Automotive Instrument Cluster Market Size, Share, Trends and Forecast by Cluster Type, Vehicle Type, Sales Channel, Application, and Region, 2025-2033

Automotive Instrument Cluster Market Size and Share:

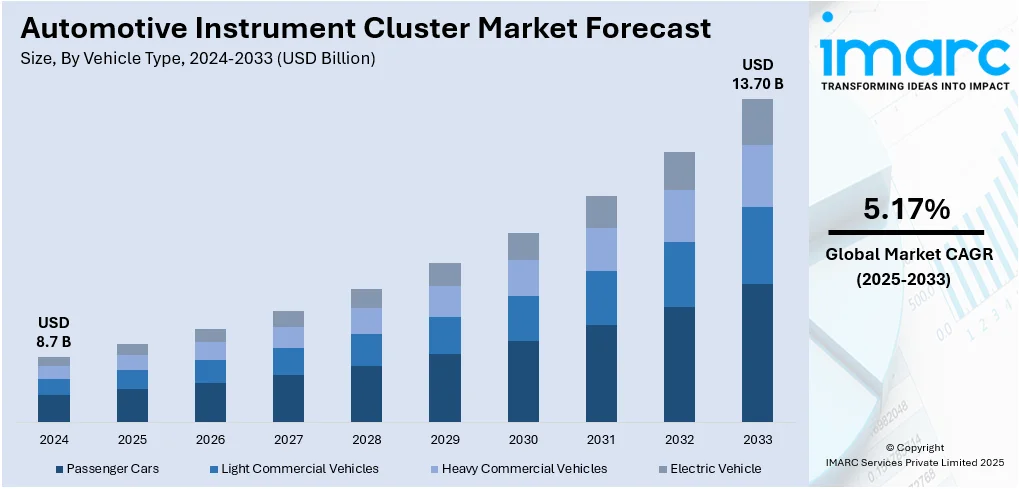

The global automotive instrument cluster market size was valued at USD 8.7 Billion in 2024. The market is projected to reach USD 13.70 Billion by 2033, exhibiting a CAGR of 5.17% from 2025-2033. Asia Pacific currently dominates the market, holding a market share of over 47.8% in 2024. The market is driven by mounting demand for digital and hybrid displays, growth in adoption of electric and hybrid vehicles, and embedding advanced driver-assistance systems (ADAS) and infotainment capabilities. Users are looking for more intuitive, connected, and customizable driving experiences, which encourages automakers to evolve display technologies. Furthermore, changing vehicle safety legislations and the move toward energy efficiency are driving cluster design innovation at a faster pace. These aspects are largely driving the growing automotive instrument cluster market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 8.7 Billion |

|

Market Forecast in 2033

|

USD 13.70 Billion |

| Market Growth Rate 2025-2033 | 5.17% |

The global automotive instrument cluster market is being driven by the enhanced integration of sophisticated infotainment and navigation systems into the vehicle displays. As there is a change in consumer tastes towards more engaging and connected driving experiences, manufacturers are adding digital clusters to vehicles that integrate multimedia, navigation, and vehicle status data into one integrated, easy-to-use interface. These systems provide unbroken access to GPS navigation, traffic reports, music streaming, and hands-free calls, greatly improving driving convenience. For example, in January 2025 – BMW revealed its Panoramic iDrive with a 3D heads-up display covering the entire windshield to replace the standard gauge cluster in its forthcoming Neue Klasse-derived X-class SUV. Furthermore, the growth in vehicle-to-everything (V2X) communications further aids this trend, as instrument clusters are now required to show alerts and data from nearby infrastructure. Furthermore, technological innovation in artificial intelligence and voice recognition is evolving clusters into dynamic interaction centers that react to driver input in real time. This intersection of technologies is developing a new breed of instrument clusters intended to offer an integrated and customized experience, which makes them crucial elements in entry-level as well as premium cars sold around the world.

To get more information on this market, Request Sample

In 2024, the United States represented around 85.80% share of automotive instrument cluster market outlook on the back of healthy consumer demand for digital displays that address sustainability and energy efficiency objectives. With growing adoption of electric and hybrid cars in the U.S., there is a need for improved cluster interfaces that provide real-time information like battery levels, regenerative braking effectiveness, and range estimates. This is changing how instrument clusters are developed, with digital panels becoming more prevalent to take in energy-related information and visualizations. These clusters are also being tailored to enable intuitive user interfaces that streamlines energy monitoring and minimizes driver distraction. For instance, in August 2024 – Ford rolled out its Android-based Digital Experience in the 2025 Explorer, with a 13.2″ screen and a 12.3″ digital gauge cluster with built-in map projection, its initial Ford-labeled deployment. Moreover, while government policies encourage vehicle electrification and efficiency gains, manufacturers are integrating energy analytics directly into the driver's main line of sight. This trend towards functional, high-resolution instrument clusters in electric and hybrid cars is leading the charge to driving continued demand for instrument clusters throughout the American automotive ecosystem.

Automotive Instrument Cluster Market Trends:

Technological Advancements in Vehicle Electronics

Technological advancements in vehicle electronics are significantly influencing the automotive instrument cluster market trends. Modern vehicles are increasingly equipped with electronic systems that offer enhanced functionality and user experience. Additionally, they encompass the integration of high-resolution displays, touch-screen interfaces, and customizable options, allowing drivers to personalize their dashboard display according to their preferences. For instance, META and BMW aim to incorporate IMU data from a BMW car’s sensor array in real-time into the tracking system of the Project Aria research glasses. Apart from this, instrument clusters are increasingly being integrated with vehicle connectivity systems, allowing them to access and display information from external sources, such as smartphone apps, cloud services, and vehicle-to-infrastructure communication systems.

Rising Demand for Electric and Hybrid Vehicles

As per the automotive instrument cluster market analysis, rapid shift towards electric and hybrid vehicles, owing to the growing need for reducing carbon footprints, is proliferating the market demand. Moreover, government bodies are launching favorable policies to encourage investments in the automotive industry. For instance, in February 2022, the Indian government announced that the subsidy under the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) program was US$ 351 Million in 2023. This amount was nearly nine times the allocation for FY21. The demand for electric and hybrid vehicles is further expected to bolster the market growth. The International Energy Agency (IEA) reports that the number of available electric-car models grew 15 % year-on-year to nearly 785 in 2024, intensifying demand for EV-specific displays, battery state-of-charge, range estimations, and energy-flow animations. For instance, Toyota Australia added several improvements to its well-liked Corolla hatchback and sedan ranges in November 2022, including the hybrid powertrain and Toyota Connected Services capabilities.

Integration of infotainment and Navigation Systems

The integration of infotainment and navigation systems in the automotive instrument cluster systems is a key trend that is shaping the development of modern vehicle displays. The global automotive infotainment sector reached USD 21.1 Billion in 2024 and is projected by IMARC Group to hit USD 41.2 Billion by 2033, a 6.93 % CAGR (2025-2033). The integration allows for a more consolidated and streamlined display. Modern instrument clusters are no longer limited to displaying basic vehicle information, they also encompass multifunctional displays that integrate entertainment, information, and navigation features. This integration enhances the driving experience by providing easy access to essential functions, such as global positioning system (GPS) navigation, traffic updates, multimedia playback, and smartphone connectivity. For instance, in February 2024, Peugeot announced its integration of ChatGPT artificial intelligence into its vehicles, making it one of the first car manufacturers to do so.

Government Regulations on Vehicle Safety and Fuel Efficiency

Government regulations regarding vehicle safety and fuel efficiency are stimulating innovations in the automotive instrument cluster market. For instance, regulations mandating the display of tire pressure monitoring, fuel efficiency, and emission levels have necessitated the development of more informative and sophisticated instrument clusters. Furthermore, these regulations aim to promote safer driving practices and reduce environmental impact through better fuel efficiency. Apart from this, to promote the production and purchase of electric vehicles and two-wheelers, the government has implemented several incentives and subsidies. To hasten the transition to electric vehicles, the rules were reinforced in 2023.

Automotive Instrument Cluster Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global automotive instrument cluster market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on cluster type, vehicle type, sales channel, and application.

Analysis by Cluster Type:

- Analog

- Digital

- Hybrid

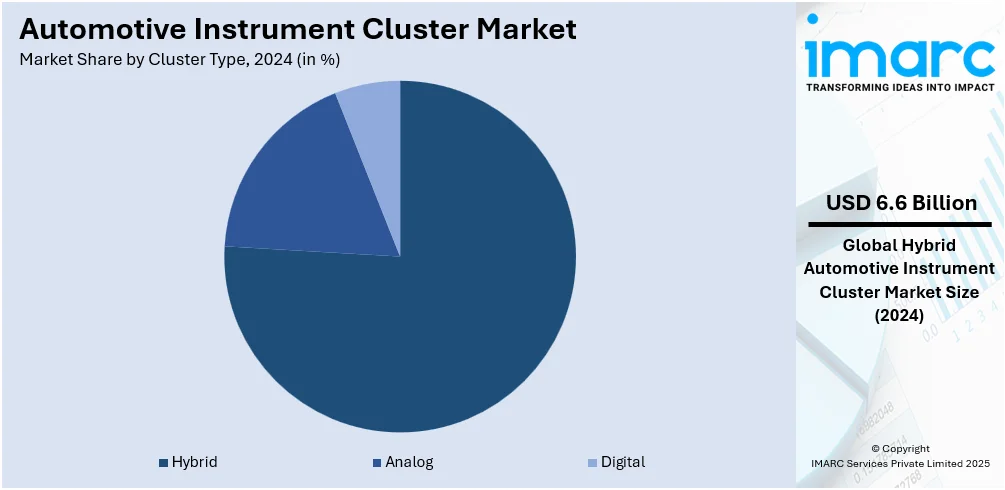

Hybrid instrument clusters accounted for around 75.7% market share of the global automotive instrument cluster market in 2024 and were thus the leading type among vehicle categories. They are so prevalent because they can combine analog dials with digital screens in perfect harmony, providing familiarity along with additional capabilities at a lower price than a completely digital option. Hybrid clusters are attractive to companies seeking cost savings without losing usability. They offer critical driving details like speed and fuel level combined with real-time information like navigation and safety alerts to suit the wider consumer base across entry-level and high-end segments. Their flexibility across internal combustion engine (ICE), hybrid, and electric cars again accelerates demand. As cars become increasingly connected, hybrid clusters remain an effective solution to enable step-by-step digitalization. Their modularity, simple integration, and cost benefit guarantee ongoing market favor, especially in innovation versus affordability-balancing markets.

Analysis by Vehicle Type:

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Electric Vehicle

Growing vehicle sales and consumer demand for digital instrument clusters are driving growth in the passenger car segment. Growing demand for infotainment systems, navigation, and real-time vehicular information improves the adoption of high-end clusters. Automakers are adding fully digital or hybrid instrument clusters to improve the overall user experience, enhance vehicle design, and enable connected driving features.

Instrument clusters in light commercial vehicles are crucial for providing operating information, fuel efficiency data, and route tracing functionality. As e-commerce and last-mile delivery activities grow, LCVs now come with digital or semi-digital clusters for better fleet management. Telematics integration is a prominent feature of the segment, enabling maintenance reminders and driver behavior observation for commercial use.

Heavy commercial trucks need rugged and informative instrument clusters to provide safe and efficient operations on long hauls. These clusters frequently incorporate advanced diagnostics, load monitoring, and telematics displays. Increased use of fleet management systems and regulatory pressures for improved safety are prompting OEMs to utilize high-resolution, rugged digital clusters optimized for severe driving conditions and logistics efficiency.

Electric cars require extremely interactive and digital cluster instruments to share battery health, charge levels, energy use, and range. With accelerating EV uptake worldwide, manufacturers favor cutting-edge displays with personalized interfaces and real-time analytics. The cluster segment is experiencing high-speed innovation in design, with smooth integration of infotainment and intelligent mobility solutions boosting performance and user interaction.

Analysis by Sales Channel:

- OEM

- Aftermarket

The OEM segment commands a leading share in the automotive instrument cluster market on the back of close partnerships with automakers and the inclusion of sophisticated digital displays in newer car models. Growing demand for smart dashboards, coupled with OEMs' interest in upgrading driver experience and safety, keeps this segment growing. OEMs are also facilitated by scalability and early technology take-up.

The aftermarket market is picking up steam as car owners want to replace old-style clusters with new digital or hybrid clusters. The demand is strong in older cars and commercial fleets that need better function, GPS capability, or a facelift. DIY culture and specialty shops further bolster the market segment with affordable solutions for clusters compared to factory settings.

Analysis by Application:

- Speedometer

- Odometer

- Tachometer

- Others

The speedometer is still a central feature of contemporary instrument clusters but no longer as an independent market segment since it has become part of larger digital and hybrid display systems. Modern instrument clusters have speed information as part of multifunctional formats, displaying navigation, media, ADAS warning, and vehicle diagnostics as well. Such integration simplifies the driver's interface, minimizing distraction while increasing visual simplicity and effectiveness. The shift from traditional analog speedometers to digital representations within TFT and OLED panels reflects changing automotive design priorities, emphasizing sleek aesthetics and data accessibility. Customizable digital dashboards allow drivers to configure layouts where speed, fuel, range, and performance metrics are prioritized according to personal preference. As connected and partially autonomous driving technologies improve, the speedometer function is more and more supplemented by contextual elements such as adaptive cruise speed, detection of speed limits, and dynamic warnings. This integrated functionality guarantees that speed monitoring becomes a must, although no longer separately defined in market analyses.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

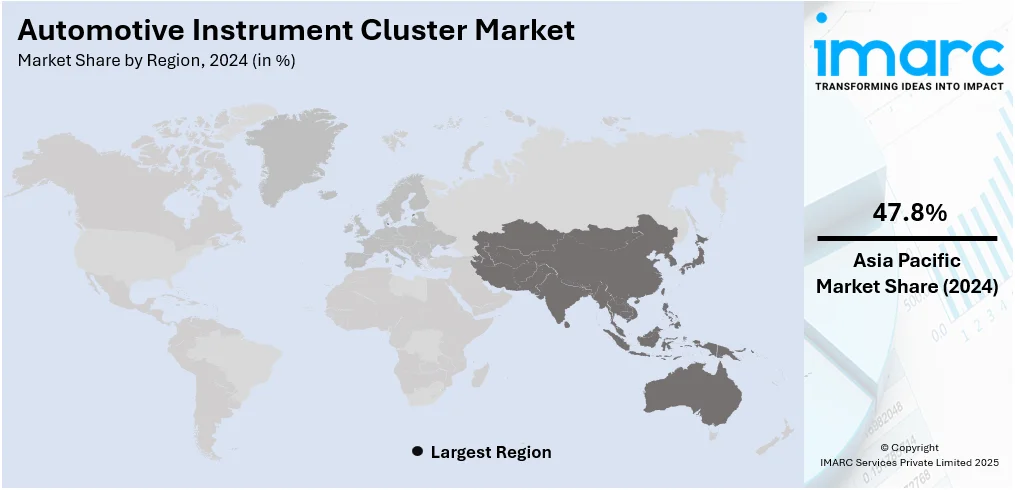

During 2024, the Asia Pacific region had around 47.8% share in the overall automotive instrument cluster market, which ranks the region as the top regional player. This leadership is due to the availability of key vehicle manufacturers, huge production capacity, and increasing demand for economy as well as premium cars with innovative interiors. Regions like China, Japan, South Korea, and India are quickly embedding digital technologies into cars, promoting the requirement for intelligent and multifunctional instrument clusters. Electrification and hybridization of vehicles are also progressing rapidly throughout the region, promoting digital interfaces for range monitoring, visualization of energy flow, and system diagnostics. Moreover, positive government policies for automotive innovation and clean mobility are responsible for higher production and deployment of superior clusters. Strong component manufacturing and export base in Asia Pacific also ensures OEMs' ability to cater to both domestic and overseas markets. These synergistic factors create the region's position as an engine for global instrument cluster industry growth.

Key Regional Takeaways:

North America Automotive Instrument Cluster Market Analysis

In North America, the automotive instrument cluster market is witnessing significant growth fueled by increasing consumer demand for digital and connected in-vehicle interfaces. The region enjoys a technologically advanced automotive ecosystem wherein manufacturers are highly incorporating high-resolution displays, customizing user interfaces, and advanced driver-assistance system (ADAS) visualizations into cluster designs. The shift towards electric and hybrid cars is especially impactful, as these platforms need dynamic clusters that are able to show battery level, energy flow, and range information in real-time. Regulatory focus on vehicle safety and information availability has also spurred the creation of clusters that combine navigation, alerts, and multimedia duties into a single combined module. North American customers are also increasingly expressing a keen desire for digital cockpit experiences, and manufacturers are responding by installing digital or hybrid clusters even in middle-range vehicles. The presence of the large OEMs and continued R&D spending in automotive electronics cements the position of the region as a leading innovation center in this market.

United States Automotive Instrument Cluster Market Analysis

The market for automotive instrument clusters in the United States is experiencing consistent growth as a result of increased demand from consumers for digitally enhanced and user-friendly car interfaces. Greater integration of voice recognition and head-up display capabilities contributes to enhanced user experience, driving market growth. Movement toward connected and semi-autonomous vehicles further speeded up deployment of reconfigurable digital clusters. Based on one survey of autonomous cars, 13% of American drivers would have faith in riding in autonomous cars, up from 9% last year, reflecting growing comfort with automation and justifying demand for dynamic cluster systems. Heightened concern over EVs is also pushing manufacturers to implement novel cluster designs to show battery state, range, and power consumption in real time. OEMs are investing in high-performance processors and modular architecture to provide smoother animations and real-time updates. In addition, boosting demand for multi-screen dashboard settings is helping clusters integrate with infotainment systems. Higher safety standards and increasing driver distraction awareness are propelling the creation of minimalist yet informative interfaces. Additionally, regulatory focus on fuel efficiency and emission monitoring is driving the uptake of smart instrument clusters with support for eco-driving feedback mechanisms and real-time diagnostic capabilities.

Europe Automotive Instrument Cluster Market Analysis

Europe's automotive instrument cluster market is growing, underpinned by increased demand for intuitive driver information systems in line with the region's safety and sustainability focus. Customers are demanding more real-time navigation indications and integration of advanced driver-assistance systems (ADAS) on the cluster interface. Europe ADAS Market will grow to USD 35.5 billion in 2025 at a CAGR of 8.60% and reach USD 53.63 billion by 2030. OEMs are utilizing fully digital clusters for better ergonomics and providing smooth transitions between driving modes and real-time vehicle analysis. The growth of shared mobility and fleet services in urban locations is also promoting the use of instrument clusters for multiple drivers, emphasizing flexibility and data personalization. High cluster connectivity to mobile apps and home devices is becoming a distinct driving factor in the region, reaffirming the function of clusters as a command center interface.

Asia Pacific Automotive Instrument Cluster Market Analysis

Asia Pacific's automotive instrument cluster market is expanding at a great pace, with increased demand for small and mid-size cars featuring sophisticated display capabilities. Urbanization and an expanding population that is highly technologically driven, together with a boost in automobile manufacturing and increasing disposable incomes are driving the uptake of digital clusters among new models of cars. By 2050, the population of Asia's cities is projected to amplify by 50%, with an extra 1.2 billion people. Manufacturers are preoccupied with incorporating gesture control and haptic feedback in clusters to support driver engagement while not sacrificing safety. Demand for smart mobility solutions and two-wheeler integration with digital meters is opening up innovative opportunities. Growing dependence on data-led user interfaces for traffic and routing optimization is helping drive the growth of AI-enabled cluster systems. Cloud-based upgrades and remote diagnostic capability are also increasing value.

Latin America Automotive Instrument Cluster Market Analysis

Latin America market growth of the instrument cluster is driven primarily by the increasing demand for affordable vehicles with basic digital upgrades. Region countries are witnessing rising usage of semi-digital clusters in mid-level cars due to urbanization and emerging middle-class buyers. As stated, as early as 2050, 90% of Latin Americans will be urban dwellers. There are over 55 cities with populations exceeding one million. While totally digital clusters are confined to the premium segments, OEMs are now starting to bring about cost-effective technology upgrades to address regional tastes as well as enhance competitiveness.

Middle East and Africa Automotive Instrument Cluster Market Analysis

The Middle East and Africa automotive instrument cluster market is advancing with the help of growing consumer knowledge of in-vehicle digital technologies. Growing automobile upgrades in metropolitan regions are driving demand for visually striking cluster systems with real-time vehicle health meters. The major growth driver is regional demand for luxury automobiles with upscale interiors, where digital clusters help to provide a high-end user experience. Middle East luxury car market size was USD 20699.6 Million in 2024 and is anticipated to expand at a CAGR of 4.68% from 2025-2033. In addition, transforming transportation ecosystems such as smart city projects are encouraging the use of advanced cluster technologies.

Competitive Landscape:

The automotive instrument cluster market competitive scenario is changing at a very fast pace in accordance with changing consumer needs and advancements in technology, and the market is expected to grow at a very high rate during the forecast period. As digitalization gains momentum across vehicle segments, industry leaders are concentrating on creating sophisticated clusters that combine high-resolution displays, ADAS interfaces, navigation, and infotainment features in one unit. The automotive instrument cluster market forecast indicates robust growth fueled by demand for improved driver experience, connectivity, and smart vehicle interfaces. This calls for investing in flexible platforms that enable internal combustion, hybrid, and electric vehicle customization. Automaker and tech firm partnerships are growing stronger, with the goal of integrating AI, voice control, and cloud-based services into future-generation clusters. Regional dynamics also influence competition—Asia Pacific dominates manufacturing, North America and Europe take the lead in innovation and safety compliance—defining a forward-looking and globally competitive market landscape.

The report provides a comprehensive analysis of the competitive landscape in the automotive instrument cluster market with detailed profiles of all major companies, including:

- Alps Alpine Co Ltd.

- Continental AG

- JPM Group

- Nippon Seiki Co. Ltd.

- Pricol Limited

- Robert Bosch GmbH (Robert Bosch Stiftung GmbH)

- Simco Auto Limited

- Valid Manufacturing Ltd.

- Visteon Corporation

Latest News and Developments:

- May 2025: Suzuki launched the 2025 Access Ride Connect TFT Edition in India, featuring a 4.2-inch TFT instrument cluster the first in its mass-market two-wheelers. Priced at ₹1.02 lakh, the upgraded cluster offered enhanced visuals, Bluetooth connectivity, and modern design. A new Pearl Mat Aqua Silver color variant also debuted.

- April 2025: Bajaj introduced the 2025 Dominar 400 at dealerships across India, featuring its first major update in years. A key upgrade included a fully digital Bluetooth-enabled instrument cluster, adapted from the Pulsar NS400Z. This enhanced connectivity and user interface signaled Bajaj’s push towards modern cockpit designs in premium motorcycles.

- April 2025: Maruti Suzuki launched the 2025 Grand Vitara in India with a 7-inch digital instrument cluster offered exclusively in the strong-hybrid variant. This upgrade, alongside a 9-inch infotainment system and other tech features, reflected the brand’s continued focus on enhancing cockpit digitalization in mid-size SUVs to improve user experience.

- February 2025: Waze rolled out version 5.4 on Android and iOS, enabling navigation data display on vehicle instrument clusters via CarPlay and Android Auto. Compatible with select vehicles like BMW, Ford, and Polestar, the update enhanced driver convenience by shifting map visibility closer to eye level, boosting instrument cluster utility.

- January 2025: Honda launched the 2025 Livo with a fully digital instrument cluster displaying real-time mileage, distance to empty, gear position, and service reminders. This upgrade aligned with the rising demand for smart displays in two-wheelers. The update marked Honda’s push to enhance rider information accessibility while meeting new emission norms.

Automotive Instrument Cluster Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Cluster Types Covered | Analog, Digital, Hybrid |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicle |

| Sales Channels Covered | OEM, Aftermarket |

| Applications Covered | Speedometer, Odometer, Tachometer, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Alps Alpine Co Ltd, Continental AG, JPM Group, Nippon Seiki Co. Ltd., Pricol Limited, Robert Bosch GmbH (Robert Bosch Stiftung GmbH), Simco Auto Limited, Valid Manufacturing Ltd, Visteon Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive instrument cluster market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global automotive instrument cluster market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive instrument cluster industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The automotive instrument cluster market was valued at USD 8.7 Billion in 2024.

The automotive instrument cluster market is projected to exhibit a CAGR of 5.17% during 2025-2033, reaching a value of USD 13.70 Billion by 2033.

The automotive instrument cluster market is driven by the growing demand for digital and hybrid displays, growing adoption of hybrid and electric vehicles, and the adoption of ADAS and infotainment systems. Preference for customized driving experiences among consumers, coupled with regulatory focus on vehicle safety and access to real-time data, is further driving market growth in every class of vehicle.

Asia Pacific currently dominates the automotive instrument cluster market, accounting for a share of 47.8%. This is driven by robust vehicle production capability, growing consumer interest in high-tech features, and aggressive EV take-up in the region. Government initiatives backing smart mobility and domestic manufacturing also add to the extensive adoption of digital cluster systems among markets such as China, India, and Japan.

Some of the major players in the automotive instrument cluster market include Alps Alpine Co Ltd, Continental AG, JPM Group, Nippon Seiki Co. Ltd., Pricol Limited, Robert Bosch GmbH (Robert Bosch Stiftung GmbH), Simco Auto Limited, Valid Manufacturing Ltd, Visteon Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)