Australia Semiconductor Packaging Market Size, Share, Trends and Forecast by Type, Packaging Material, Technology, End User, and Region, 2025-2033

Australia Semiconductor Packaging Market Overview:

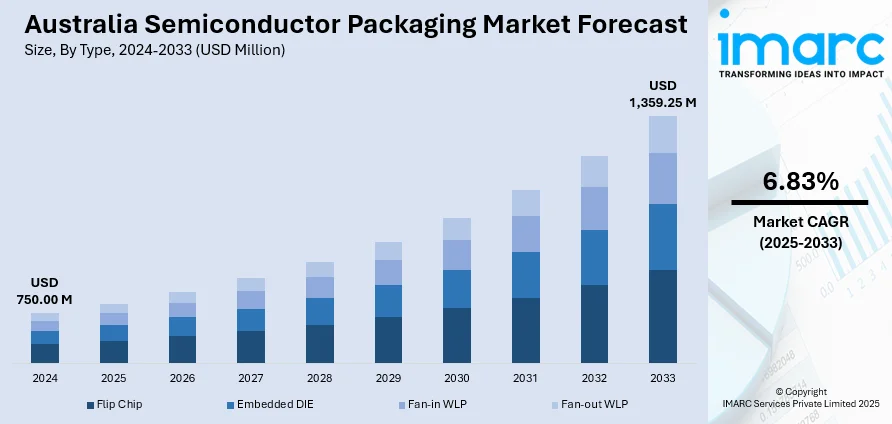

The Australia semiconductor packaging market size reached USD 750.00 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 1,359.25 Million by 2033, exhibiting a growth rate (CAGR) of 6.83% during 2025-2033. Rising domestic chip assembly investments, surging demand from electric vehicles (EVs), rapid fifth-generation (5G) network expansion, growing Internet of Things (IoT) adoption, local data center growth, development of defense electronics, miniaturization trends, burgeoning government focus on technology self-reliance, and adoption of advanced formats like 2.5D/3D integrated circuits (ICs), fan-out wafer-level packaging (FOWLP), and system-in-package (SiP) solutions are factors accelerating the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024 |

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 750.00 Million |

| Market Forecast in 2033 | USD 1,359.25 Million |

| Market Growth Rate 2025-2033 | 6.83% |

Australia Semiconductor Packaging Market Trends:

Rising Investments in Domestic Semiconductor Fabrication and Backend Infrastructure

Australia is increasingly working to develop its semiconductor ecosystem with increased investments in fabrication and backend packaging plants. While historically the country has depended on importation to meet semiconductor needs, recent strategic investment by government and private organizations are aimed at building up indigenous capabilities. For instance, the Australian government invested approximately USD 980 million in direct investment and financial incentives in 2024 to stimulate approximately USD 3.25 billion worth of semiconductor manufacturing activity. This scheme, spurred by analogous global efforts such as the U.S. Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Facilitating American-Built Semiconductors (FABS) Acts, offers subsidies and tax offsets that should attract private investors and even foreign semiconductor foundries. Moreover, onshore capacity is being pushed by the need to deliver supply chain security, particularly in light of recent global disruptions, which is facilitating the market growth. These investments also align with the country's overall ambitions of emerging as a regional technology manufacturing center, which is further driving the Australia semiconductor packaging market growth. With the integration of automated backend lines and cleanroom facilities, local companies are improving packaging output, reducing lead times, and offering customized solutions for niche markets.

To get more information on this market, Request Sample

Increasing Demand from Automotive Electronics

The shift toward electric vehicles (EVs), hybrid vehicles, and advanced driver-assistance systems (ADAS) is driving the semiconductor usage in country’s automotive market, creating demand for advanced packaging solutions. Packaging of automotive chips must withstand high thermal and mechanical stress without loss of reliability over extended periods. These packages are increasingly finding applications in powertrain control, battery management systems and in-vehicle infotainment, including quad flat no-leads (QFN), ball grid arrays (BGA), and system-in-package (SiP) configurations. Additionally, backend semiconductor demand is also receiving a bolster from the country’s growing interest in EV battery manufacturing and electric mobility startups. To mitigate risk of overseas procurement, automotive original equipment manufacturer (OEMs) & Tier 1 suppliers are reaching for local sourcing, which is providing a positive Australia semiconductor packaging market outlook.

Expansion of 5G and IoT Deployments

Australia’s growing investments in fifth-generation (5G) infrastructure and smart city initiatives are amplifying the demand for semiconductor devices and, consequently, advanced packaging solutions. The deployment of base stations, edge computing nodes, and connected sensors across urban and rural regions requires high-frequency, low-latency chips packaged with superior electrical and thermal performance. System-in-package (SiP) and flip-chip BGA technologies are becoming central to supporting compact, multi-functional wireless modules. In the IoT segment, which includes smart homes, agriculture, logistics, and utility management, there is a rising demand for ultra-low-power, compact chipsets. These rely on wafer-level chip scale packaging (WLCSP) and molded interconnect substrate (MIS) solutions to meet size and energy efficiency constraints. Apart from this, the country’s commitment to digital infrastructure development, supported by public funding and industry participation, is projected to drive sustained demand for localized and customized semiconductor packaging services, which is boosting the Australia semiconductor packaging market share.

Australia Semiconductor Packaging Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the region level for 2025-2033. Our report has categorized the market based on type, packaging material, technology, and end user.

Type Insights:

- Flip Chip

- Embedded DIE

- Fan-in WLP

- Fan-out WLP

The report has provided a detailed breakup and analysis of the market based on the type. This includes flip chip, embedded DIE, fan-in WLP, and fan-out WLP.

Packaging Material Insights:

- Organic Substrate

- Bonding Wire

- Leadframe

- Ceramic Package

- Die Attach Material

- Others

A detailed breakup and analysis of the market based on the packaging material have also been provided in the report. This includes organic substrate, bonding wire, leadframe, ceramic package, die attach material, and others.

Technology Insights:

- Grid Array

- Small Outline Package

- Flat no-leads Package

- Dual In-Line Package

- Others

The report has provided a detailed breakup and analysis of the market based on the technology. This includes grid array, small outline package, flat no-leads package, dual in-line package, and others.

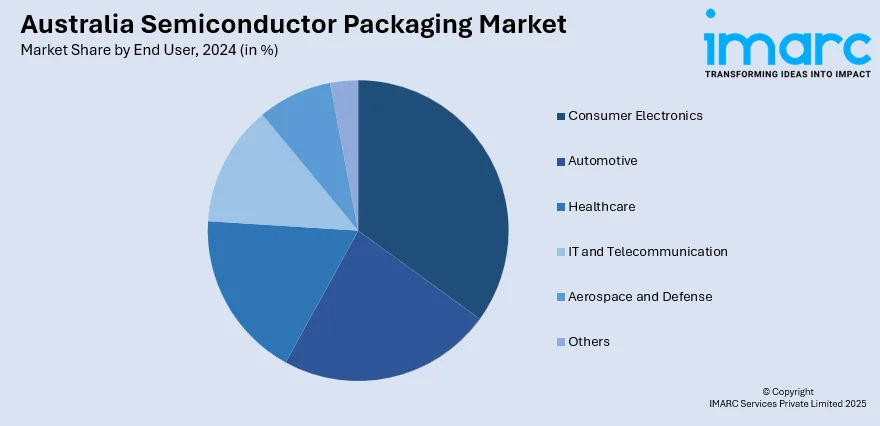

End User Insights:

- Consumer Electronics

- Automotive

- Healthcare

- IT and Telecommunication

- Aerospace and Defense

- Others

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes consumer electronics, automotive, healthcare, it and telecommunication, aerospace and defense, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Semiconductor Packaging Market News:

- In 2024, BluGlass Limited, based in Silverwater, NSW, announced the installation of commercial-scale semiconductor equipment at its facility. This installation marks a significant step in enhancing their manufacturing capabilities, particularly in the packaging of gallium nitride (GaN) lasers. The new equipment is expected to streamline production processes and improve the quality and reliability of their laser products.

Australia Semiconductor Packaging Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | USD Million |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Flip Chip, Embedded DIE, Fan-in WLP, Fan-out WLP |

| Packaging Materials Covered | Organic Substrate, Bonding Wire, Leadframe, Ceramic Package, Die Attach Material, Others |

| Technologies Covered | Grid Array, Small Outline Package, Flat No-Leads Package, Dual In-Line Package, Others |

| End Users Covered | Consumer Electronics, Automotive, Healthcare, IT and Telecommunication, Aerospace and Defense, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Australia semiconductor packaging market performed so far and how will it perform in the coming years?

- What is the breakup of the Australia semiconductor packaging market on the basis of type?

- What is the breakup of the Australia semiconductor packaging market on the basis of packaging material?

- What is the breakup of the Australia semiconductor packaging market on the basis of technology?

- What is the breakup of the Australia semiconductor packaging market on the basis of end user?

- What is the breakup of the Australia semiconductor packaging market on the basis of region?

- What are the various stages in the value chain of the Australia semiconductor packaging market?

- What are the key driving factors and challenges in the Australia semiconductor packaging?

- What is the structure of the Australia semiconductor packaging market and who are the key players?

- What is the degree of competition in the Australia semiconductor packaging market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia semiconductor packaging market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia semiconductor packaging market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia semiconductor packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)