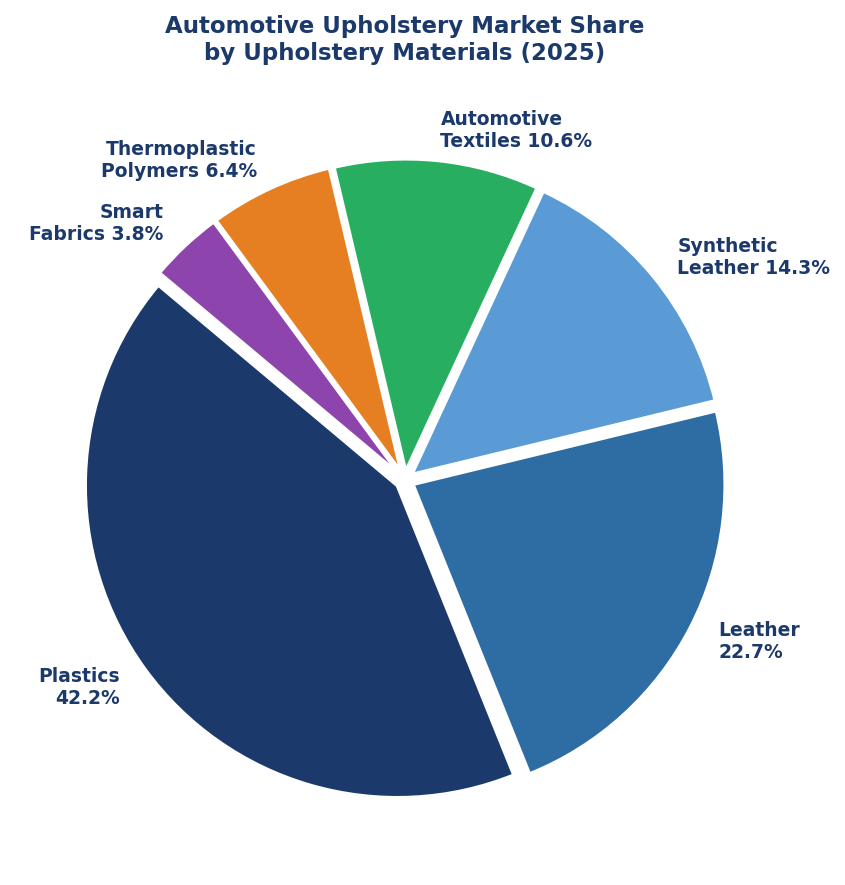

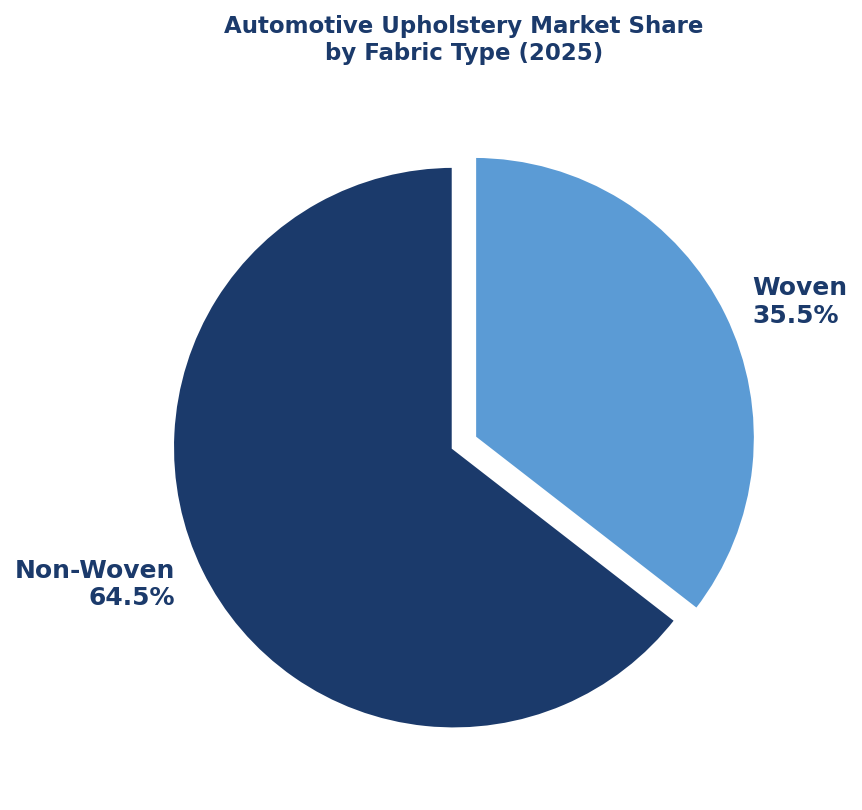

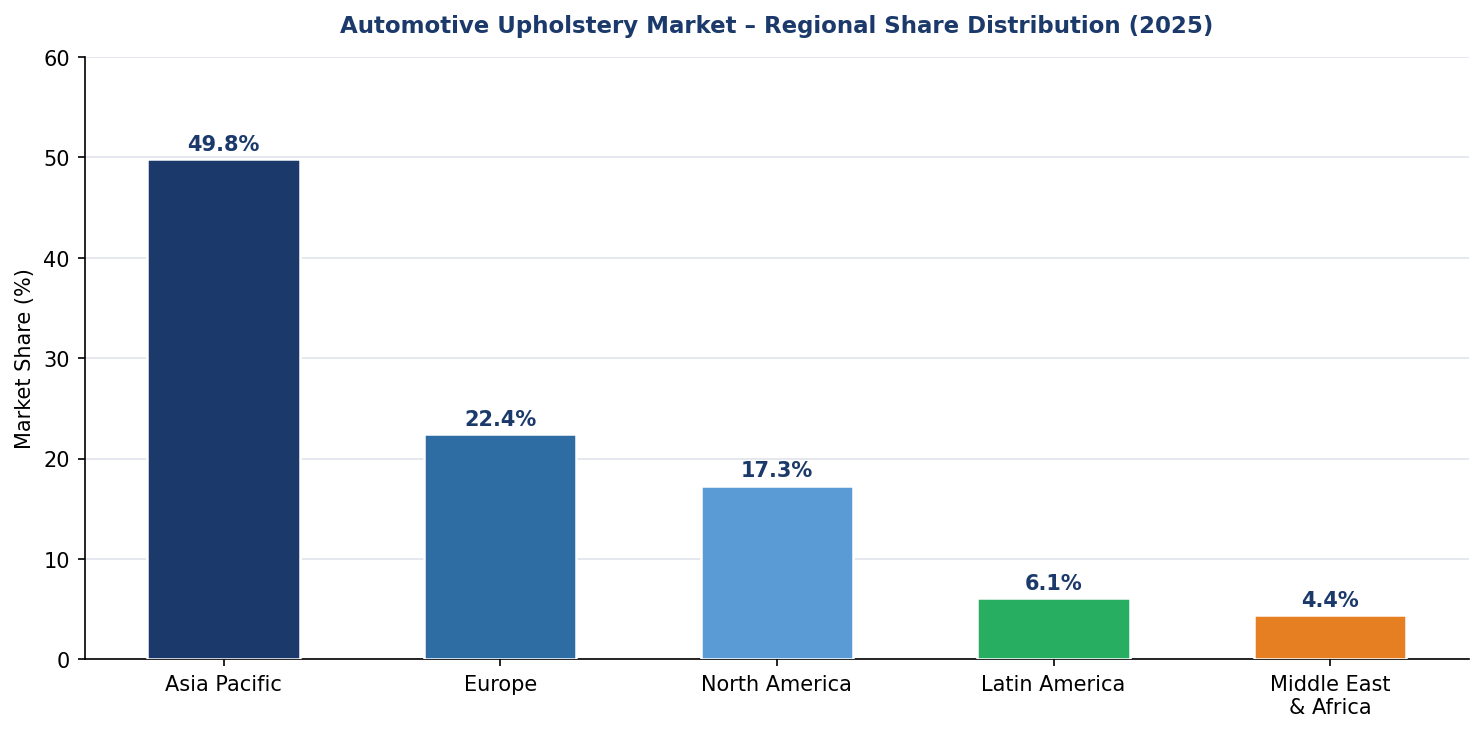

The global automotive upholstery market size was valued at USD 7.8 Billion in 2025 and is projected to reach USD 11.4 Billion by 2034, exhibiting a CAGR of 4.15% during the forecast period 2026-2034. Expanding vehicle production volumes, rising consumer preference for premium and customized vehicle interiors, and rapid adoption of sustainable and lightweight upholstery materials are the primary forces driving market growth. Plastics dominate upholstery materials with a 42.2% share in 2025, while non-woven fabric type leads at 64.5%. Asia Pacific commands 49.8% of global revenue in 2025, driven by China's surging automobile output and India's growing premium vehicle segment.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.8 Billion |

|

Forecast Market Size (2034) |

USD 11.4 Billion |

|

CAGR (2026-2034) |

4.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (49.8% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~5.3%) |

|

Leading Upholstery Material |

Plastics (42.2%, 2025) |

|

Leading Fabric Type |

Non-Woven (64.5%, 2025) |

The chart below illustrates the global automotive upholstery market growth trajectory from 2020 through 2034, contrasting consistent historical expansion against a sustained forecast curve powered by EV interior premiumization, smart fabric adoption, and rising luxury vehicle penetration across Asia Pacific and Europe.

Figure 1: Global Automotive Upholstery Market Growth Trend (2020–2034)

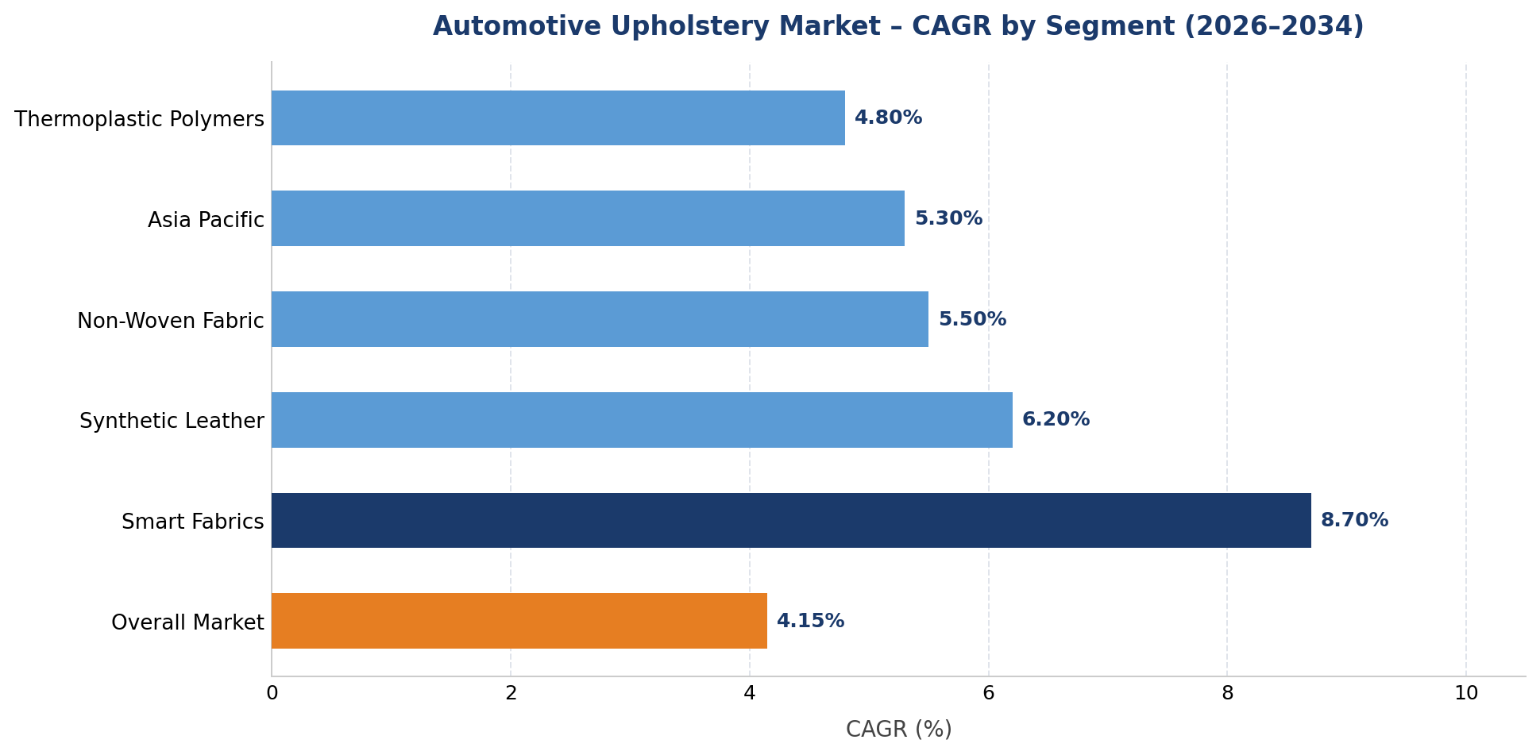

Segment-level CAGR comparisons highlight Smart Fabrics and Synthetic Leather as the two fastest-growing sub-categories within the global automotive upholstery industry through 2034, reflecting a structural shift toward technologically advanced and sustainable interior materials.

Figure 2: CAGR Comparison – Automotive Upholstery Market Segments (2026–2034)

Executive Summary

The global automotive upholstery market is undergoing a fundamental transformation driven by the convergence of premiumization, electrification, and sustainability imperatives across the global automotive sector. Valued at USD 7.8 Billion in 2025, the market is forecast to reach USD 11.4 Billion by 2034 at a CAGR of 4.15%. Global vehicle production surpassed 92 million units in 2024 (OICA), and each incremental vehicle unit represents a baseline upholstery procurement demand, establishing a stable growth floor for the market through the forecast period.

Plastics command the dominant material share at 42.2% in 2025, driven by their cost-effectiveness, design flexibility, and proven durability in mass-market passenger car applications. Leather, at 22.7%, continues to anchor the premium and luxury vehicle segment, where consumer willingness to pay a premium for authentic hide-based upholstery remains strong in Western Europe, North America, and the luxury tier of Asia Pacific markets. Synthetic Leather at 14.3% is the fastest-evolving material sub-segment, benefitting from both cost and sustainability advantages over genuine leather.

Non-woven fabric type dominates at 64.5% in 2025, underpinned by automotive OEMs' preference for lightweight, cost-efficient, and recyclable materials that support vehicle weight reduction targets. Asia Pacific leads with 49.8% global revenue share in 2025, anchored by China's position as the world's largest vehicle production market at 34 million units annually. Europe at 22.4% and North America at 17.3% follow, with both regions characterized by premium vehicle penetration and stringent sustainability standards shaping upholstery material evolution through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Material Segment |

Plastics – 42.2% share (2025) |

|

Second Material Segment |

Leather – 22.7% share (2025) |

|

Leading Fabric Type |

Non-Woven – 64.5% share (2025) |

|

Leading Region |

Asia Pacific – 49.8% revenue share (2025) |

|

Second Region |

Europe – 22.4% revenue share (2025) |

|

Top Companies |

Adient, Lear Corp., Toyota Boshoku, Faurecia (Forvia), Grupo Antolin |

|

Market Opportunity |

Smart Fabrics at ~8.7% CAGR; EV interior premiumization; sustainable bio-based materials |

Key analytical observations supporting the above data:

- Plastics' 42.2% dominance in 2025: reflects the cost-price optimization imperative among mass-market OEMs globally, particularly in Asia Pacific and Latin America where entry-level to mid-range vehicles constitute the bulk of production volumes.

- Leather at 22.7%: sustains its position as the benchmark luxury upholstery material, with premium OEMs such as BMW, Mercedes-Benz, and Lexus standardizing genuine leather across flagship model lines as a key brand differentiation element.

- Non-Woven dominance at 64.5%: is structurally supported by its lightweight properties – typically 20-35% lighter than woven alternatives – helping OEMs meet tightening vehicle weight and fuel economy standards across both ICE and EV platforms.

- Asia Pacific's 49.8% revenue leadership: is underpinned by China's 34 million annual vehicle production output, India's rapidly expanding automotive sector growing at approximately 7-9% annually, and ASEAN markets' surging vehicle ownership rates.

- Smart Fabrics at 3.8% in 2025: represent the highest-growth frontier, incorporating heated/ventilated seat functions, biometric sensor integration, and self-cleaning nano-coatings – positioning this segment for ~8.7% CAGR through 2034 as EV platforms create premium specification demand.

- The aftermarket upholstery segment: is experiencing accelerated growth in North America and Europe, with Katzkin Leather and Sage Automotive Interiors leading customization-driven demand from vehicle owners seeking post-sale interior upgrades.

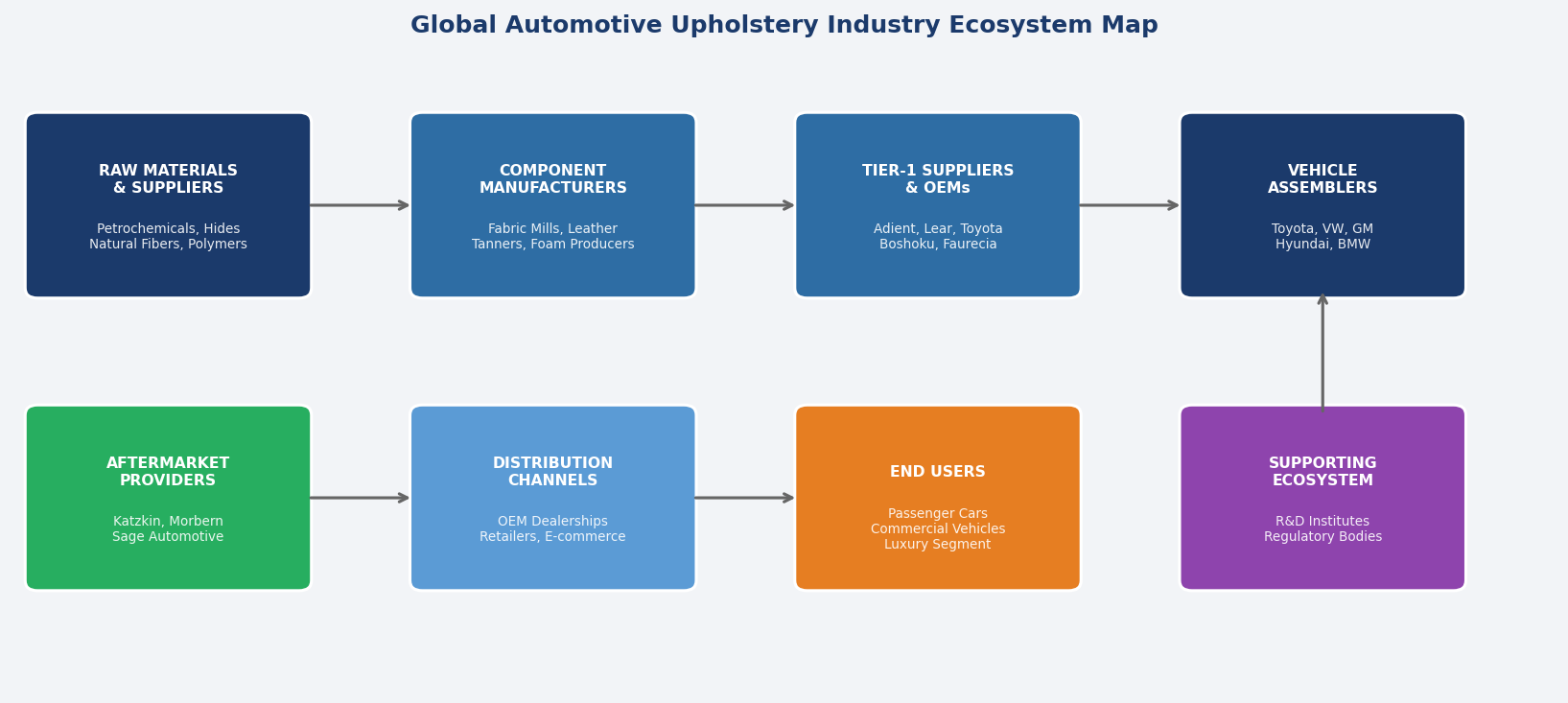

Global Automotive Upholstery Market Overview

Automotive upholstery encompasses all interior fabric, leather, polymer, and composite material surfaces within a vehicle cabin, including seat covers, headliners, door panel trims, floor carpeting, center console covers, and roof linings. Modern automotive upholstery serves dual functional and aesthetic purposes – providing occupant comfort, thermal management, noise insulation, and structural protection while simultaneously defining the interior design language that influences vehicle purchasing decisions across consumer segments.

Applications span passenger cars, light commercial vehicles, heavy-duty trucks, buses, and premium recreational vehicles, with segment-specific upholstery specifications varying significantly between mass-market economy vehicles and ultra-premium models. The ecosystem involves chemical feedstock producers, fabric mills and tanneries, Tier-1 automotive interior suppliers, OEM vehicle assemblers, and a substantial aftermarket channel serving vehicle owners seeking interior customization.

Macroeconomic enablers include global vehicle production exceeding 92 million units in 2024 (OICA), rising middle-class vehicle ownership in emerging markets, and the accelerating EV transition driving demand for premium digital-era interior experiences that elevate upholstery specification standards across vehicle price bands.

Figure 3: Global Automotive Upholstery Industry Ecosystem Map

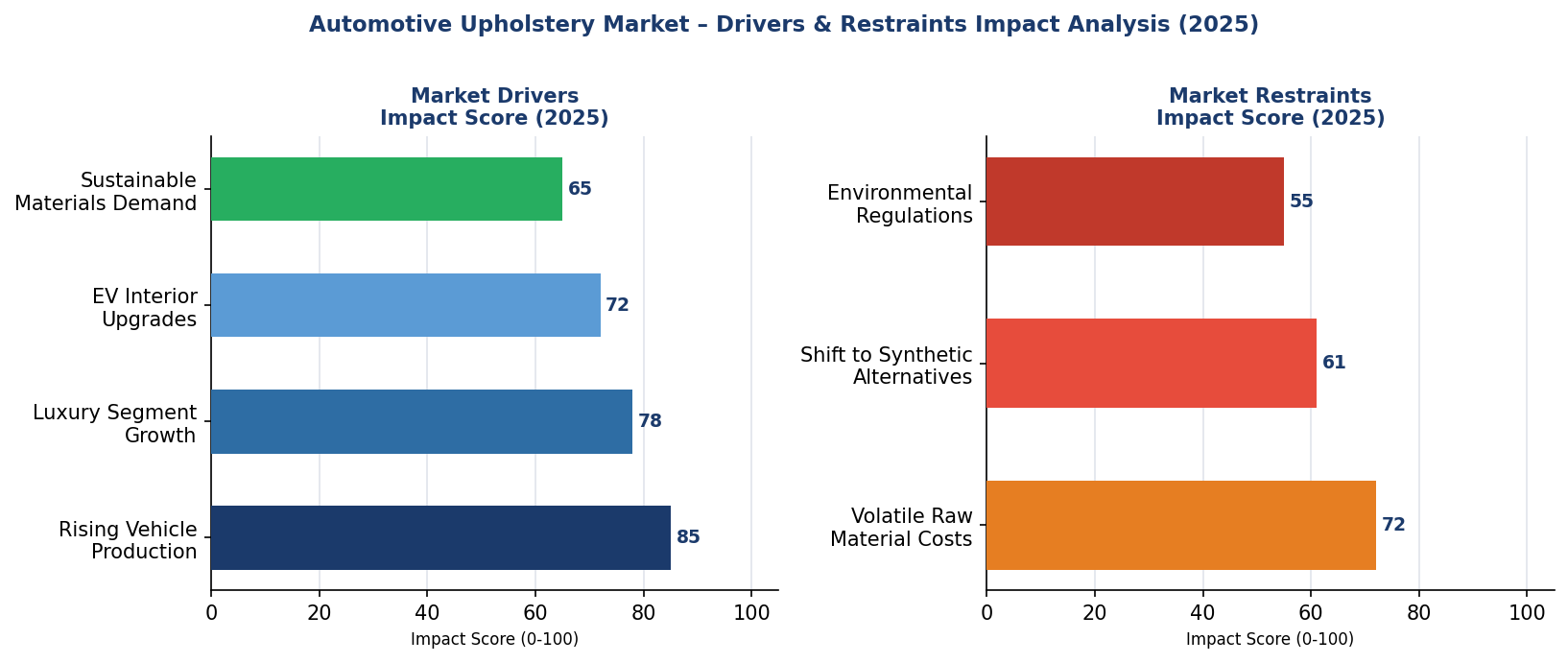

Market Dynamics

Figure 4: Automotive Upholstery Market – Drivers & Restraints Impact Analysis (2025)

Market Drivers

- Rising Global Vehicle Production and Sales: Global vehicle production surpassed 92 million units in 2024 (OICA), creating a structurally large and stable demand base for automotive upholstery materials and components. With China accounting for 34 million units and India projected to become the world's third-largest vehicle market by 2026, the Asia Pacific demand engine remains the dominant growth vector. Each new vehicle manufactured requires a complete set of upholstery materials valued at USD 250–1,200 per vehicle depending on segment and specification.

- Luxury and Premium Vehicle Segment Expansion: Global luxury vehicle sales reached approximately 2.5 million units in 2024, with BMW, Mercedes-Benz, Audi, and Lexus leading volumes. Premium vehicles typically command upholstery material costs of USD 800–2,500 per vehicle versus USD 150–350 for economy models, generating disproportionately high market value per unit. The luxury segment is growing at approximately 6-8% annually, outpacing overall vehicle market growth rates.

- EV Platform Interior Premiumization: Electric vehicle adoption – with global EV sales exceeding 17 million in 2024 (IEA) – is creating a structural upholstery market upgrade cycle. EV cabins, freed from ICE mechanical constraints, are being redesigned with lounge-style seating architectures, expanded material specifications, and premium sustainable upholstery options, increasing upholstery content value per vehicle by approximately 15-25% versus equivalent ICE models.

- Growing Demand for Sustainable and Bio-based Materials: Tightening EU End-of-Life Vehicle (ELV) regulations, automotive OEM sustainability commitments including BMW's i Vision Circular concept and Volkswagen's net-zero 2050 targets, and growing consumer environmental awareness are driving accelerating adoption of recycled polyester, plant-based leather alternatives, and bio-polymer upholstery materials.

Market Restraints

- Volatile Raw Material Costs: Automotive upholstery materials are exposed to commodity price volatility across multiple input categories – crude oil-derived polymers and synthetic fibers, cattle hide prices for genuine leather, and cotton and natural fiber prices for textile products. Brent crude oil price fluctuations of ±30-40% between 2022-2024 directly impacted polymer-based upholstery input costs, compressing Tier-1 supplier margins.

- Competitive Substitution by Synthetic Alternatives: The rising quality and declining cost premium of synthetic leather (PU leather, vegan leather) is creating substitution pressure against genuine leather in mid-range vehicle segments. As synthetic alternatives improve in texture, durability, and perceived quality, leather's 22.7% market share faces structural erosion, particularly in environmentally conscious European and premium Asian consumer segments.

- Complex Environmental Compliance Requirements: The EU REACH regulation, the US Consumer Product Safety Improvement Act, and evolving global VOC emission standards for vehicle interior materials impose significant R&D and compliance costs on upholstery manufacturers, particularly smaller regional suppliers who lack the scale to absorb certification expenditures.

Market Opportunities

- Smart Fabric Integration in Next-Generation Vehicles: Smart fabrics incorporating conductive fibers for seat heating/ventilation control, pressure-sensitive biometric monitoring, and electroluminescent design elements represent a premium technology frontier with projected ~8.7% CAGR through 2034. Automotive OEMs are actively developing smart upholstery applications – BMW's i Vision Dee concept demonstrated full-cabin smart fabric integration with color-changing capabilities.

- Aftermarket Customization Market Expansion: The global automotive aftermarket upholstery segment is estimated to exceed USD 3.5 Billion by 2030, driven by personalization trends in North America and Europe, and rapidly growing custom interior modification culture in China and Southeast Asia. Companies such as Katzkin Leather report 20%+ annual revenue growth driven by vehicle owner demand for factory-quality leather upgrades.

- Commercial Vehicle Fleet Modernization: Long-haul trucks, passenger buses, and fleet commercial vehicles represent a structurally underpenetrated upholstery opportunity. Driver comfort, durability, and hygiene requirements for commercial vehicles are driving premium upholstery specification upgrades in European and North American fleet markets.

Market Challenges

- Supply Chain Complexity and Regional Concentration Risks: Automotive upholstery supply chains involve geographically distributed raw material sources, processing facilities, and assembly operations, creating vulnerability to disruption. The COVID-19 period demonstrated how semiconductor shortages and logistics disruptions cascaded through automotive supply chains, indirectly impacting upholstery demand by constraining vehicle production.

- Technical Complexity of Smart Material Integration: Integrating electronic components and sensor systems into upholstery fabrics requires precise coordination between textile engineers, automotive electronics specialists, and OEM engineering teams, creating long development cycles of 24-36 months and significant NRE cost barriers for smaller manufacturers.

- Balancing Cost Efficiency with Sustainability Requirements: OEM procurement teams face competing pressures to reduce material costs while simultaneously meeting increasingly stringent sustainability certifications. Bio-based and recycled content materials typically carry 15-40% cost premiums versus conventional alternatives, requiring phased adoption strategies aligned with OEM cost-down schedules.

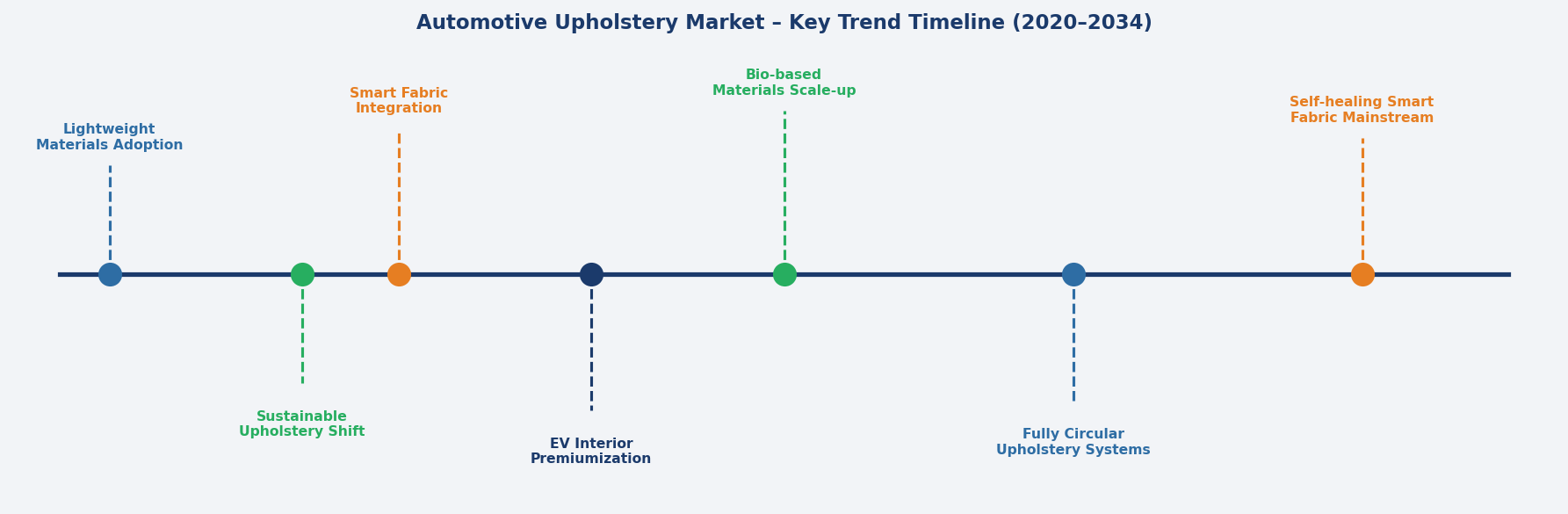

Emerging Market Trends

Figure 5: Automotive Upholstery Market – Key Trend Timeline (2020–2034)

1. Sustainable and Bio-Based Material Adoption

The automotive industry is undergoing a fundamental materials shift toward sustainable upholstery alternatives. BMW's deployment of KELO leather alternative and Volkswagen's commitment to increase recycled materials content to 40% in new models by 2030 are landmark benchmarks reshaping supplier material portfolios. Plant-based leathers derived from cactus (Desserto), apple waste, and mushroom mycelium are transitioning from concept to production deployment, with multiple luxury OEMs committing to animal-free interior programs by 2028–2030.

2. Smart Fabric and Embedded Technology Integration

Smart fabrics embedding sensors, heating elements, and electronic functionality directly into upholstery materials represent the most significant technology frontier in automotive interiors. Seiren Co., Ltd.'s "Viscotecs" electric heating fabric technology and Sage Automotive Interiors' advanced sensor-integrated seat covers are production-stage examples. The global smart textile market, valued at USD 5.6 Billion in 2023, is growing at ~26% CAGR, with automotive interiors identified as a primary growth application driving investment.

3. Lightweight Material Adoption Driven by EV Weight Targets

EV range optimization is creating powerful demand for lightweight upholstery materials. Every 100 kg of vehicle weight reduction extends EV range by approximately 6-10 km, creating strong OEM economic incentive to specify lightweight non-woven fabrics and thermoplastic polymer components over heavier traditional materials. Non-woven fabrics are lighter than woven equivalents and leather, making them the preferred upholstery material choice for BEV platform optimization strategies.

4. Premiumization and Interior Personalization Trends

Consumer demand for highly personalized vehicle interiors is expanding upholstery material diversity and customization optionality at OEM level. Mercedes-Benz's designo custom order program, BMW's Individual customization service, and Rolls-Royce's Bespoke program each report growing take rates exceeding 30-40% of orders in key markets. Chinese OEM NIO's "Second Living Room" interior philosophy, emphasizing premium comfort materials and customization, is setting new interior specification benchmarks for the broader industry.

5. Circular Economy and End-of-Life Material Recovery

The EU's End-of-Life Vehicle (ELV) Regulation revision requires 25% recycled content in new vehicles by 2030, directly targeting upholstery materials. Recaro's closed-loop seat material recycling program and Adient's ICON program developing take-back and recycling infrastructure for automotive upholstery are industry reference initiatives. Chemical recycling technologies are advancing to enable high-quality polyester fiber recovery from end-of-life upholstery, supporting circular material supply chains.

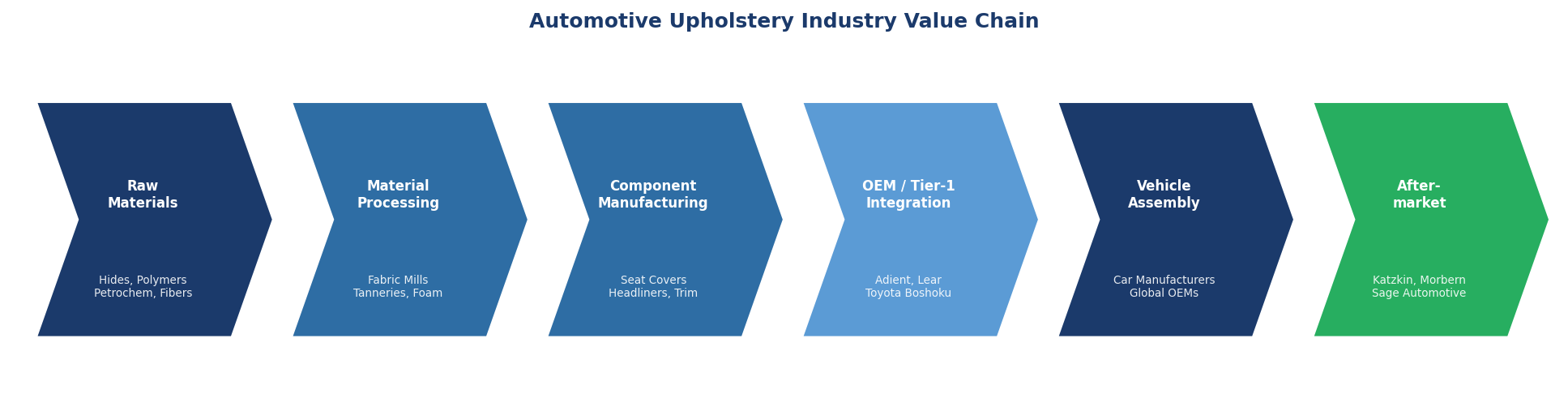

Industry Value Chain Analysis

The automotive upholstery value chain spans six integrated stages from raw material extraction through end-consumer vehicle delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements that shape the competitive landscape for market participants.

|

Stage |

Key Players / Examples |

|

Raw Materials & Chemicals |

Petrochemical producers (BASF, Dow Chemical), cattle hide suppliers, natural fiber farms, and polymer resin producers including Lanxess and Covestro |

|

Fabric Processing & Tanning |

Freudenberg Performance Materials, Borgers SE & Co. KGaA, specialised tanneries (Midland Leather), and foam producers (Recticel, Vitafoam) |

|

Component Manufacturing |

Acme Mills, Seiren Co. Ltd, Morbern, MarvelVinyls, The Haartz Corporation, Martur Automotive Seating Systems |

|

Tier-1 Supplier Integration |

Adient PLC, Lear Corporation, Toyota Boshoku Corporation, Faurecia (Forvia SE), Grupo Antolin Irausa S.A. |

|

OEM Vehicle Assembly |

Toyota, Volkswagen Group, GM, Stellantis, Hyundai-Kia, BYD, Ford, BMW Group, Mercedes-Benz, Honda |

|

Aftermarket & End Users |

Katzkin Leather Inc., Sage Automotive Interiors, Morbern (aftermarket), vehicle owners, fleet operators, customization shops |

Tier-1 suppliers occupy the highest strategic value position in the automotive upholstery value chain, integrating materials, components, and engineering into turnkey seat and interior systems. However, OEMs are increasingly internalizing design and material specification capabilities to reduce Tier-1 dependency and capture greater value from premium interior differentiation, particularly in the luxury and EV segments.

Figure 6: Automotive Upholstery Industry Value Chain

Technology Landscape in the Automotive Upholstery Industry

Advanced Material Technologies

Thermoplastic polyurethane (TPU) and thermoplastic elastomer (TPE) materials are replacing conventional PVC in automotive upholstery applications, offering superior flexibility, UV resistance, and recyclability. BASF's Elastollan TPU and Covestro's Desmopan range are widely adopted in premium OEM specifications. Bio-based TPU variants incorporating bio-polyols derived from plant oils are entering production deployment, supported by EU Renewable Raw Materials directives.

Smart Fabric and E-Textile Innovation

Conductive fiber integration enabling in-seat heating, ventilation, and biometric monitoring is the most commercially advanced smart upholstery technology. Heated seat penetration has reached approximately 65% in European vehicles and 45% in North American vehicles in 2024, creating a mature baseline for sensor-integrated seat fabric upgrades. Capacitive sensing fabrics for occupant detection (replacing traditional pressure mats) and gesture control integration represent the next-generation development frontier.

Surface Treatment and Protective Coating Technologies

Nano-coating and hydrophobic surface treatment technologies, including Crypton's performance fabric technology and Nano-Care's nanotechnology fabric treatment, are being integrated into automotive upholstery to enhance stain resistance, antimicrobial protection, and longevity. These treatments extend upholstery service life by an estimated 2-3 vehicle lifecycle years, reducing total cost of ownership for fleet operators and premium vehicle owners.

Sustainable and Circular Material Technologies

Chemical recycling technologies, including pyrolysis for polyester fiber recovery and enzymatic leather decomposition, are enabling closed-loop upholstery material systems. Renault's commitment to 33% recycled content in the Scenic E-Tech's interior and BMW's deployment of ECONYL regenerated nylon from ocean waste in vehicle interiors represent production-scale circular material implementations. Algae-based polyurethane foams and mycelium leather (Bolt Threads' Mylo) are advancing through OEM qualification testing.

Market Segmentation Analysis

By Upholstery Materials

Plastics command a 42.2% majority share in 2025, reflecting the material's dominance across mass-market vehicle interior applications including door panels, instrument panel cladding, and seat structural components. The plastics segment benefits from design flexibility through injection molding, cost efficiency at scale, and continuous material innovation enabling soft-touch and premium-feel plastic surfaces at economical price points. OEM adoption of PP, ABS, and PC-ABS compounds is near-universal in the USD 15,000–35,000 vehicle segment that constitutes the largest global sales volume tier.

Figure 7: Automotive Upholstery Market Share by Upholstery Materials (2025)

Leather maintains a 22.7% market share in 2025, driven by premium and luxury vehicle segments where genuine leather remains the benchmark interior quality indicator. Leather's share is projected to face gradual compression through 2034 as synthetic leather and bio-based alternatives capture mid-range market share, though luxury-grade leather demand in the USD 50,000+ vehicle segment is expected to remain resilient. Synthetic Leather at 14.3% is the fastest-growing traditional material segment, benefitting from vegan consumer preferences, sustainability commitments, and a 25-35% cost advantage over genuine leather at equivalent quality grades.

Automotive Textiles at 10.6% serve primarily headliner, carpet, and door insert applications, with performance textiles incorporating Crypton antimicrobial and fluid resistance treatments gaining traction in commercial vehicle and family SUV segments. Thermoplastic Polymers at 6.4% are growing driven by EV weight reduction imperatives, with injection-molded TPE components replacing traditional PVC and fabric laminates in cost-sensitive applications. Smart Fabrics at 3.8%, though smallest in current share, represent the highest growth trajectory at ~8.7% CAGR through 2034.

By Fabric Type

Non-Woven fabric type dominates at 64.5% in 2025, underpinned by automotive OEMs' structural preference for lightweight, cost-efficient, and versatile non-woven materials. Non-woven fabrics require less energy to produce than woven equivalents, are more amenable to automated high-volume manufacturing, and offer superior acoustic insulation properties when used in headliner and floor carpet applications. The material's compatibility with recycled fiber inputs supports OEM sustainability commitments.

Figure 8: Automotive Upholstery Market Share by Fabric Type (2025)

Woven fabric type at 35.5% in 2025 maintains its position in premium seat fabric applications where woven patterns, richer tactile quality, and superior abrasion resistance justify the higher material cost. European luxury OEMs and Japanese vehicle brands with strong textile heritage – including Toyota's premium Lexus line and Honda's Acura models – continue to specify high-quality woven seat textiles as standard or optional equipment in premium trim levels.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Companies |

|

Asia Pacific |

49.8% |

China vehicle output, India EV expansion, ASEAN auto growth, premium customization trend |

Toyota Boshoku, Seiren Co., Martur, local Chinese OEM suppliers |

|

Europe |

22.4% |

Luxury OEM premiumization, ELV sustainability mandates, BMW/VW/Mercedes material R&D |

Borgers SE, Grupo Antolin, Faurecia, Adient Europe |

|

North America |

17.3% |

EV interior upgrades, aftermarket customization, F-150/SUV premium trim demand |

Lear Corp., Katzkin Leather, Sage Automotive, Acme Mills |

|

Latin America |

6.1% |

Brazil/Mexico vehicle production growth, entry-level vehicle plastic demand |

Local Tier-2 suppliers, Faurecia Brazil, Adient Mexico |

|

Middle East & Africa |

4.4% |

GCC luxury vehicle adoption, Saudi Vision 2030 mobility, South Africa auto sector |

International Tier-1 subsidiaries, regional distributors |

Asia Pacific commands 49.8% of global revenue in 2025 – the most dominant regional position in the automotive upholstery market globally. China's cumulative vehicle production and sales in 2024 reached 31.282 million and 31.436 million units, representing year-on-year growth of 3.7% and 4.5%, respectively, according to data from the China Association of Automobile Manufacturers (CAAM). Both figures hit new records, maintaining volumes above 30 million units. Also, battery-electric vehicles (BEVs) accounted for 60% of China's total NEV sales in 2024, indicating a 10.4 percentage point decline from 2023. Meanwhile, plug-in hybrid electric vehicles (PHEVs) grew rapidly to account for 40% of the total volume. The Chinese domestic EV boom is directly driving premium upholstery specification upgrades as NIO, Li Auto, BYD's Han and Seal models, and XPeng compete on interior quality as a primary consumer choice differentiator.

Figure 9: Automotive Upholstery Market – Regional Share Distribution (2025)

Europe at 22.4% in 2025 is defined by the dual forces of luxury vehicle premiumization and sustainability regulation. The EU's End-of-Life Vehicle (ELV) regulation revision, requiring 25% recycled material content in new vehicles by 2030, is reshaping upholstery material specifications across German, French, Italian, and Swedish OEM supply chains. BMW's Munich R&D campus and Volkswagen's Wolfsburg facilities are driving material innovation investments of hundreds of millions of euros annually in sustainable interior materials programs.

North America at 17.3% is anchored by the US market's structural preferences for premium truck and SUV interiors – the Ford F-Series, Chevrolet Silverado, and Ram 1500 pickup trucks alone represent approximately 2.5 million annual unit sales, with leather and premium synthetic upholstery standard across multiple trim levels. The North American aftermarket upholstery market is particularly dynamic, with Katzkin Leather reporting 20%+ annual revenue growth driven by consumer desire for post-sale leather interior upgrades.

Competitive Landscape

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Adient PLC |

Adient Seating Systems |

Leader |

Global seat manufacturing scale, OEM relationships, R&D in smart seating |

|

Lear Corporation |

Lear E-Systems / ComfortMax |

Leader |

Thermal comfort technologies, GM partnership, EV seat integration |

|

Toyota Boshoku Corp. |

Toyota Boshoku Interior |

Leader |

Toyota ecosystem integration, Japan quality heritage, sustainable materials |

|

Faurecia (Forvia SE) |

Faurecia (FORVIA) / HELLA integration |

Leader |

Complete cockpit systems, sustainability leadership, full-vehicle interior scope |

|

Grupo Antolin Irausa |

Grupo Antolin Interior |

Challenger |

Headliner leadership, global OEM coverage, lighting-integrated interiors |

|

Borgers SE & Co. KGaA |

Borgers Automotive |

Challenger |

Non-woven specialist, acoustic management, European OEM focus |

|

Sage Automotive Interiors |

Sage / Ultrafabrics |

Challenger |

Premium synthetic leather, sustainable materials, North America strength |

|

Katzkin Leather Inc. |

Katzkin Custom Leather |

Emerging |

Aftermarket leather leadership, North America OEM partnerships |

|

Seiren Co., Ltd |

Viscotecs / Seiren Auto |

Emerging |

Smart heating fabric technology, Japan premium OEM supplier |

|

The Haartz Corporation |

Haartz Convertible Tops |

Emerging |

Convertible top fabric specialist, premium performance fabrics |

The automotive upholstery competitive landscape is characterized by a small number of global Tier-1 automotive seating and interior system suppliers commanding dominant OEM relationships, alongside specialized material innovators carving high-value niches in smart textiles, premium synthetic leather, and sustainable material segments. Adient and Lear Corporation collectively hold estimated combined revenue exceeding USD 40 Billion annually across their full automotive seating businesses, though upholstery materials represent a subset of broader seating system revenue.

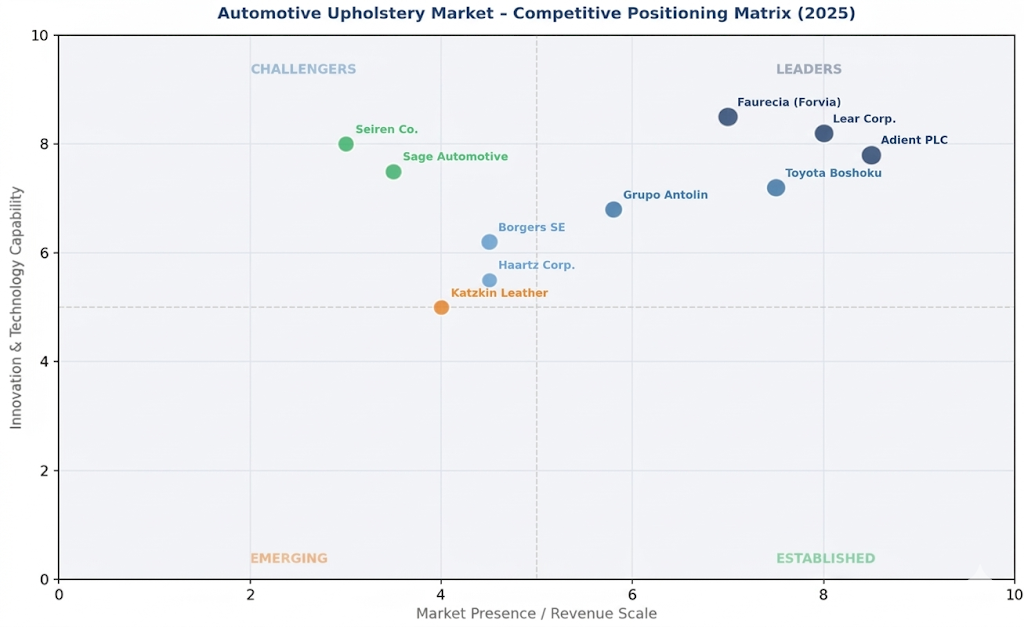

Figure 10: Automotive Upholstery Market – Competitive Positioning Matrix (2025)

Key Company Profiles

Adient PLC

Adient PLC, headquartered in Dublin, Ireland, is the world's largest automotive seating supplier, with operations in 30+ countries and approximately 75,000 employees globally. The company serves virtually all major global OEMs, including Toyota, General Motors, Volkswagen, Ford, and BMW, as a primary Tier-1 seating systems partner.

- Product Portfolio: Complete automotive seating systems, seat covers and upholstery components, seat structures and mechanisms, and foam and trim components.

- Recent Developments: In 2024, Adient partnered with BASF to develop next-generation sustainable seat foam using bio-based polyols. In Q1 2025, the company announced expanded smart seating R&D capabilities for integrated biometric monitoring.

- Strategic Focus: Adient's strategy centers on transitioning from hardware-centric seating supply to software-enabled seating systems incorporating health monitoring, comfort optimization, and connectivity, targeting premium OEM platforms through 2030.

Lear Corporation

Lear Corporation, headquartered in Southfield, Michigan, USA, is a global Tier-1 automotive supplier specializing in seating and E-Systems with annual revenues exceeding USD 23 Billion (2023). Lear's seating division is among the world's largest, with deep partnerships across North American, European, and Asian OEM ecosystems.

- Product Portfolio: ComfortMax seat systems, thermal comfort upholstery, intelligent seating platforms, and E-Systems connectivity solutions integrated into seating.

- Recent Developments: In 2024, Lear announced a strategic engineering partnership with General Motors for ComfortMax Seats with thermal comfort technologies for select GM EV models. The company targets EBITDA margin expansion through premium upholstery content growth in North American and European programs.

- Strategic Focus: Lear is investing in smart seating integration – combining upholstery materials with embedded electronics for occupant sensing, thermal management, and connectivity – targeting USD 1 Billion+ in incremental smart seating revenue by 2028.

Toyota Boshoku Corporation

Toyota Boshoku Corporation, headquartered in Aichi, Japan, is a member of the Toyota Group and a leading global manufacturer of automotive interior systems, including seat assemblies, door trims, headliners, and floor systems. The company operates in 27 countries with manufacturing in all major automotive production regions.

- Product Portfolio: Seat assemblies and upholstery, interior trims, filtration systems, and floor systems incorporating carpeting and upholstery materials.

- Recent Developments: Toyota Boshoku unveiled its "2030 Vision" interior materials strategy in 2024, committing to 30% bio-based and recycled material content across its product portfolio by 2030, aligned with Toyota Group's carbon neutrality targets.

- Strategic Focus: The company is expanding sustainable material programs while deepening integration with Toyota's BEV platform development, where Toyota Boshoku serves as the primary interior systems Tier-1 partner for the Toyota/Lexus EV lineup.

Faurecia (Forvia SE)

Faurecia, operating under the Forvia SE umbrella since its merger with HELLA in 2022, is one of the world's largest automotive technology suppliers. Headquartered in Nanterre, France, with revenues exceeding EUR 22 Billion in 2023, Forvia's Faurecia division covers seating, interiors, and clean mobility solutions across 33 countries.

- Product Portfolio: Complete seating systems, interior modules, acoustic and soft trim solutions, and zero-emission mobility technologies.

- Recent Developments: Faurecia unveiled the "SeatForHealth" concept in 2024, integrating health monitoring sensors into seat upholstery to measure vital signs in real time. The company is advancing its MATERI'ACT sustainable materials platform targeting 50% sustainable content in products by 2025.

- Strategic Focus: Forvia's strategy prioritizes the integration of health and wellness technology into upholstery systems, carbon-neutral manufacturing, and expansion of its sustainable materials portfolio to meet EU regulatory requirements and OEM ESG commitments.

Grupo Antolin Irausa S.A.

Grupo Antolin, headquartered in Burgos, Spain, is a global leader in automotive interior components with particular strength in headliner systems, door trims, overhead systems, and lighting-integrated interior modules. The company operates in 26 countries with annual revenues exceeding EUR 3 Billion.

- Product Portfolio: Headliner systems, door panels, overhead consoles, lighting systems, and instrument panel components with integrated upholstery surfaces.

- Recent Developments: Grupo Antolin deployed its Ambient Light integrated headliner system in multiple European OEM programs in 2024, combining fabric upholstery with embedded LED ambient lighting controlled via vehicle infotainment systems.

- Strategic Focus: The company is focused on smart interior integration – embedding lighting, sensing, and connectivity directly into upholstery and trim components – targeting premium European OEM programs where interior technology differentiation drives purchase decisions.

Market Concentration Analysis

The global automotive upholstery market exhibits moderate concentration among a small number of global Tier-1 automotive seating and interior suppliers, with Adient, Lear Corporation, Toyota Boshoku, and Faurecia (Forvia) collectively accounting for approximately 40-50% of global market revenue in 2025 when measured across their full seating and interior systems scope inclusive of upholstery content.

The market demonstrates a classic bifurcated competitive structure. At the OEM-integrated Tier-1 level, consolidation trends are pronounced – developing advanced smart seating and sustainable material capabilities requires R&D investment of USD 200-500 Million annually per major player, creating high barriers that limit competitive entry and support incumbent advantage. The top 5 Tier-1 suppliers hold estimated upholstery-relevant revenue market shares ranging from 8-15% individually.

Simultaneously, the materials and specialized component sub-markets are highly fragmented. More than 200 regional fabric mills, leather tanneries, and polymer component manufacturers supply inputs to Tier-1 assemblers and OEM aftermarket channels. The Haartz Corporation in convertible tops, Katzkin Leather in aftermarket leather, and Seiren Co. in smart heating fabrics each hold dominant positions within focused niches without posing broad competitive threats to Tier-1 system integrators.

Consolidation activity is increasing – Forvia's merger integration, strategic partnerships such as Adient's BASF collaboration, and private equity investment in specialty fabric companies reflect a market in gradual structural consolidation. Chinese domestic upholstery suppliers are a notable competitive dynamic, with companies such as BAIC's interior subsidiary and Huafeng Group gaining domestic OEM share in China's strategically critical market.

Investment & Growth Opportunities

Fastest-Growing Segments

Smart Fabrics represent the highest-growth investment opportunity at ~8.7% CAGR through 2034. Seiren Co.'s Viscotecs electric heating fabric and Sage Automotive Interiors' sensor-embedded seat covers are pioneering commercial deployments that are establishing scalable manufacturing precedents. Investment in smart textile production infrastructure, electronic fiber integration technologies, and OEM qualification partnerships represents the most capital-efficient path to premium market positioning in the next 5-7 years.

Synthetic Leather at ~6.2% CAGR is the second-fastest growing segment, particularly in bio-based and sustainably certified variants. The global vegan leather market is projected to exceed USD 89 Billion by 2030 across all applications, with automotive representing a high-value captive demand base as luxury OEMs commit to animal-free interior programs.

Emerging Market Expansion

According to an industry report, Indian automotive market, including passenger and commercial vehicles, will grow from 5.1 million units in 2023 to 7.5 million units by 2030, with the passenger vehicle segment reaching 6.0 million units. This will further solidify India's position as the third-largest passenger vehicle market in the world. supported by rising middle-class income levels and government PLI scheme incentives supporting automotive manufacturing expansion. The Indian premium vehicle segment is growing at approximately 12-15% annually, creating accelerating demand for premium upholstery specifications.

In 2023, the ASEAN vehicle market ranked as the fifth-largest sub-regional market globally, with total sales reaching approximately 3.3 million units. The passenger cars market in ASEAN is estimated to generate revenues of around USD 68.3 billion by 2025.. The region's growing EV adoption driven by Chinese OEM market entry is elevating interior specification standards across vehicle segments.

Venture & Private Investment Trends

Notable investment activity includes Bolt Threads' USD 57.5 Million funding for Mylo mycelium leather scaling, Desserto's multiple investment rounds for cactus-based leather production expansion, and Pangaia's bio-material licensing partnerships with automotive OEMs. Strategic private equity consolidation in the specialty automotive fabric and synthetic leather segment is evidenced by multiple mid-market M&A transactions in 2023-2025.

Future Market Outlook (2026-2034)

The global automotive upholstery market forecast projects steady value expansion from USD 7.8 Billion in 2025 to USD 11.4 Billion by 2034 at a CAGR of 4.15%, a 46% absolute value increase underpinned by vehicle production growth, premium specification upgrades, sustainable material adoption mandates, and smart fabric technology integration across the forecast period.

Three structural forces are most likely to reshape the automotive upholstery market through 2034. First, the EV interior premiumization cycle – as EV platforms gain market share to an estimated 40-50% of new vehicle sales by 2030-2032 globally, each unit represents a USD 200-400 upholstery specification upgrade opportunity versus ICE equivalents, generating meaningful aggregate market value uplift beyond raw volume growth.

Second, regulatory-driven sustainability mandates will restructure material mix away from conventional polymers and leather toward recycled, bio-based, and circular economy materials through 2034. The EU's ELV regulation 25% recycled content requirement by 2030 alone affects approximately 10-12 million new vehicles annually in Europe, creating a regulatory pull market for sustainable upholstery materials with limited conventional alternative substitutability.

Third, smart fabric technology will transition from a luxury-exclusive feature set to mainstream premium specification by 2030-2032. Heated and ventilated seat fabrics, today standard in 65% of European vehicles, will be complemented by sensor-embedded biometric monitoring and adaptive comfort fabrics as OEM differentiation tools in the mass-market premium tier – the highest-volume revenue segment for upholstery value add. By 2034, the automotive upholstery industry is forecast to have completed its foundational transformation from commodity interior materials supply to technology-enabled premium interior experience delivery.

Research Methodology

Primary Research

Primary research encompassed structured interviews with automotive interior supply chain stakeholders, including product directors at Tier-1 upholstery suppliers, automotive OEM purchasing and interior programme managers, automotive textile and leather processing industry executives, specialty fabric and smart material developers, and institutional investors in automotive materials technology companies. Primary insights validated market sizing, material segment shares, technology adoption timelines, and competitive positioning assessments presented in this report.

Secondary Research

Secondary sources include OICA global vehicle production data (2024), IEA Global EV Outlook, EU End-of-Life Vehicle regulation publications, REACH compliance documentation from ECHA, company annual reports and investor presentations (Adient, Lear, Faurecia/Forvia, Toyota Boshoku), trade publications including Automotive News, INDA nonwovens industry reports, International Leather Journal, Polymer Degradation and Stability journal, and regional automotive industry association data from SIAM (India), CAAM (China), ACEA (Europe), and Alliance for Automotive Innovation (US).

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating global and regional vehicle production forecasts, per-vehicle upholstery material content value analysis by vehicle segment, material mix evolution modeling aligned with regulatory timelines, and end-user demand curve analysis. Scenario analysis (base, optimistic, and conservative cases) was conducted to account for macroeconomic uncertainty, commodity price volatility, and EV adoption rate variability through the 2026-2034 forecast horizon.

Automotive Upholstery Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Upholstery Materials Covered | Automotive Textiles, Leather, Plastics, Smart Fabrics, Synthetic Leather, Thermoplastic Polymers |

| Fabric Types Covered | Non-woven, Woven |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles |

| Sales Channels Covered | OEM, Aftermarket |

| Applications Covered | Carpets, Dashboards, Roof Liners, Seat Covers, Sun Visors, Trunk Liners |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Adient PLC, Lear Corporation, Toyota Boshoku Corp., Faurecia (Forvia SE), Grupo Antolin Irausa, Borgers SE & Co. KGaA, Sage Automotive Interiors, Katzkin Leather Inc., Seiren Co., Ltd, The Haartz Corporation |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive upholstery market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global automotive upholstery market outlook.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive upholstery industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global automotive upholstery market was valued at USD 7.8 Billion in 2025, driven by rising vehicle production, premium interior demand, and lightweight material adoption across global OEM platforms.

The market is projected to reach USD 11.4 Billion by 2034, growing at a CAGR of 4.15% during 2026-2034, supported by EV premiumization, smart fabric adoption, and sustainable material mandates.

Plastics lead with a 42.2% share in 2025, followed by leather at 22.7%. Smart Fabrics, though smallest at 3.8%, represent the fastest-growing material segment at ~8.7% CAGR through 2034.

Non-Woven fabric type dominates at 64.5% in 2025, preferred by OEMs for its lightweight, cost-efficient, and recyclable properties. Woven fabric at 35.5% serves premium seat applications.

Asia Pacific leads with a 49.8% share in 2025, driven by China's 34 million vehicle production output, India's expanding automotive sector, and rising consumer demand for premium interiors.

Key drivers include rising global vehicle production exceeding 92 million units in 2024 (OICA), EV interior premiumization, growing luxury vehicle sales, and demand for sustainable and smart upholstery materials.

Leading companies include Adient PLC, Lear Corporation, Toyota Boshoku Corporation, Faurecia (Forvia SE), Grupo Antolin, Borgers SE, Sage Automotive Interiors, Katzkin Leather, Seiren Co., Ltd, and The Haartz Corporation.

EV platforms drive premium interior specifications and lightweight material demand. EV upholstery content value is approximately 15–25% higher per vehicle versus ICE equivalents, representing structural market uplift.

Smart fabrics integrate conductive fibers enabling seat heating, ventilation, biometric sensing, and electroluminescent design. Seiren's Viscotecs heating fabric and sensor-integrated seat covers are production examples.

The EU ELV regulation requiring 25% recycled content by 2030, bio-based leather alternatives (cactus leather, mycelium), and OEM commitments to animal-free interiors are reshaping the material landscape.

Smart Fabrics at ~8.7% CAGR through 2034 is the fastest-growing segment, driven by sensor integration demand for health monitoring, heated/ventilated seats, and next-generation EV interior architectures.

IMARC Group offers up to 10% free customization including additional country data, company profiles, custom segmentation, and strategic scenario analysis. Contact our research team within 12-week support window.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)