Australia Pharmaceutical Market Size, Share, Trends and Forecast by Therapeutic Class, Drug Type, Prescription Type, and Region, 2026-2034

Australia Pharmaceutical Market Size & Forecast 2026-2034

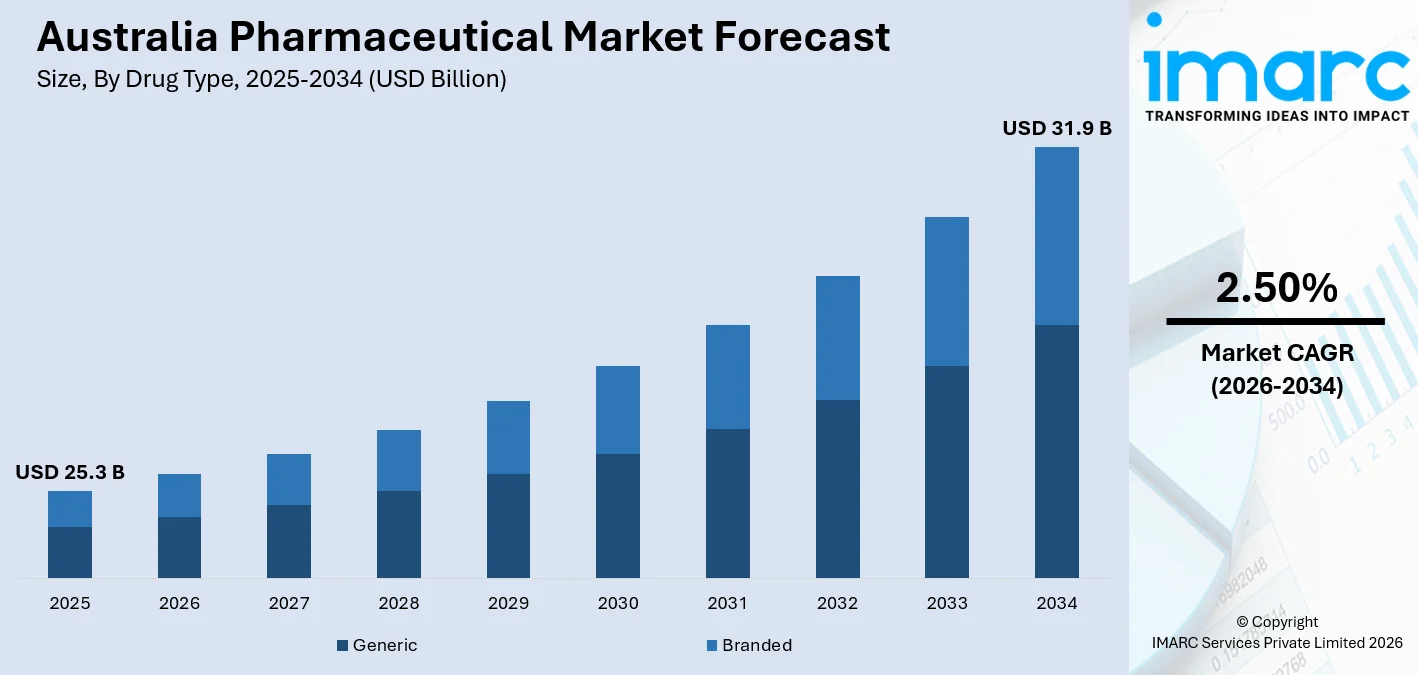

The Australia pharmaceutical market size, valued at USD 25.3 Billion in 2025, is projected to reach USD 31.9 Billion by 2034, growing at a CAGR of 2.50% from 2026-2034, driven by the Pharmaceutical Benefits Scheme (PBS) expanding access to high-cost oncology biologics, a rapidly ageing population, and rising government support. The Australian government earmarked $3.2 billion in the budget to support the reforms, representing an investment in health, productivity, and the well-being of households.

To get more information on this market Request Sample

Australia Pharmaceutical Industry Analysis - Key Insights

- Antineoplastic and immunomodulating agents command 18.6% of the market by therapeutic class in 2025 - reflecting structural premium pricing, these agents account for approximately one third of PBS expenditure.

- Generic drugs account for the largest market share of 57.4% in the drug type segment in 2025 - anchored by PBS price disclosure policies that structurally reward generic substitution and price reduction of approximately 31%.

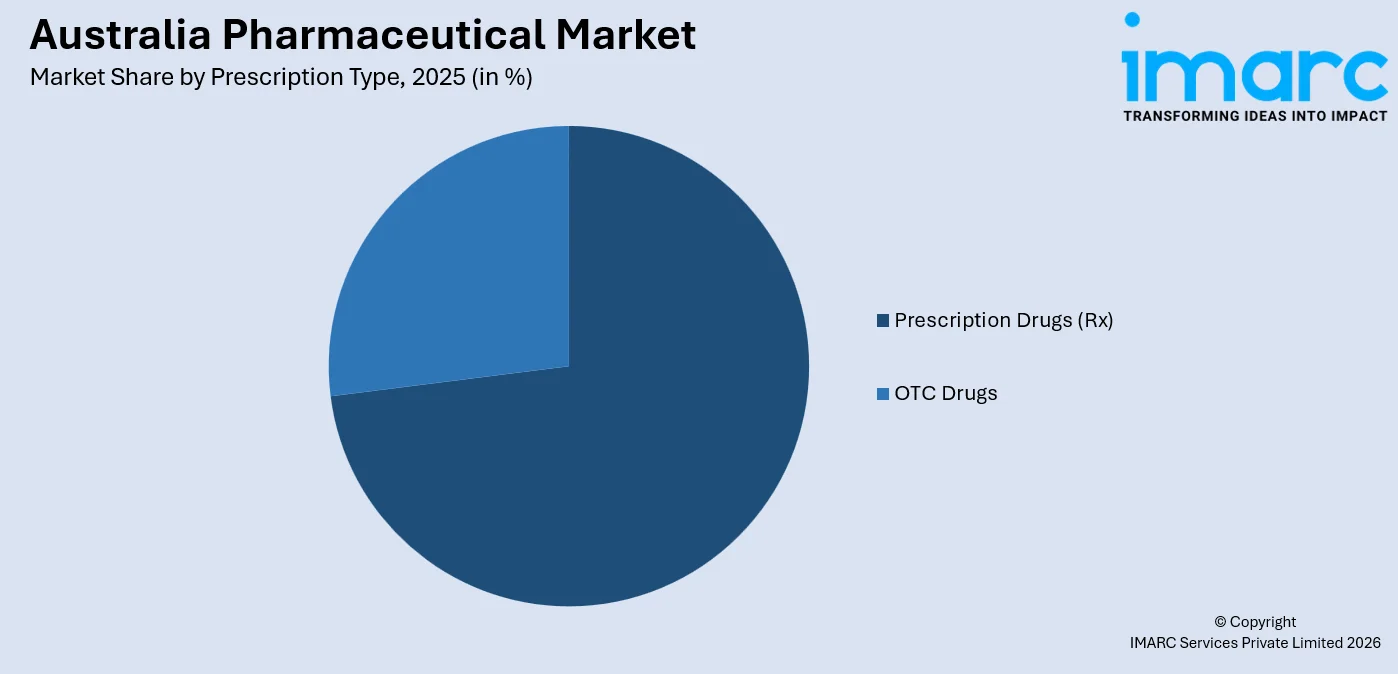

- Prescription drugs (Rx) dominate at 72.9% of the prescription type segment in 2025 - driven by the PBS subsidy model that channels most drug spend through physician scripts, complex biologic therapies, and strict therapeutic guidelines for high-cost PBS-listed medicines.

- Australia Capital Territory & New South Wales leads regionally at 35.8% in 2025 - underpinned by Sydney's dense specialist hospital network, national pharmaceutical headquarters presence, and high government healthcare expenditure per capita.

Australia Pharmaceutical Market Trends and Dynamics 2026

Market Trends

Rapid expansion of oncology biologics and targeted therapies on the PBS

Australia's oncology segment is the single largest therapeutic class driver, with antineoplastic and immunomodulating agents absorbing an average AUD 259 per person in PBS government expenditure annually. This expansion is tightly linked to the cancer burden, with Australia registering over 165,000 new cancer diagnoses annually, an average of over 450 every day, with 55% cases diagnosed in males in 2023, with diagnosis rates outpacing population growth due to an ageing demographic profile.

Surge in electronic prescriptions and digital dispensing reshaping distribution

Australia's pharmaceutical distribution landscape is being restructured by digital health adoption. More than 219 million electronic prescriptions have been issued since 2020 by over 85,000 prescribers, enabling prescriptions to be sent electronically to any licensed pharmacy nationwide. The Australia pharmaceutical market trends toward online pharmacy consolidation are accelerating, with e-pharmacies growing the fastest among all distribution channels.

Biosimilar adoption is accelerating under government uptake drivers

Australia's biosimilar landscape is maturing rapidly. In April 2025, Sandoz's Tyruko, a biosimilar of Biogen's Tysabri (natalizumab), was approved by Australia's Therapeutic Goods Administration (TGA). The lower price of biosimilars, demonstrating significant cost relief within the oncology supportive care portfolio.

- Personalized Medicine and Genomics: TGA priority-review pathways are shortening approval timelines for gene therapies and precision oncology agents.

- Domestic API Manufacturing Investment: Government grants are stimulating onshore manufacturing of antimicrobials, injectables, and mRNA vaccines, reducing Australia's heavy import dependence for active pharmaceutical ingredients.

- Life Saving Drugs Program Expansion: The LSDP, which fully subsidises high-cost transformational therapies for rare diseases outside the PBS, is growing its medicine roster and extending access to patients with conditions previously excluded from public funding.

Growth Drivers

Ageing population and rising chronic disease burden

According to the Australian Bureau of Statistics (ABS), the number of Australians aged 85 and older is expected to double by 2042, surpassing 1 million people. The demand for pharmaceuticals in Australia is expected to grow rapidly, as the growing aging population needs multiple medications to manage various health conditions.

Commonwealth Budget healthcare investment and PBS expansion

Federal healthcare investment is directly expanding pharmaceutical demand. The Budget allocated AUD 3.2 billion toward cheaper medicines in 2025–26, this government budget on cheaper medicines accelerating the market growth. An AUD 7.9 billion investment targets universal bulk-billing coverage for 9 in 10 GP visits by 2030, expanding the volume of consultations that generate pharmaceutical prescriptions.

TGA regulatory modernization enabling faster drug launches

TGA priority-review pathways for novel biologics and rolling submissions for rare-disease therapies are shortening regulatory lead times, enabling faster commercialization of high-value medicines. In February 2025, the Australian Therapeutic Goods Administration (TGA) approved Alovtech and Cipla’s Uteknix, a biosimilar to J&J/Janssen’s Stelara (ustekinumab). The Australia pharmaceutical market outlook is reinforced by these streamlined regulatory approvals.

- PBS Reimbursement Sustainability Model: Price disclosure mechanisms, biosimilar uptake drivers, and cost-sharing arrangements are enabling the PBS to list more innovative treatments while managing net expenditure growth.

- Expanding Specialist Hospital Infrastructure: Growing complex care capacity across corporate hospital chains is driving demand for high-cost injectable biologics, oncology infusions, and critical-care medicines requiring hospital pharmacy dispensing.

- Digital Health Integration and Tele-Prescribing: E-prescription legislation, mobile health apps, and telehealth consultations are reducing geographic barriers to pharmaceutical access.

Market Restraints

PBS pricing pressure and price disclosure erosion: Australia's PBS price disclosure regime triggers automatic subsidy reductions as market competition intensifies, progressively compressing originator revenues after generic or biosimilar entry.

Heavy import dependence and supply chain vulnerabilities: Australia depends on imports for the vast majority of its active pharmaceutical ingredients, exposing the market to foreign exchange volatility, geopolitical supply disruptions, and extended procurement lead times during global demand surges.

Regulatory complexity and reimbursement uncertainty: The PBAC's stringent cost-effectiveness standards and multi-stage submission requirements create lengthy timelines between TGA registration and PBS listing, delaying patient access to innovative therapies and increasing commercial uncertainty for pharmaceutical sponsors.

Australia Pharmaceutical Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Therapeutic Class | Antineoplastic and Immunomodulating Agents | 18.6% | 2025 |

| Drug Type | Generic | 57.4% | 2025 |

| Prescription Type | Prescription Drugs (Rx) | 72.9% | 2025 |

| Region | Australia Capital Territory & New South Wales | 35.8% | 2025 |

Therapeutic Class Insights

Antineoplastic and Immunomodulating Agents - 18.6% market share (2025) | Leading Therapeutic Class

Antineoplastic and immunomodulating agents represent the highest-expenditure therapeutic class in Australia, with Pharmaceutical Benefits Scheme (PBS) government spending averaging AUD 259 per person annually, significantly exceeding all other medicine categories. The PBAC recommended 137 out of 182 cancer medicine indications for PBS funding, with monoclonal antibodies and protein kinase inhibitors constituting the two largest oncology subcategories.

|

Segment Breakdown Antineoplastic and Immunomodulating Agents (18.6%) · Alimentary Tract and Metabolism · Blood and Blood Forming Organs · Cardiovascular System · Dermatologicals · Genito Urinary System and Sex Hormones · Systemic Hormonal Preparations · Anti-infectives for Systemic Use · Musculoskeletal System · Nervous System · Antiparasitic Products, Insecticides, and Repellents · Respiratory System, Sensory Organs · Others |

Drug Type Insights

Generic - 57.4% market share (2025) | Leading Drug Type

Generic medicines dominate the market. The Commonwealth’s partnership with Medicines Australia and the Generic and Biosimilar Medicines Association (GBMA) strengthens its ongoing collaboration with Australia’s pharmaceutical industry, further accelerating the pace of price disclosure adjustments, structurally expanding the generic market's volume and revenue share.

|

Segment Breakdown Generic (57.4%) · Branded |

Prescription Type Insights

Access the comprehensive market breakdown Request Sample

Prescription Drugs (Rx) - 72.9% market share (2025) | Leading Prescription Type

Prescription medicines dominate the market. In 2023, an annual average of 13 PBS-funded prescriptions were dispensed per person, with the national average government cost reaching AUD 641 per capita, a 13% increase over the prior year. PBS authority requirements for high-cost biologics and oncology agents ensure that prescription-only pathways remain entrenched for the most expensive and highest-value market segments. The Australia pharmaceutical market forecast reflects sustained Rx dominance as biologic and specialty medicine listings continue to expand through the PBAC pipeline.

|

Segment Breakdown Prescription Drugs (Rx) (72.9%) · OTC Drugs |

Regional Insights

Australia Capital Territory & New South Wales - 35.8% market share (2025) | Leading Region

Australia Capital Territory & New South Wales constitutes the dominant pharmaceutical region, anchored by Sydney's concentration of specialist hospitals, the operational headquarters of major multinationals, and the ACT's disproportionately high government healthcare expenditure per capita. In July 2025, Neuraxpharm launched its Australian affiliate, Neuraxpharm Australia, focused on CNS products with Sydney as its operational center, reflecting the region's appeal for new market entrants.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

35.8%

|

|

Major Growth Drivers

|

Specialist hospital density, multinational headquarters cluster, TGA regulatory hub, highest absolute PBS script volume |

|

Outlook

|

Sustained regional leadership with biologic and specialty growth |

|

Regional Breakdown Australia Capital Territory & New South Wales (35.8%) · Victoria & Tasmania · Queensland · Northern Territory & Southern Australia · Western Australia |

Victoria & Tasmania:

Victoria is Australia's second-largest pharmaceutical market. The state hosts significant pharmaceutical manufacturing infrastructure and clinical trial activity. In November 2024, Race Oncology completed a therapeutic development program at Monash University's Fragment Platform, identifying 39 molecular candidates for FTO-targeting compounds, demonstrating Victoria's active role in early-stage drug discovery and pipeline development that underpins long-term market demand.

|

Metric

|

Details

|

|---|---|

|

Major Growth Drivers

|

Melbourne research precinct, clinical trial density, private hospital network, manufacturing infrastructure |

|

Outlook

|

Strong growth led by Melbourne biomedical cluster |

Queensland:

Queensland is expanding its pharmaceutical market through state-level pharmacist prescribing pilots that are broadening primary care access and shifting chronic-disease maintenance prescriptions from specialist to community pharmacy settings. The state's rapidly growing population and above-average rates of lifestyle-related chronic disease, including type 2 diabetes, cardiovascular conditions, and respiratory disease, are generating structural demand growth.

|

Metric

|

Details

|

|---|---|

|

Major Growth Drivers

|

Population growth, pharmacist prescribing pilots, lifestyle disease burden, Medicare Urgent Care Clinic expansion |

|

Outlook

|

Robust growth via community pharmacy channel expansion |

Northern Territory & Southern Australia:

The Northern Territory presents a distinctive pharmaceutical market challenge, characterized by geographically dispersed populations, a high proportion of First Nations communities with elevated chronic disease burden, and logistics constraints for temperature-sensitive medicines in remote settings. The Northern Territory had the lowest absolute script volume and per-capita expenditure among all Australian states and territories.

|

Metric

|

Details

|

|---|---|

|

Major Growth Drivers

|

Tertiary hospital network, above-average per-capita PBS rates, rural health funding, chronic disease management programs |

|

Outlook

|

Moderate growth driven by South Australia urban demand |

Western Australia:

Western Australia's pharmaceutical market is driven by Perth's growing tertiary care infrastructure, above-average state government healthcare expenditure underpinned by mining-sector economic strength and rising private health insurance coverage among a higher-income demographic cohort. The state's population is growing faster than the national average, and investment is expanding specialist care capacity that generates PBS-linked prescription demand.

|

Metric

|

Details

|

|---|---|

|

Major Growth Drivers

|

Population growth, mining-sector income premium, expanding tertiary hospital capacity, high private health insurance rates |

|

Outlook

|

Steady growth driven by Perth hospital expansion |

Market Outlook 2026-2034

What is the future outlook of the Australia pharmaceutical market?

The Australia pharmaceutical market is expected to sustain steady revenue growth through 2034.

Australia's pharmaceutical market is well-positioned for sustained, steady expansion through 2034, supported by a structurally ageing population, an expanding PBS medicine list, and continued government commitment to universal medicine affordability. Biosimilar penetration across high-value biologics classes will moderate expenditure growth while enabling the PBAC to list additional innovative therapies. Digital health integration, 60-day dispensing, and pharmacist prescribing expansion will broaden patient access and increase the Australia pharmaceutical market trends toward chronic-disease adherence and community-based dispensing models, collectively underpinning the market growth.

Australia Pharmaceutical Market - Leading Key Players

The Australia pharmaceutical market is shaped by a concentrated group of multinational pharmaceutical corporations competing on PBS reimbursement expertise, pharmacoeconomic evidence generation, and supply chain resilience.

| Company | Leading Brands | Highlights |

|---|---|---|

| AbbVie Inc. | Humira (adalimumab), Skyrizi, Rinvoq | Relocating Sydney headquarters to new CBD location in late 2026; market leader in adalimumab with strong PBS position maintained through originator and brand strategy across biosimilar competition |

| Amgen Inc. | Prolia, Xgeva, Repatha, Enbrel | Secured five new denosumab brand registrations (November 2024) to preempt biosimilar competition; strong oncology supportive care and bone health portfolio backed by PBAC-funded PBS indications |

| AstraZeneca | Tagrisso, Imfinzi, Forxiga, Farxiga | PBS listings added for chronic obstructive pulmonary disease (COPD); Sydney-headquartered regional leadership with deep oncology and cardiovascular PBS portfolio across Australian clinical networks |

Some of the other key market players in Australia pharmaceutical market are CSL Limited, Eli Lilly Australia Pty Ltd, GSK plc, Merck KGaA, Novartis Pharmaceuticals Australia Pty Ltd., Pfizer Australia Pty Ltd., Roche Australia, and Sanofi, etc.

Latest Development & News

- In October 2025, Algorae Pharmaceuticals signed a binding term sheet with Cadila Pharmaceuticals Limited for a proposed license and supply agreement. As part of the agreement, Algorae plans to launch two generic medicines in Australia, focusing on key therapeutic areas such as cardiovascular and metabolic disorders.

- In July 2025, Ego Pharmaceuticals announced a major step forward in its commitment to Australian manufacturing with the launch of a $156 million investment spread over the next decade. The investment includes the opening of the cutting-edge Zorzi Innovation Centre (ZInC), the Green Core sustainability initiative, a new cream filling line, and expanded warehouse operations.

- In July 2025, Biocon Biologics, the biosimilars division of Biocon, announced the launch of Nepexto, a biosimilar for autoimmune diseases, in Australia through its local partner, Generic Health. Nepexto is a biosimilar to Enbrel (etanercept), which is marketed by Amgen.

Australia Pharmaceutical Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Therapeutic Classes Covered | Alimentary Tract and Metabolism, Blood and Blood Forming Organs, Cardiovascular System, Dermatologicals, Genito Urinary System and Sex Hormones, Systemic Hormonal Preparations, Anti-infectives for Systemic Use, Antineoplastic and Immunomodulating Agents, Musculoskeletal System, Nervous System, Antiparasitic Products, Insecticides, and Repellents, Respiratory System, Sensory Organs, Others |

| Drug Types Covered | Branded, Generic |

| Prescription Types Covered | Prescription Drugs (Rx), OTC Drugs |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | AbbVie Inc., Amgen Inc., AstraZeneca, CSL Limited, Eli Lilly Australia Pty Ltd, GSK plc, Merck KGaA, Novartis Pharmaceuticals Australia Pty Ltd., Pfizer Australia Pty Ltd., Roche Australia, Sanofi, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia pharmaceutical market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Australia pharmaceutical market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia pharmaceutical industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The Australia pharmaceutical market was valued at USD 25.3 Billion in 2025.

The Australia pharmaceutical market is anticipated to reach a value of USD 31.9 Billion by 2034.

Antineoplastic and immunomodulating agents dominate the market with a share of 18.6% in 2025, driven by premium-priced oncology biologics, PBS reimbursement for checkpoint inhibitors and antibody-drug conjugates, and accelerating cancer incidence in Australia's ageing population.

Generic dominates the market with a share of 57.4% in 2025, underpinned by PBS price disclosure policies that structurally reward generic substitution and the price reduction triggered when the first generic or biosimilar brand enters each medicine class.

Prescription drugs (Rx) dominate the market with a share of 72.9% in 2025, reflecting the PBS subsidy model that channels pharmaceutical demand through physician scripts and enforces authority prescription requirements for high-cost biologic and specialty medicines.

Australia Capital Territory & New South Wales currently leads the market, accounting for a share of 35.8%. The region's dominance is supported by Sydney's multinational headquarters cluster, the nation's highest absolute PBS script volume in New South Wales.

Some of the major players in the market include AbbVie Inc., Amgen Inc., AstraZeneca, CSL Limited, Eli Lilly Australia Pty Ltd, GSK plc, Merck KGaA, Novartis Pharmaceuticals Australia Pty Ltd., Pfizer Australia Pty Ltd., Roche Australia, and Sanofi, etc.

Key emerging trends include accelerating adoption of pharmacist prescribing pilots across Queensland and Victoria, consolidation among online and e-pharmacy platforms driven by growing 60-day dispensing uptake, increasing clinical trial activity supporting early adoption of novel oncology agents, and government-backed domestic API manufacturing investment reducing import vulnerability across priority medicine categories including antimicrobials and injectables.

Growth is driven by Australia's over-65 population exceeding 4.2 million and growing, the Commonwealth Budget's AUD 3.2 billion medicines affordability commitment reducing co-payment barriers, Ego Pharmaceuticals' AUD 156 million Zorzi Innovation Center supporting onshore manufacturing, accelerating TGA biosimilar approvals expanding competition in biologic classes, and digital health adoption through 219 million cumulative e-prescriptions enabling broader access channels.

The Australia pharmaceutical market faces PBS price disclosure erosion that compresses originator revenues after generic or biosimilar entry; heavy dependence on imported active pharmaceutical ingredients exposing the market to supply chain disruptions and currency volatility; lengthy PBAC reimbursement timelines between TGA registration and PBS listing; and cold-chain logistics constraints in remote and regional areas that limit effective penetration of temperature-sensitive biologic medicines beyond metropolitan centers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)