Automotive Glass Market Report by Glass Type (Laminated Glass, Tempered Glass, and Others), Material Type (IR PVB, Metal Coated Glass, Tinted Glass, and Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Trucks, Buses, and Others), Application (Windshield, Sidelite, Backlite, Rear Quarter Glass, Sideview Mirror, Rearview Mirror, and Others), End-User (OEMs, Aftermarket Suppliers), Technology (Active Smart Glass, Passive Glass), and Region 2026-2034

Automotive Glass Market Size:

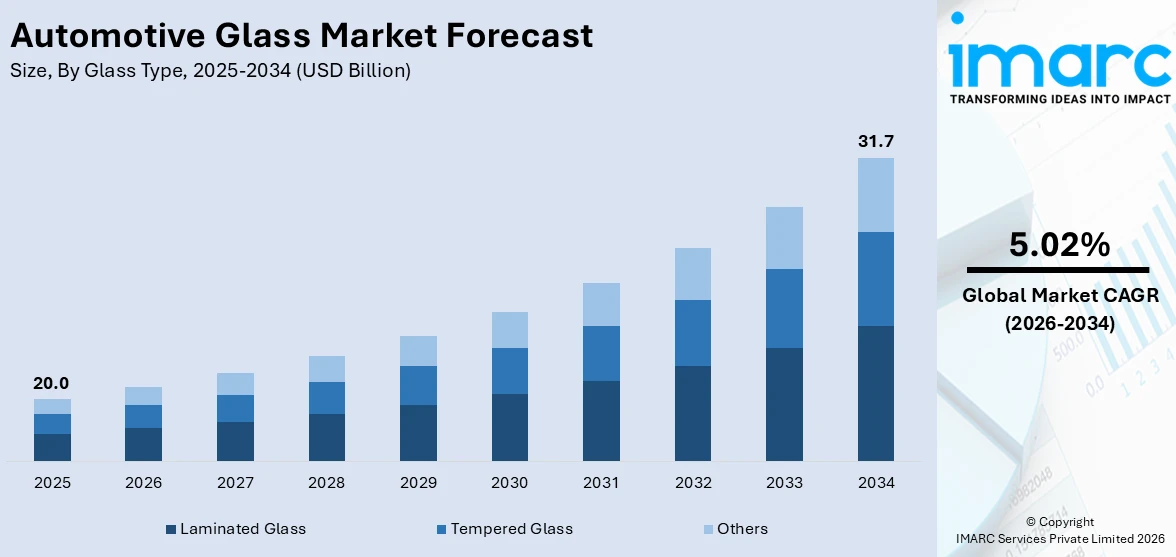

The global automotive glass market size reached USD 20.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 31.7 Billion by 2034, exhibiting a growth rate (CAGR) of 5.02% during 2026-2034. Increased vehicle production, cutting-edge glass technology advancements, stringent safety norms, the rising demand in electric and autonomous vehicles, lightweight material preferences, and sustainability initiatives in glass manufacturing are key drivers providing a considerable thrust to the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 20.0 Billion |

|

Market Forecast in 2034

|

USD 31.7 Billion |

| Market Growth Rate 2026-2034 | 5.02% |

Automotive Glass Market Analysis:

- Major Market Drivers: The pioneering consumer interests in luxury and comfort are some of the key catalysts prevalent in the automotive glass market report. Moreover, the introduction of advanced functional features, such as acoustic dampening and thermal regulation, within automobile glass and the expected rise of self-driving public transport systems, which may require enhanced quantities of high-visibility glass, are supporting the market growth. Additionally, key manufacturers are creating a lighter glass composite due to increased pressure on weight reduction in vehicles, which is accelerating the market growth. Furthermore, the integration of solar rows in sunroofs as it significantly improves energy efficiency, the increasing need for aftermarket customization and repairs, the push of digitalization into all features of automotive design, and surging use of augmented reality (AI) on windshields are all pivotal factors driving the automotive glass market price and demand, shaping the scope of the automotive glass industry in the future.

- Key Market Trends: The automotive glass market analysis shows that the consumers’ demand for larger windshield and window designs that improve visibility and look more aesthetically pleasing is supporting the market growth. This fact is also reflected in the current market share trends, such as the increasing use of gorilla glass – a superior material characterized by its strength and limited resistance. Moreover, relatively recent technology of adjustable tints for rear windshields and side glasses, offering the possibility of special privacy and ability to control sunlight availability, is another growth-inducing factor. In line with this, key manufacturers are now integrating various safety features, such as lane-keeping assist and front collision warning systems directly on the glass, which is further propelling the automotive glass market share dynamics.

- Geographical Trends: The Asia-Pacific region currently dominates the automotive glass market due to the largest volume of new global car sales, rapidly growing urban populations, and high automobile ownership rates. The region is further reinforced by the presence of major automotive and glass producers and an end-user market – the largest share of new cars are sold in the region, especially China and India. Furthermore, the extensive manufacturing capacities in the region, driven by the abundant labor force and government-backed policies, also benefit the market. Europe and North America also play a substantial role, boasting advanced technological development, high safety standards, and well-developed automotive production.

- Competitive Landscape: The competition within the automotive glass market is fierce, with major players expanding their market share through innovative solutions, strategic partnerships, and mergers and acquisitions. To stay ahead in the global automotive glass market, companies are heavily investing in research and development (R&D) and expanding their product portfolios to develop more durable and lightweight solutions with enhanced features and technology to comply with consumer demands and regulatory requirements. With a strategic focus on quality leadership, technology innovation, and sustainable development options, the suppliers can capitalize on various business automotive glass market business opportunities.

- Challenges and Opportunities: The highly competitive market dynamics guarantee a relentless drive towards technological progression, quality enhancement, and cost efficiency across the automotive glass market analysis. However, fluctuating raw material prices and high costs associated with technological advancements in the glass sector can influence overall market prices. Safety and regulatory standards set rigorous constraints to be followed and adhered to, and the automotive glass market offers vast opportunities to become more innovative in the future. The electric car trend will continue to grow, giving opportunities for companies to develop more energy-efficient and sustainable offerings in line with automotive glass market trends.

To get more information on this market Request Sample

Automotive Glass Market Trends:

Increasing Vehicle Production

The increasing volume of global vehicle production is one of the key drivers of the automotive glass market. According to ACEA, the worldwide production of motor vehicles in 2022 totaled an estimated 85.4 million vehicles, which was 5.7% higher than the 2021 level. Simultaneously, the expansion of the automotive industry requires more automotive glass to equip new vehicles with windshields, windows, and sunroofs. High consumer purchasing power, accelerated urbanization, and an increasing number of automotive production facilities worldwide contribute to market growth. As cars are produced in ever greater quantities, especially in developing countries, automotive glass has become a crucial matter for the manufacturers seeking to adequately and sustainably respond to the global vehicle demand.

Advancements in glass technology

Technological breakthroughs in automotive glass drive market development by providing smart glass that changes transparency depending on the external environment or user preference. These solutions provide vehicles with aesthetic appeal, energy-saving capability, and passenger comfort, including ultraviolet (UV) protection, insulation, and glare reduction. As a result, the consumer seeks to purchase more technologically advanced cars, creating the demand for high-tech glass solutions and forcing manufacturers to develop new glass innovations. This trend satisfies demand while responding to the automotive industry’s more advanced transition towards high-tech, high-value components.

Stringent Safety Regulations

Safety regulations are a key driver in the automotive glass market because it makes it mandatory to install safety glass for protecting passengers in case of an accident. Strict rules and regulations were imposed to use laminated or tempered glass by governments worldwide based on their ability to avoid severe injuries. For instance, in the United States, rigid safety norms like FMVSS No. 205 made it compulsory to use laminated or tempered glass in motor vehicles to reduce consumer risk. Such safety norms mandate the windshields to be laminated in critical areas such that the glass cannot shatter, and side and rear windows must be tempered so that in the event of breakage, the beams will not injure the passenger. This has compelled manufacturers to maintain high safety and quality standards and develop durable and impact-resistant automotive glass. Furthermore, it shows that manufacturers’ commitment to consumer safety in addition to profitability influences their brand image and competitiveness.

Automotive Glass Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on glass type, material type, vehicle type, application, end-user and technology.

Breakup by Glass Type:

- Laminated Glass

- Tempered Glass

- Others

Laminated glass accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the glass type. This includes laminated glass, tempered glass, and others. According to the report, laminated glass represented the largest segment.

The laminated glass segment is driven by the increasing demand for safety and security features in both automotive and architectural applications. This type of glass is renowned for its ability to hold together when shattered, offering protection against break-ins, accidents, and natural disasters. The heightened emphasis on passenger safety in vehicles, coupled with stringent regulations mandating the use of laminated glass in certain areas of a vehicle, significantly propels its demand. In the architectural sector, its popularity is bolstered by its sound insulation properties, UV protection, and energy efficiency, making it a preferred choice for modern building designs. Moreover, the shift towards green buildings and the need for energy conservation are catalyzing the adoption of laminated glass, as it plays a crucial role in enhancing thermal performance and reducing carbon footprints. The segment's growth is also fueled by innovations in glass technology, such as the incorporation of smart features and aesthetic enhancements, which align with contemporary trends in architecture and vehicle design.

Breakup by Material Type:

- IR PVB

- Metal Coated Glass

- Tinted Glass

- Others

IR PVB represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the material type. This includes IR PVB, metal coated glass, tinted glass, and others. According to the report, IR PVB represented the largest segment.

The infrared-blocking polyvinyl butyral (IR PVB) segment is driven by the increasing demand for energy-efficient automotive solutions. As global emphasis on reducing vehicle emissions and enhancing fuel efficiency intensifies, automotive manufacturers are incorporating IR PVB laminates in car windows and windshields. This material effectively blocks infrared rays, thereby significantly reducing the heat build-up inside vehicles. This reduction in interior temperature diminishes the reliance on air conditioning, leading to lower fuel consumption and reduced emissions. Moreover, the growing consumer awareness regarding UV protection and the comfort provided by IR-blocking glass are pivotal in escalating the demand for IR PVB products. The segment also benefits from stringent regulatory standards mandating the incorporation of energy-efficient materials in automotive manufacturing, which ensures continued growth and innovation in this area.

Breakup by Vehicle Type:

- Passenger Cars

- Light Commercial Vehicles

- Trucks

- Buses

- Others

Passenger cars accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the vehicle type. This includes passenger cars, light commercial vehicles, trucks, buses, and others. According to the report, passenger cars represented the largest segment.

The passenger cars segment is driven by the increasing consumer demand for safety, comfort, and aesthetic appeal in their vehicles. As per the MarkLines, 2,979,113 units of passenger cars were sold in 2022. Enhanced safety features such as laminated and tempered glass, which provide added protection in case of accidents, are paramount. Comfort is enhanced through innovations like noise-reducing acoustic glass and climate control technologies that maintain internal temperature regardless of external weather conditions. Aesthetically, there is a growing preference for larger, more panoramic windshields and windows, offering not only improved visibility but also a sense of openness and luxury. Additionally, the integration of advanced technologies such as heads-up displays (HUDs) and connectivity features for seamless integration with smartphones and other devices is becoming increasingly common, reflecting the segment's alignment with contemporary technological trends. The push towards electric vehicles (EVs) also significantly impacts this segment, with automotive glass playing a crucial role in enhancing energy efficiency, reducing vehicle weight, and supporting the integration of solar panels to power vehicle electronics.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Windshield

- Sidelite

- Backlite

- Rear Quarter Glass

- Sideview Mirror

- Rearview Mirror

- Others

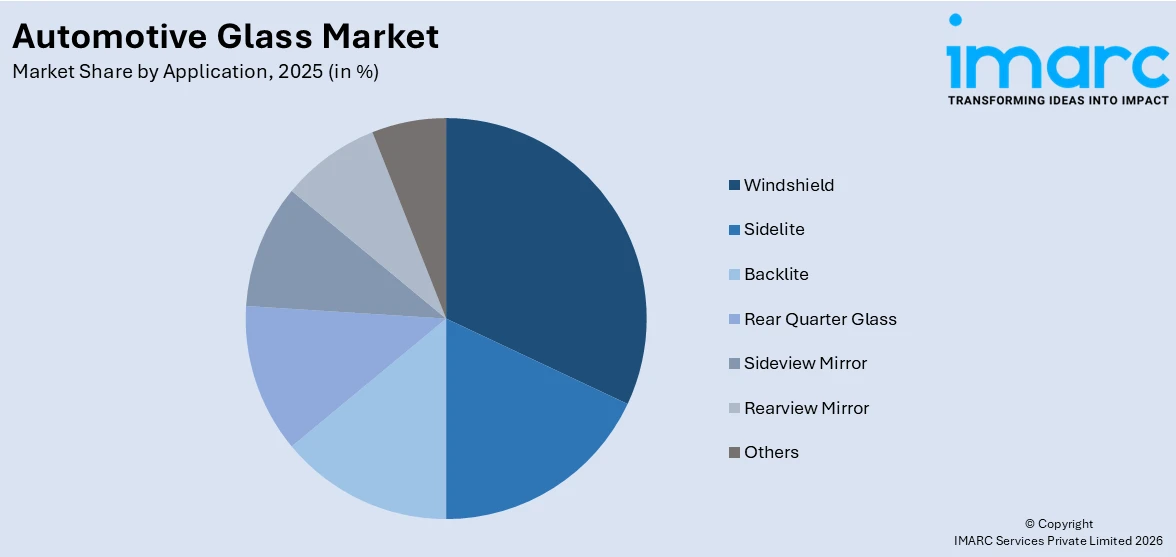

Windshield represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the application. This includes windshield, sidelite, backlite, rear quarter glass, sideview mirror, rearview mirror, and others. According to the report, windshield represented the largest segment.

The windshield segment is driven by the increasing emphasis on safety and visibility in automotive design. Enhanced safety standards worldwide necessitate high-quality windshields that can withstand impacts and provide clear visibility under various conditions. Innovations in windshield technology, such as laminated glass and heads-up displays, offer additional functionality, such as projecting information directly onto the glass, thereby increasing driver awareness and safety. The integration of advanced driver-assistance systems (ADAS) and the push for autonomous vehicles further elevate the importance of high-quality windshields, as they must accommodate various sensors and cameras. As per Stellantis, Stellantis Ventures announced it has invested in SteerLight, the developer of a new generation of high-performance light detection and ranging (LiDAR) sensing technology. Moreover, consumer demand for aesthetically pleasing vehicles with large, panoramic windshields contributes to this segment's growth, merging functionality with design elegance. The trend towards EVs also impacts this segment, as manufacturers seek to optimize aerodynamics and reduce vehicle weight, influencing windshield design and materials.

Breakup by End-User:

- OEMs

- Aftermarket Suppliers

OEMs accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the end user. This includes OEMs and aftermarket suppliers. According to the report, OEMs represented the largest segment.

The OEM segment is driven by the increasing demand for high-quality, durable automotive glass, ensuring adherence to stringent safety and quality standards set by original equipment manufacturers and regulatory bodies. This segment benefits significantly from the automotive industry's robust growth, as OEMs require reliable suppliers that can meet the precise specifications for new vehicle models. Innovations in glass technology, such as improved strength, enhanced clarity, and integrated advanced features like heads-up displays and connectivity for autonomous driving, are pivotal. The trend towards electric vehicles and the incorporation of solar panels in automotive glass also substantially impacts this segment, as OEMs seek to enhance energy efficiency and support the vehicle's electrical systems. As per the Wards Intelligence, in 2022, hybrid, plug-in hybrid, and BEV sales were 12.9% of total sales. Moreover, the rising consumer expectation for luxury features, like noise-reducing acoustic glass and UV protection, further stimulates the demand within the OEM segment, ensuring that vehicles meet the highest standards of comfort, safety, and innovation.

Breakup by Technology:

- Active Smart Glass

- Suspended Particle Glass

- Electrochromic Glass

- Liquid Crystal Glass

- Passive Glass

- Thermochromic

- Photochromic

Passive glass represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the technology. This includes active smart glass (suspended particle glass, electrochromic glass, and liquid crystal glass) and passive glass (thermochromic and photochromic). According to the report, passive glass represented the largest segment.

The passive glass segment is driven by the increasing demand for cost-effective and durable glass options in the automotive sector. This segment, focused on traditional automotive glass without active functionalities, emphasizes high strength, resilience, and safety features. Manufacturers are investing in research to enhance the toughness and shatter-resistance of passive glass, making it more appealing for consumers prioritizing safety and longevity. The segment benefits from the steady demand in both OEM and aftermarket sectors, where the need for replacement glass keeps the market buoyant. Additionally, the rising emphasis on vehicle weight reduction without compromising safety is pushing advancements in lightweight passive glass compositions, aligning with the industry’s shift towards more fuel-efficient vehicles. Environmental regulations and recycling initiatives are also pivotal, as there is a growing trend towards using sustainable and eco-friendly materials, which passive glass can accommodate due to its simpler manufacturing processes and ease of recycling compared to coated or specially treated glass.

Breakup by Region:

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- North America

- United States

- Canada

- Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Peru

- Others

- Middle East and Africa

- Turkey

- Saudi Arabia

- Iran

- United Arab Emirates

- Others

Asia Pacific leads the market, accounting for the largest automotive glass market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa (Turkey, Saudi Arabia, Iran, United Arab Emirates, Others). According to the report, Asia Pacific represents the largest regional market for automotive glass.

The Asia-Pacific’s automotive glass market is fueled by expanding demand for automobiles caused by growing population and developing economics, especially in China and India, where automobile industries are thriving. According to The World Counts, Asia’s population is projected to grow from 4.64 billion people in 2020 to 5.267 billion people in 2050. Rapid urbanization and developing living standards stimulate ownership per capita, affecting automobile glass sectors. Likewise, automotive technology innovation and advancement, along with the demand for luxury and cutting-edge automobile safety, are important components. Moreover, numerous automobile glass manufacturers in the region maintain pricing and availability competition. Economical governmental support and investments in road development boost automobile manufacturing and demand for automobile glass. Furthermore, the expanding electric vehicle market will also contribute to that market increasing, as these types of vehicles often have certain types of glass for greater efficiency and integration with cutting-edge technologies.

Competitive Landscape:

In the automotive glass market, key players are intensively focusing on a range of strategic initiatives to solidify their market positions and respond to the evolving industry demands. They are heavily investing in R&D to introduce innovative glass solutions that offer enhanced safety, durability, and added functionalities like UV protection, thermal insulation, and advanced connectivity for integrated display systems. Collaborations and partnerships with automobile manufacturers are prevalent, aiming to tailor their products to the specific needs of new vehicle models, including electric and autonomous vehicles. As per Dayton Daily News, Fuyao Glass America announced to build a 600,000-square-foot facility immediately north of its current operations at 800 Fuyao Ave. for USD 46 million. The overall combined project investment when accounting for machinery, site improvements, infrastructure, and equipment is approximately USD 300 million. Additionally, these companies are expanding their global footprints through strategic mergers, acquisitions, and joint ventures, enabling them to access new markets and leverage local expertise. Emphasis is also placed on sustainability, with efforts to reduce carbon footprints and incorporate recycling in the production process, aligning with the growing consumer and regulatory demand for environmentally friendly products.

The report provides a comprehensive analysis of the competitive landscape in the global automotive glass market with detailed profiles of all major companies, including:

- AGC Inc.

- Central Glass Co., Ltd.

- Corning Incorporated

- Fuyao Glass Industry Group Co., Ltd.

- Gentex Corporation

- Guardian Industries Holdings (Koch Industries)

- Magna International Inc.

- Nippon Sheet Glass Co., Ltd.

- Saint-Gobain Sekurit

- Schott AG

- Sisecam

- Vitro Inc.

- Webasto Group

- Xinyi Glass Holdings Limited

Automotive Glass Market News:

- In June 2022: Corning announced a collaboration with Hyundai Mobis to develop lightweight automotive glass solutions aimed at enhancing vehicle fuel efficiency and safety. The partnership aims to leverage Corning's expertise in advanced glass technologies to produce durable and lightweight automotive glass that meets stringent industry standards.

- In August 2022: Saint-Gobain inaugurated a new automotive glass production facility in China, reinforcing its presence in the Asia-Pacific region. The state-of-the-art facility is equipped with advanced manufacturing technologies to produce high-quality automotive glass products tailored to meet the specific needs of the Chinese market.

Automotive Glass Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Glass Types Covered | Laminated Glass, Tempered Glass, Others |

| Material Types Covered | IR PVB, Metal Coated Glass, Tinted Glass, Others |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Trucks, Buses, Others |

| Applications Covered | Windshield, Sidelite, Backlite, Rear Quarter Glass, Sideview Mirror, Rearview Mirror, Others |

| End-Users Covered | OEMs, Aftermarket Suppliers |

| Technologies Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | AGC Inc., Central Glass Co., Ltd., Corning Incorporated, Fuyao Glass Industry Group Co., Ltd., Gentex Corporation, Guardian Industries Holdings (Koch Industries), Magna International Inc., Nippon Sheet Glass Co., Ltd., Saint-Gobain Sekurit, Schott AG, Sisecam, Vitro Inc., Webasto Group, Xinyi Glass Holdings Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive glass market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global automotive glass market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive glass industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global automotive glass market was valued at USD 20.0 Billion in 2025.

We expect the global automotive glass market to exhibit a CAGR of 5.02% during 2026-2034.

The emergence of smart automotive glass in luxury and premium cars, along with the rising product integration with in-vehicle entertainment systems, is currently driving the global automotive glass market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations resulting in temporary closure of numerous manufacturing units in automotive sector, thereby hampering the demand for automotive glass.

Based on the glass type, the global automotive glass market has been segmented into laminated glass, tempered glass, and others. Currently, laminated glass holds the majority of the total market share.

Based on the material type, the global automotive glass market can be divided into IR PVB, metal coated glass, tinted glass, and others. Among these, IR PVB exhibits a clear dominance in the market.

Based on the vehicle type, the global automotive glass market has been categorized into passenger cars, light commercial vehicles, trucks, buses, and others. Currently, passenger cars account for the majority of the global market share.

Based on the application, the global automotive glass market can be segregated into windshield, sidelite, backlite, rear quarter glass, sideview mirror, rearview mirror, and others. Among these, windshield currently holds the largest market share.

Based on the end-user, the global automotive glass market has been bifurcated into OEMs and aftermarket suppliers, where OEMs exhibit a clear dominance in the market.

Based on the technology, the global automotive glass market can be categorized into active smart glass and passive glass. Currently, passive glass accounts for the majority of the total market share.

On a regional level, the market has been classified into Europe, Asia Pacific, North America, Latin America, and Middle East and Africa, where Asia Pacific currently dominates the global market.

Some of the major players in the global automotive glass market include AGC Inc., Central Glass Co., Ltd., Corning Incorporated, Fuyao Glass Industry Group Co., Ltd., Gentex Corporation, Guardian Industries Holdings (Koch Industries), Magna International Inc., Nippon Sheet Glass Co., Ltd., Saint-Gobain Sekurit, Schott AG, Sisecam, Vitro Inc., Webasto Group, Xinyi Glass Holdings Limited, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)