Autoimmune Disease Diagnosis Market Size, Share, Trends and Forecast by Product Type, Disease Type, Test Type, End-User, and Region, 2025-2033

Autoimmune Disease Diagnosis Market Size and Share:

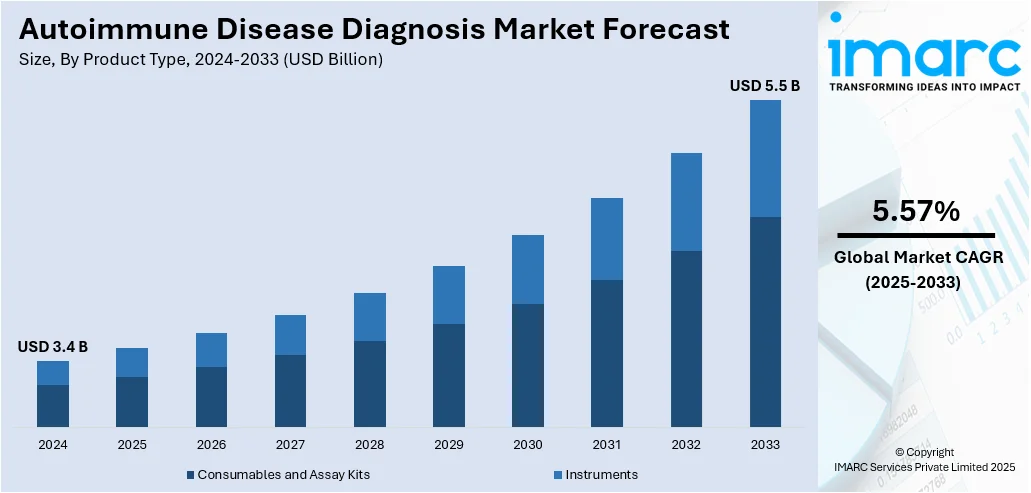

The global autoimmune disease diagnosis market size was valued at USD 3.4 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 5.5 Billion by 2033, exhibiting a CAGR of 5.57% during 2025-2033. North America dominated the market, holding a significant market share of over 39.7% in 2024. Rising focus on improving patient outcomes, advancements in diagnostic technologies, collaborations and partnerships among major players, and the need for accurate diagnostic solutions represent some of the factors contributing to the autoimmune disease diagnosis market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 3.4 Billion |

|

Market Forecast in 2033

|

USD 5.5 Billion |

| Market Growth Rate (2025-2033) | 5.57% |

The market is growing due to several key drivers. The rising global incidence of autoimmune disorders like rheumatoid arthritis, lupus, and multiple sclerosis has increased the need for accurate diagnosis. Awareness among patients and healthcare providers has improved, prompting earlier testing and treatment. Technological advancements, especially in biomarker discovery and imaging, allow faster and more precise detection. Aging populations are more prone to autoimmune conditions, which further fuels demand. There's also increased investment in research and development, leading to better diagnostic tools. Expansion of healthcare infrastructure in emerging markets has improved access to testing services. In addition, the growing use of point-of-care testing and automation in labs helps reduce turnaround time, making diagnosis more efficient. These combined factors are pushing the market forward and encouraging innovation across diagnostic platforms.

To get more information on this market, Request Sample

In the United States, efforts to improve early detection of autoimmune disorders like lupus and rheumatoid arthritis are gaining pace through new multi-biomarker assays. These tools aim to raise diagnostic sensitivity by targeting markers such as TC4d, TIgG, and TIgM, signaling a shift toward more precise, blood-based testing methods in clinical immunology. For instance, in January 2025, Exagen Inc. received conditional approval from the New York State Department of Health for its new biomarker assays to enhance the detection of lupus and rheumatoid arthritis. The assays, set to be added to the AVISE CTD platform, were designed to improve diagnostic sensitivity using biomarkers like TC4d, TIgG, and TIgM.

Autoimmune Disease Diagnosis Market Trends:

Advancements in Diagnostic Technologies

New biomarkers like autoantibodies are discovered to diagnose specific autoimmune diseases like lupus, rheumatoid arthritis, and celiac disease. For instance, epidemiological studies have shown that the incidence (rate of new cases) of global autoimmune diseases has risen yearly by 19.1% with rheumatological diseases such as Sjögren’s and lupus rising 7.1% per year. Biomarkers can provide more precise classification and early identification of autoimmune diseases. More individualized diagnostics are allowing for the discovery of distinct protein signatures or metabolic profiles linked to autoimmune disorders only because of developments in proteomics and metabolomics. Furthermore, microarray technology allows simultaneous testing of multiple biomarkers, which makes it easier to diagnose complex autoimmune diseases involving multiple genetic or protein factors. Additionally, companies are launching cutting-edge products and new technologies, which is positively influencing the autoimmune disease diagnosis market outlook. For instance, on 25 March 2024, AbbVie Inc. and Landos Biopharma, Inc. announced a definitive agreement under which AbbVie will acquire Landos, a clinical stage biopharmaceutical company focused on the development of novel and oral therapeutics for patients with autoimmune diseases. The main investigational asset of Landos is NX-13, a first-in-class, oral NLRX1 agonist with a bimodal mechanism of action (MOA).

Rising Focus on Improving Patient Outcomes

The US Food and Drug Administration (FDA) provided clearance for Werfen's Aptiva connective tissue disease (CTD) essential reagent under 510(k) on October 16, 2023. New reagents benefit in speeding up diagnosis and enhancing patient outcomes in difficult-to-diagnose autoimmune disorders. As per the autoimmune disease diagnosis market forecast, rising efforts to enhance early and precise detection for improved patient care are likely to boost demand. Apart from this, early diagnosis of autoimmune disorders enables medical professionals to start treatment quickly while preventing or delaying the onset of diseases, including multiple sclerosis, lupus, and rheumatoid arthritis.

Collaborations and Partnerships among Key Players

On January 10, 2023, ScipherMedicine acquired CrossBridge, a Philadelphia-based data, analytics, and software company, to enhance its data and analytics capabilities. This enables a more granular and real time understanding of patients' treatment pathways. The software as a service (SaaS) value-based care platform aids in lowering healthcare costs while enhancing patient outcomes. Through various collaborations, companies combine their expertise in immunology, molecular biology, and bioinformatics, which supports the autoimmune disease diagnosis market growth. A large number of pharmaceutical companies are collaborating with diagnostic companies to provide companion diagnostics tests that are intended to determine which patients will benefit the most from particular treatments. For instance, in total 2,399,600 of the 15 key diagnostic tests were performed during April 2025. This is an increase of 70,600 (3.0%) from April 2024, which is 8.2% when adjusted for working days. These diagnostics aid in matching patients with the best biologic therapy for autoimmune illnesses, enhancing results while decreasing treatment selection trial and error. These partnerships also involve the co-development of treatments and diagnostic tools. For instance, pharmaceutical companies might work with diagnostics firms to create tests that monitor treatment efficacy, helping doctors adjust therapies in real time to improve patient outcomes.

Autoimmune Disease Diagnosis Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global autoimmune disease diagnosis market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on product type, disease type, test type, and end-user.

Analysis by Product Type:

- Consumables and Assay Kits

- Instruments

Consumables and assay kits stood as the largest product type in 2024, holding around 72.8% of the market. Diagnostic laboratories and hospitals require a continuous supply of consumables and assay kits for routine testing and monitoring of autoimmune diseases. Since autoimmune conditions often require long-term monitoring, the demand for consumables remains high. They are used in a variety of diagnostic procedures, including immunohistochemistry, flow cytometry, Western blot, and enzyme-linked immunosorbent assay (ELISA). They play a vital role in identifying autoantibodies connected to celiac disease, multiple sclerosis, lupus, and rheumatoid arthritis. Assay kits and consumables have a shorter lifespan as compared to diagnostic devices.

Analysis by Disease Type:

- Systemic Autoimmune Disease

- Rheumatoid Arthritis

- Psoriasis

- Systemic Lupus Erythematosus (SLE)

- Multiple Sclerosis

- Others

- Localized Autoimmune Disease

- Inflammatory Bowel Disease

- Type 1 Diabetes

- Thyroid

- Others

Localized autoimmune disease led the market with around 51.7% of market share in 2024. Localized autoimmune diseases are far more common as compared to systemic autoimmune illnesses. Localized autoimmune disease diagnostic procedures are more precise and targeted. Additionally, companies are developing products that aid in the treatment of various illnesses. For example, on June 9, 2023, AstraZeneca and Quell Therapeutics entered in a license agreement to develop multiple engineered T-regulator (Treg) cell therapies with the potential to be curative for both type 1 diabetes (T1D) and inflammatory bowel disease (IBD) indications. Autologous multi-modular Treg cell therapy candidates for key autoimmune disease indications will be developed using Quell's patented toolbox of Treg cell engineering modules. This is expected to provide a positive autoimmune disease diagnosis market forecast.

Analysis by Test Type:

- Routine Laboratory Tests

- Inflammatory Markers

- Autoantibodies and Immunologic Tests

- Others

Autoantibodies and immunologic tests led the market with around 35.3% of market share in 2024. The growing use of autoantibodies and immunologic tests is pushing demand in the autoimmune disease diagnosis market. These tests help detect early-stage autoimmune disorders by identifying specific autoantibodies linked to diseases like rheumatoid arthritis, lupus, and type 1 diabetes. Their accuracy makes them a preferred first-line diagnostic tool among clinicians. With more awareness, patients are seeking earlier evaluation, especially when symptoms are vague. Labs and diagnostics companies are expanding panels to include newer biomarkers, which are now being validated at a faster rate due to advances in immunology. Also, insurance coverage for these tests has improved, reducing out-of-pocket costs and encouraging broader adoption. As autoimmune conditions become more widely recognized and better understood, the use of immunologic assays continues to increase, helping drive both clinical demand and revenue in this segment.

Analysis by End-User:

- Clinical Laboratories

- Hospitals

- Others

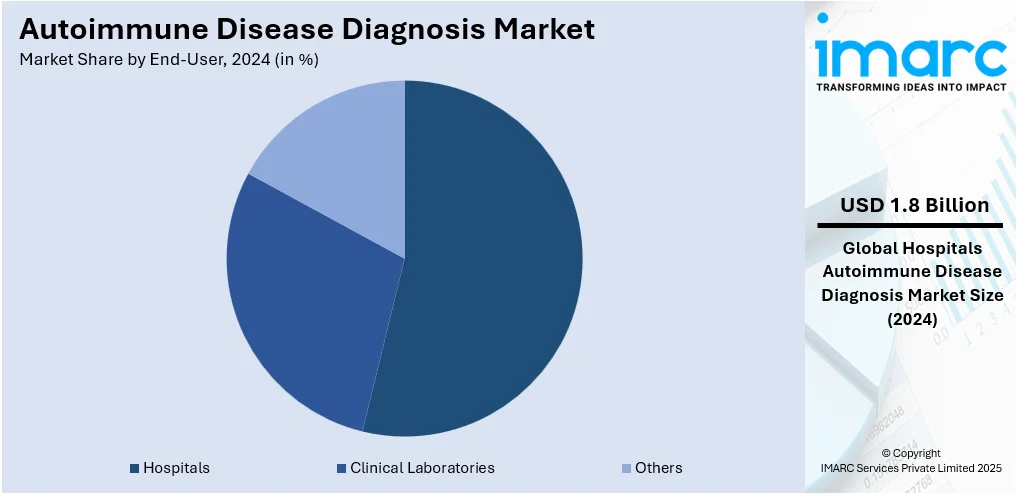

Hospitals led the market with around 53.6% of market share in 2024. In the autoimmune disease diagnosis market, hospitals are a major demand driver due to their role as primary diagnostic and treatment centers. They handle a large share of autoimmune cases, especially moderate to severe ones that require specialized testing. Hospitals typically invest in advanced diagnostic tools, such as autoantibody panels, ANA testing, and flow cytometry, because of the need for accuracy in complex cases. These facilities often house multidisciplinary teams, including immunologists, rheumatologists, and lab technicians, who rely on high-throughput and integrated diagnostic systems. The increasing number of autoimmune disorders being diagnosed in hospital settings, combined with a rise in hospital-based outpatient services, also adds to the volume. Further, hospitals tend to adopt newer diagnostic technologies earlier than small labs or clinics, which helps boost market growth through faster adoption and higher procurement volumes.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 39.7%. North America, particularly the United States, has a high prevalence of autoimmune diseases among individuals. The region benefits from a highly developed healthcare system with widespread access to advanced diagnostic technologies. Clinical laboratories, hospitals, and specialized diagnostic centers have the latest molecular diagnostics and imaging techniques, enabling efficient and accurate diagnosis of autoimmune diseases. Besides this, autoimmune disease diagnosis companies in the region are focusing on introducing solutions that provide enhanced care to individuals suffering from autoimmune diseases. For example, on October 03, 2023, WellTheory, a first-of-its-kind virtual solution for the 50 Million Americans suffering from autoimmune disease, launched an enterprise solution that will enable employers and payers to offer autoimmune care through WellTheory. Through its new enterprise solution, WellTheory will be able to tackle the unseen costs and productivity impacts of untreated autoimmune diseases across the entire healthcare ecosystem.

Key Regional Takeaways:

United States Autoimmune Disease Diagnosis Market Analysis

In 2024, the United States accounted for 91.50% of the market share in North America. United States is witnessing increased autoimmune disease diagnosis adoption due to the sharp rise of autoimmune diseases across various age groups. Over 50 Million Americans (8% of the U.S. population) are affected by autoimmune diseases and current data suggests that the prevalence of autoimmune diseases is rising. The growing prevalence of conditions such as multiple sclerosis and rheumatoid arthritis has prompted healthcare providers to invest in advanced testing tools. The rise of autoimmune diseases has created pressure on public health systems, leading to enhanced diagnostic programs and early intervention strategies. Hospitals and clinics are emphasizing personalized diagnostics, which is accelerating the adoption of specialized screening tools. Growing awareness, availability of advanced diagnostic technologies, and integration of electronic health records further support early detection. In addition, insurance coverage for autoimmune disease-related tests has improved access to diagnosis. Rising clinical research initiatives are also contributing to the adoption of advanced autoimmune disease diagnosis tools nationwide.

Asia Pacific Autoimmune Disease Diagnosis Market Analysis

Asia-Pacific is experiencing growing autoimmune disease diagnosis adoption primarily due to the increasing number of Type 1 Diabetes patients. For instance, the estimated number of individuals with diabetes in India was 32 Million in the year 2000, which rose to 63 Million by 2012, 74 Million in 2021, and it is now 101 Million, according to the ICMR–INDIAB Study. This autoimmune disorder, commonly diagnosed in children and young adults, has seen a notable surge across urban and semi-urban populations. The rising incidence of Type 1 Diabetes is prompting significant investments in early diagnostic platforms, with a focus on improving glycemic control and disease monitoring. Healthcare systems are expanding their diagnostic infrastructure to manage growing pediatric and adolescent cases. The increase in Type 1 Diabetes patients is also driving innovation in test kits, especially those supporting rapid and accurate detection.

Europe Autoimmune Disease Diagnosis Market Analysis

Europe is seeing a rising prevalence of thyroid-related autoimmune disorders, particularly Hashimoto’s thyroiditis and Graves’ disease, which is leading to greater reliance on diagnostic technologies. Expansion of healthcare infrastructure across urban and rural areas is improving access to advanced autoimmune disease diagnostic services. For instance, Germany has more than 1,900 hospitals, including over 30 elite university hospitals, combining top-level patient care with research and innovation. Public health campaigns targeting thyroid awareness and increased physician focus on autoimmune symptoms are enhancing early detection. New investments in immunology labs and academic research centres are aiding diagnosis accuracy. Technological upgrades in laboratories and clinical support systems are boosting adoption further. Rising healthcare expenditure and the aging population are also contributing to broader diagnosis initiatives. With growing thyroid cases and investment on healthcare infrastructure in Europe, the region continues to strengthen its position in autoimmune disease diagnostics.

Latin America Autoimmune Disease Diagnosis Market Analysis

Latin America is witnessing increased autoimmune disease diagnosis adoption driven by rising incidences of lupus, rheumatoid arthritis, and celiac disease. Awareness campaigns and support from medical societies are prompting early clinical consultations. Expanding diagnostic facilities and greater availability of trained professionals are improving accessibility. For instance, Novo Nordisk plans to invest USD 1.09 Billion to boost Ozempic, Wegovy production in Brazil. As autoimmune diseases like lupus, rheumatoid arthritis, and celiac disease gain attention, diagnostic procedures are becoming more widespread. Rising focus on public healthcare support is contributing to enhanced diagnosis practices.

Middle East and Africa Autoimmune Disease Diagnosis Market Analysis

Middle East and Africa are undergoing rapid improvements in healthcare systems, leading to broader autoimmune disease diagnosis adoption. Growing healthcare facilities are increasing the availability of diagnostics in both urban and semi-urban areas. For the 2025 fiscal year, the UAE allocated AED 5.7 Billion, equivalent to 8% of the federal budget, to healthcare and community prevention services, reflecting its sustained commitment to developing the health sector. With more hospitals and laboratories being equipped for autoimmune screenings, patients now have better access to early-stage diagnostics. Expansion of medical infrastructure continues to support effective diagnosis in the region.

Competitive Landscape:

The autoimmune disease diagnostics market is seeing steady activity across product development, research, and collaborations. Diagnostic tools are becoming more precise, with new technologies enabling earlier and less invasive detection. Research groups and labs are working closely with diagnostics firms to bring innovations into clinical use more quickly. AI and machine learning are starting to influence test development, especially in pattern recognition and predictive diagnostics. Governments are showing more interest through national health strategies and dedicated funding for autoimmune conditions. Product launches and R&D remain the most consistent forms of progress, while formal partnerships and agreements are also frequent. Compared to others, large-scale fundraising or private investment announcements are less common right now. Most movement is driven by research and collaboration.

The report provides a comprehensive analysis of the competitive landscape in the autoimmune disease diagnosis market with detailed profiles of all major companies, including:

- Abbott Laboratories

- AESKU.GROUP

- Danaher Corp.

- bioMérieux SA

- Bio-Rad Laboratories, Inc.

- PerkinElmer Inc.

- Hemagen Diagnostics, Inc.

- Inova Diagnostics, Inc.

- Myriad Genetics, Inc.

- Quest Diagnostics Incorporated

- Siemens Healthineers AG

- SQI Diagnostics

- Thermo Fisher Scientific Inc.

- Trinity Biotech plc

Latest News and Developments:

- April 2025: Brian Freed, from the University of Colorado, pioneered gene-editing work on the HLA gene, aiming to block autoimmune diseases like rheumatoid arthritis. He co-founded RheumaGen, which used CU's research to develop cell therapies, and planned clinical trials for 2026.

- April 2025: Amgen announced that the FDA had approved UPLIZNA as the first and only treatment for IgG4-related disease, marking a major advancement in autoimmune diseases. The therapy had demonstrated an 87% reduction in flare risk and enabled corticosteroid-free, flare-free remission in the MITIGATE trial.

- February 2025: CIC biomaGUNE launched Taldeki Biosolutions to advance disease diagnosis using nanosensors, targeting autoimmune diseases among others. The company developed patented metal/protein hybrid sensors to enable rapid, cost-effective antibody detection and addressed limitations in traditional in vitro diagnostics.

Autoimmune Disease Diagnosis Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Consumables and Assay Kits, Instruments |

| Disease Types Covered |

|

| Test Types Covered | Routine Laboratory Tests, Inflammatory Markers, Autoantibodies and Immunologic Tests, Others |

| End-Users Covered | Clinical Laboratories, Hospitals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, AESKU.GROUP, Danaher Corp., bioMérieux SA, Bio-Rad Laboratories, Inc., PerkinElmer Inc., Hemagen Diagnostics, Inc., Inova Diagnostics, Inc., Myriad Genetics, Inc., Quest Diagnostics Incorporated, Siemens Healthineers AG, SQI Diagnostics, Thermo Fisher Scientific Inc., Trinity Biotech plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the autoimmune disease diagnosis market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the autoimmune disease diagnosis industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The autoimmune disease diagnosis market was valued at USD 3.4 Billion in 2024.

The autoimmune disease diagnosis market is projected to exhibit a CAGR of 5.57% during 2025-2033, reaching a value of USD 5.5 Billion by 2033.

Key factors driving the autoimmune disease diagnosis market include increasing prevalence of autoimmune disorders, rising awareness, improved diagnostic technologies, growing elderly population, and expanded healthcare access. Advancements in biomarkers and point-of-care testing are also contributing to faster, more accurate detection and early intervention.

North America dominated the autoimmune disease diagnosis market in 2024, accounting for a share of 39.7% due to advanced healthcare infrastructure, high awareness, strong reimbursement policies, and significant investment in diagnostic technologies and research across the region.

Some of the major players in the autoimmune disease diagnosis market include Abbott Laboratories, AESKU.GROUP, Danaher Corp., bioMérieux SA, Bio-Rad Laboratories, Inc., PerkinElmer Inc., Hemagen Diagnostics, Inc., Inova Diagnostics, Inc., Myriad Genetics, Inc., Quest Diagnostics Incorporated, Siemens Healthineers AG, SQI Diagnostics, Thermo Fisher Scientific Inc., Trinity Biotech plc, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)