Australia Oil and Gas Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Australia Oil and Gas Market Size, Share, Trends & Forecast (2026-2034)

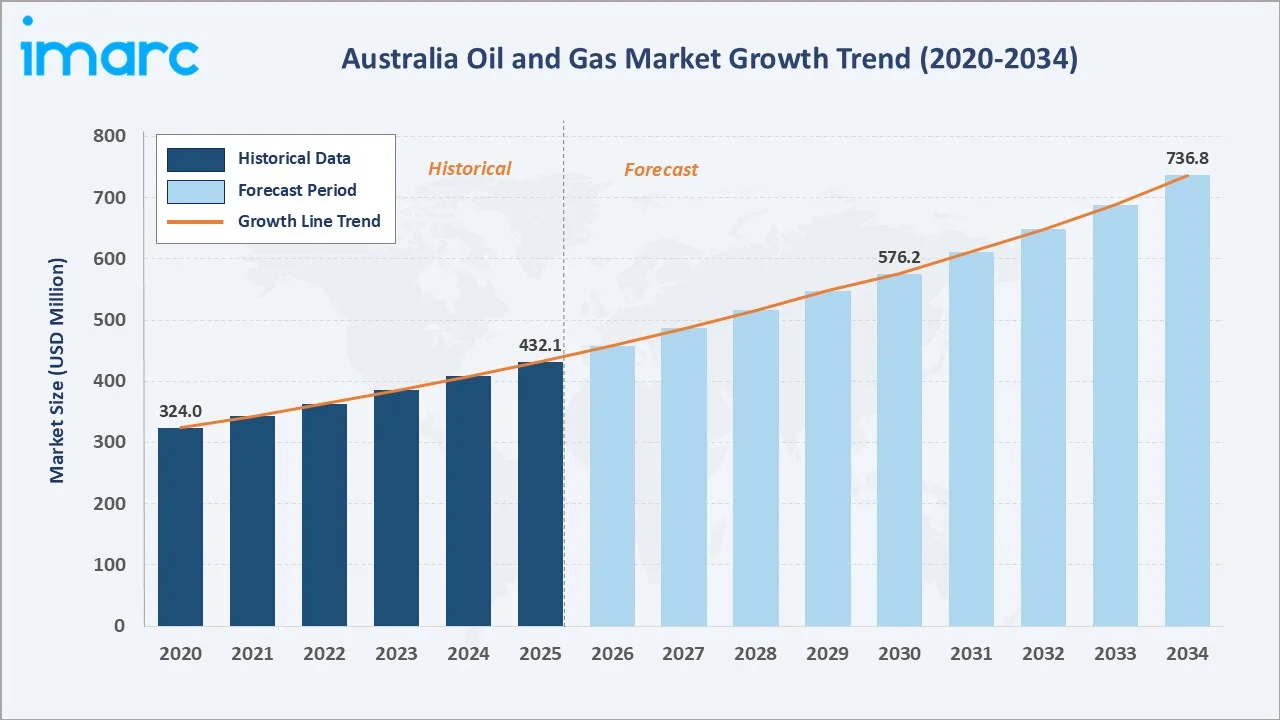

The Australia oil and gas market size reached USD 432.1 Million in 2025 and is projected to reach USD 736.8 Million by 2034, exhibiting a CAGR of 5.93% during 2026-2034. Growing Asian energy demand, LNG export expansion, infrastructure investment, and strategic government support are the primary growth forces shaping this market.

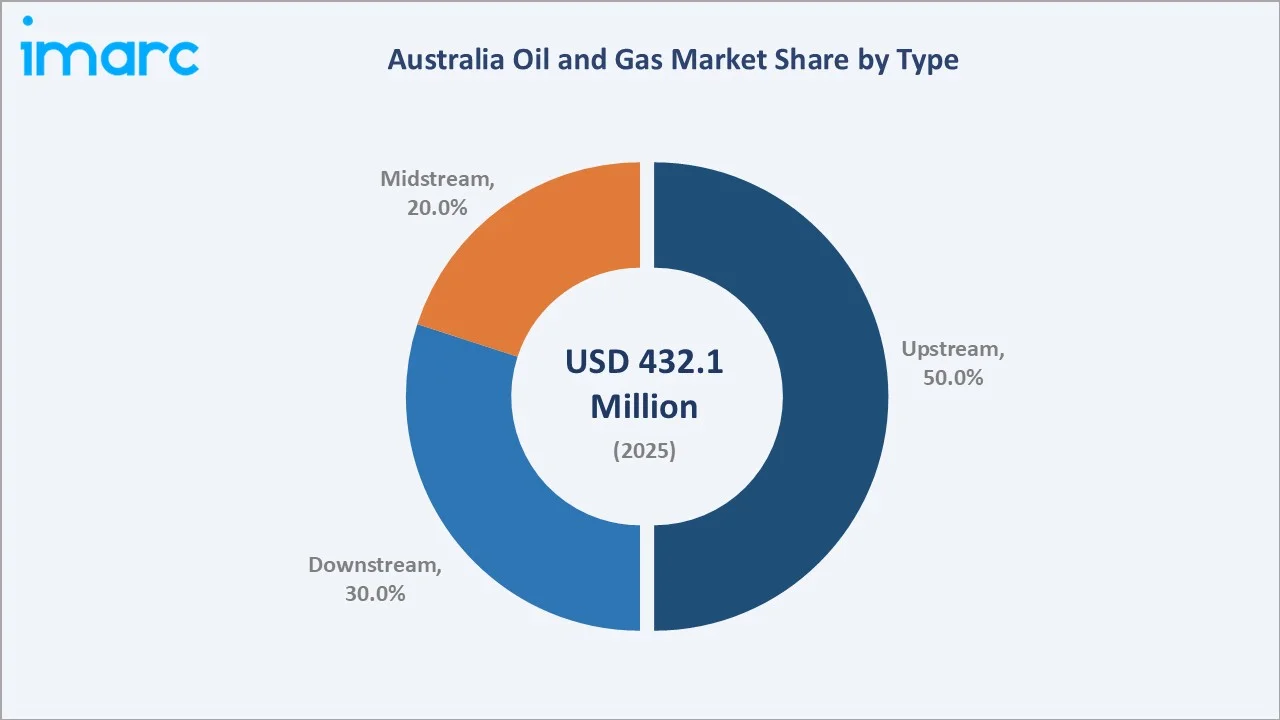

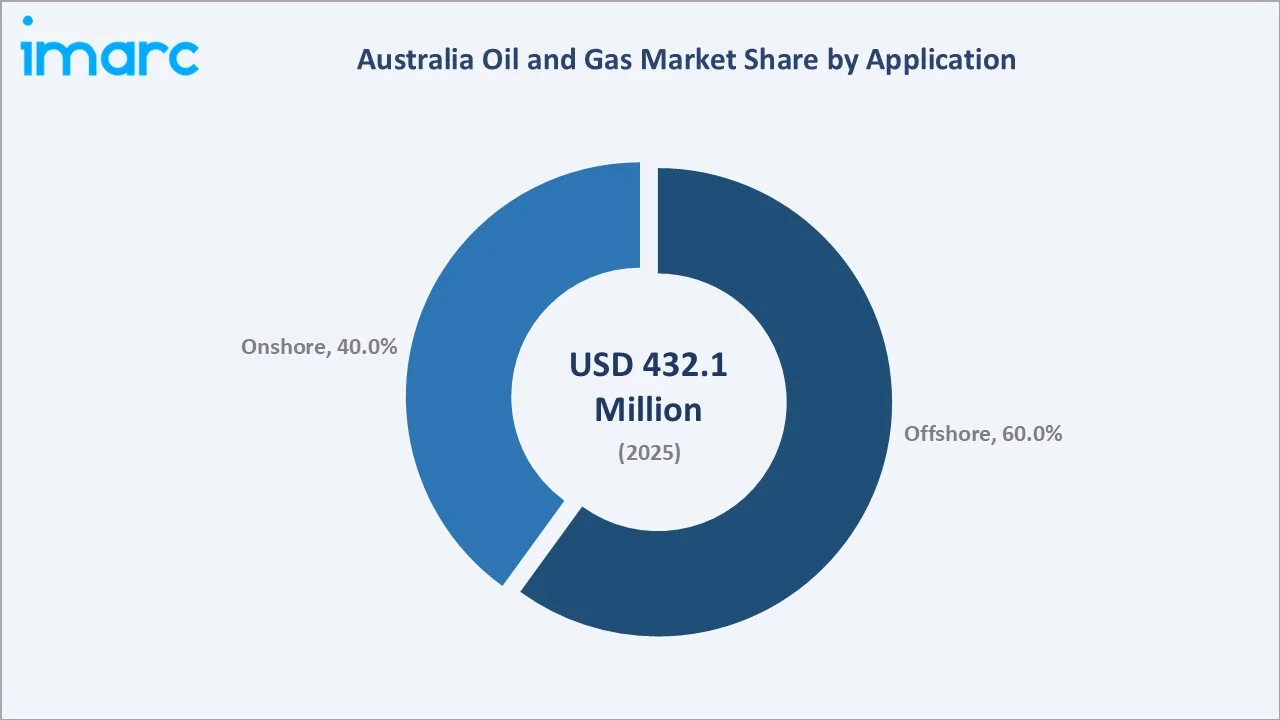

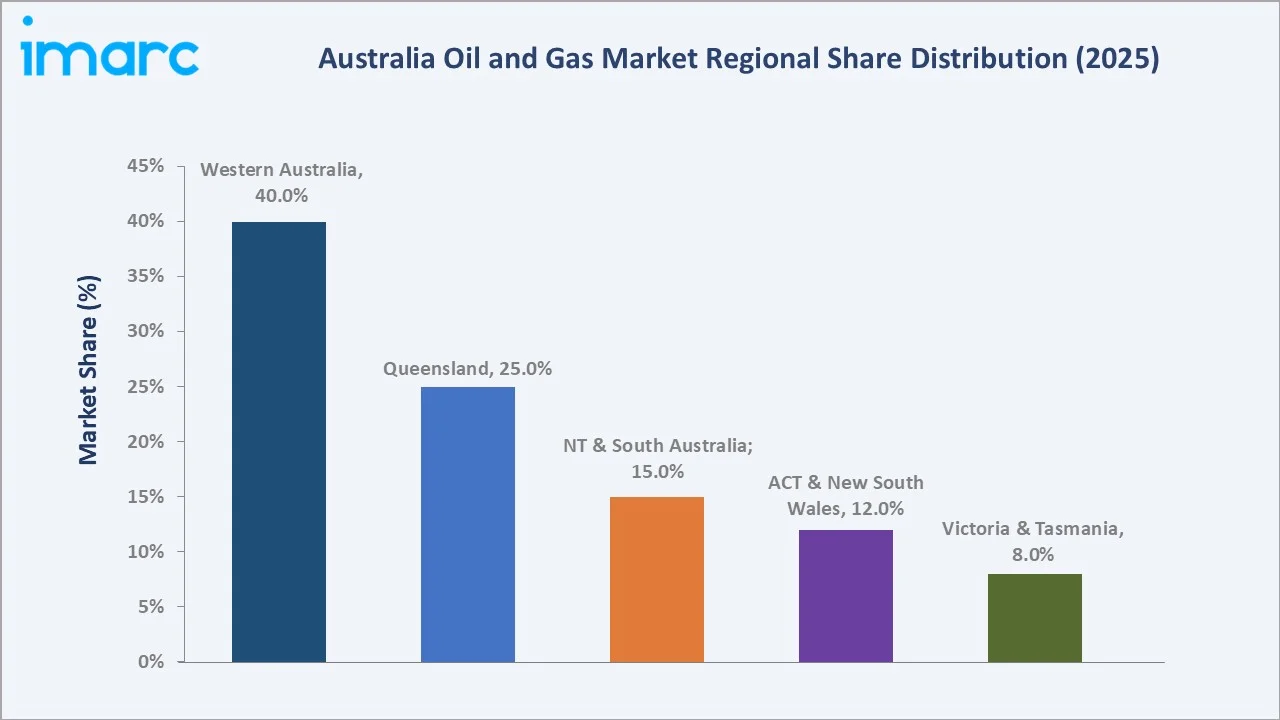

Upstream leads type segmentation at 50.0% in 2025, driven by exploration and production activities from Australia's prolific offshore basins. Offshore commands 60.0% application share, reflecting deep-water LNG project concentration. Western Australia dominates the regional landscape with a 40.0% share, underpinned by world-scale LNG infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 432.1 Million |

|

Forecast Market Size (2034) |

USD 736.8 Million |

|

CAGR (2026-2034) |

5.93% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Type |

Upstream (50.0% share, 2025) |

|

Leading Application |

Offshore (60.0% share, 2025) |

|

Leading Region |

Western Australia (40.0% share, 2025) |

The Australia oil and gas market growth trajectory from 2020 through 2034 reflects consistent demand driven by LNG export growth and recovering upstream investment. The forecast to USD 736.8 Million by 2034 captures accelerating offshore development, rising Asian energy imports, and sustained upstream capital expenditure across Western Australia.

To get more information on this market, Request Sample

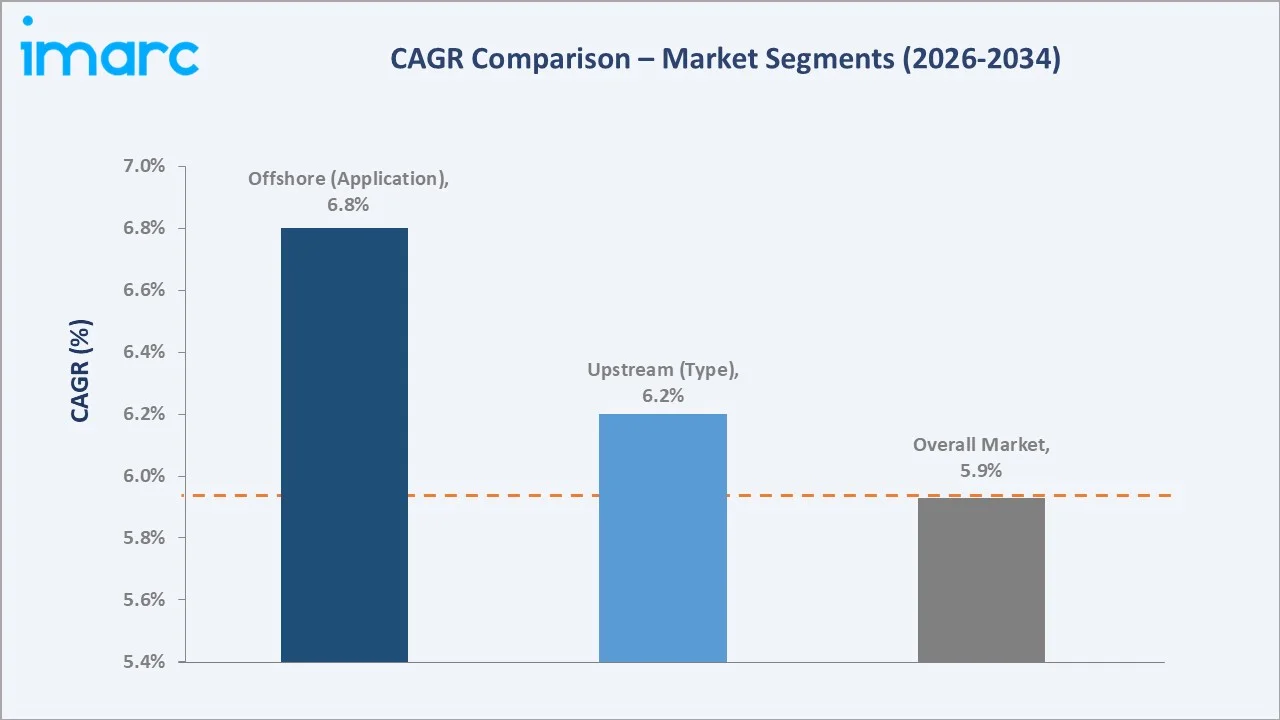

The CAGR trajectories across key type and application sub-segments highlight Offshore at approximately 6.80% CAGR and Upstream at approximately 6.20% CAGR as the fastest-growing categories within the Australia oil and gas market through 2034.

Executive Summary

The Australia oil and gas market is on a sustained growth trajectory from USD 432.1 Million in 2025 to USD 736.8 Million by 2034. The sector encompasses upstream exploration, midstream processing, and downstream refining, benefiting from Asia's transitional energy demand and Australia's world-class LNG export infrastructure.

Upstream leads type at 50.0% in 2025 owing to its critical role in resource discovery and production from prolific basins in Western Australia and Queensland. Downstream (30.0%) captures LNG liquefaction and refining value, while Midstream (20.0%) encompasses the pipeline and processing infrastructure linking production to markets.

Offshore commands 60.0% application share in 2025, reflecting Australia's strategic deep-water reserves in the Browse, Carnarvon, and Bonaparte basins. Onshore (40.0%) encompasses Cooper Basin gas production, Queensland coal seam gas, and Northern Territory unconventional resources critical to domestic energy supply and LNG feedstock.

Western Australia dominates at 40.0% in 2025, underpinned by offshore LNG projects and major operator headquarters. Queensland follows at 25.0%, driven by coal seam gas and LNG export activities from Gladstone's three-train LNG complex serving long-term Asian supply contracts.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Upstream – 50.0% share (2025) |

|

Leading Application |

Offshore – 60.0% share (2025) |

|

Leading Region |

Western Australia – 40.0% share (2025) |

|

Second Largest Region |

Queensland – 25.0% share (2025) |

|

Top Companies |

BP p.l.c., Chevron Corporation, Origin Energy Limited, Santos Ltd, and Woodside Energy, among others. |

Key Analytical Observations Expanding on the Above Data:

- Upstream, at 50.0% in 2025, dominates because Australia's energy value is overwhelmingly concentrated in resource extraction. The Carnarvon, Browse, and Bonaparte basins anchor production, while Queensland's coal seam gas fields supply three world-scale LNG trains serving decades-long supply contracts with Japan, China, and South Korea.

- Offshore commands 60.0% share because Australia's most prolific hydrocarbon accumulations lie beneath the continental shelf. Deepwater LNG projects—Gorgon, Wheatstone, Prelude, Ichthys—represent multi-decade production commitments and collectively position Australia among the world's top three LNG exporters by volume.

- Western Australia's 40.0% regional dominance reflects its unrivalled concentration of offshore LNG infrastructure. The North West Shelf, Gorgon, and Wheatstone projects represent over USD 90 billion in combined capital investment, ensuring sustained production volumes and export revenues through the forecast horizon to 2034.

- Offshore applications, growing at approximately 6.80% CAGR, are accelerated by new deepwater exploration in the Browse Basin, the Scarborough gas field development by Woodside Energy, and continued capital investment in offshore floating LNG technology that unlocks previously stranded gas reserves at commercially viable production costs.

Australia Oil and Gas Market Overview

The Australia oil and gas market encompasses upstream exploration and production, midstream processing and pipeline transport, and downstream refining and LNG export operations. The market structure integrates major international operators, independent producers, pipeline owners, and LNG export consortia serving long-term Asian supply agreements.

The ecosystem integrates global energy majors, domestic independent producers, infrastructure owners, government resource agencies, environmental regulators, and end consumers spanning domestic industrial users, power generators, and international LNG buyers across Japan, China, South Korea, and emerging Asian economies.

Market Dynamics

To evaluate market opportunities, Request Sample

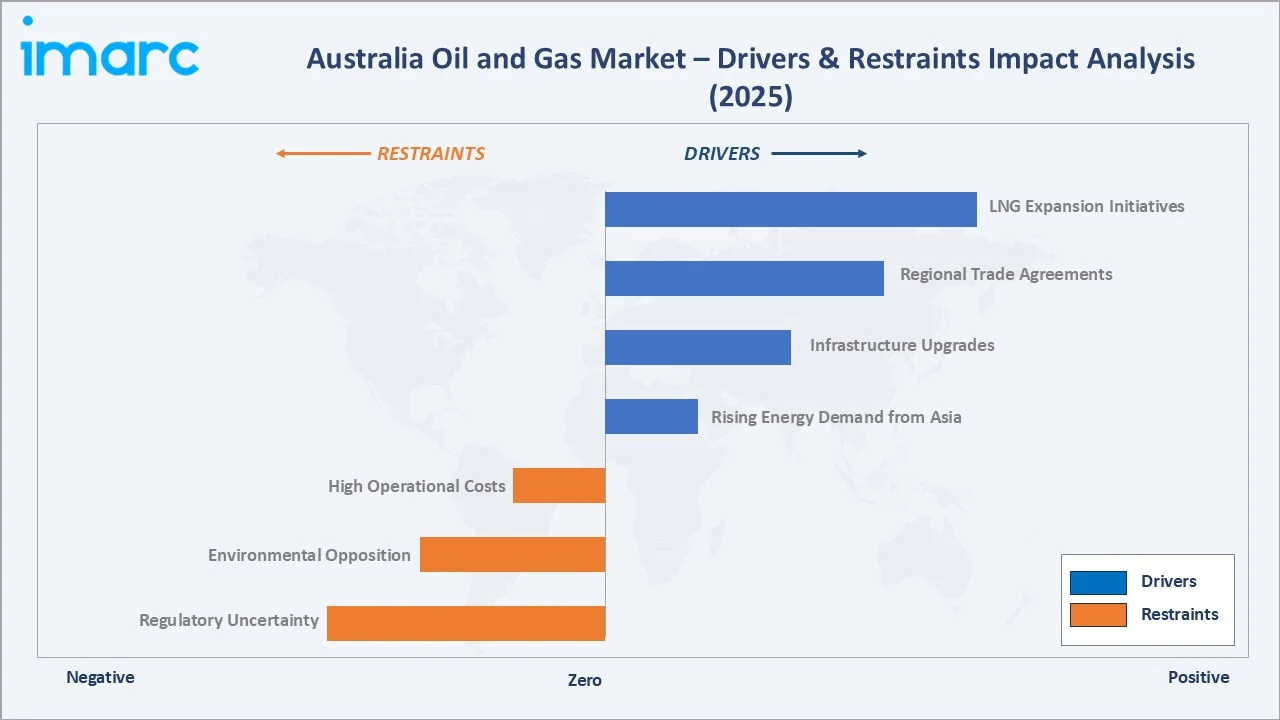

Market Drivers

- LNG Expansion Initiatives: Australia is investing significantly to expand its LNG sector, responding to rising demand from Asian markets. New facilities and terminal upgrades are boosting export capacity, generating employment, and extending the productive life of major gas fields, solidifying Australia's long-term role in the global energy supply network.

- Regional Trade Agreements: Australia's strategic location and diplomatic relationships with Japan, India, China, and South Korea drive long-term LNG supply contracts. These agreements minimize trade barriers, ensure stable revenue for producers, and position Australian gas as a reliable, clean-burning energy source for Asia's coal-to-gas energy transition.

- Infrastructure Upgrades: Investments in pipelines, LNG export terminals, and gas processing facilities enhance supply chain efficiency and alleviate transportation constraints. Enhanced infrastructure improves delivery reliability to both domestic and international markets, attracting further capital investment by improving operational scalability and production yield.

- Rising Energy Demand from Asia: Asia's rapid industrialization and decarbonization transition from coal to cleaner natural gas create sustained demand growth for Australian LNG exports. Increasing electrification, industrial gas use, and government-mandated emissions reductions across major Asian economies underpin long-term structural demand for Australian gas supply.

Market Restraints

- Regulatory Uncertainty: Frequent changes in environmental regulations, exploration permits, and emissions policy create unpredictability for long-lead capital projects. Misalignment between federal and state regulatory frameworks adds complexity, increasing development timelines and deterring both domestic and international investment in new Australian projects.

- Environmental Opposition: Significant public and Indigenous community resistance to fossil fuel projects creates legal delays, protests, and regulatory reviews that impede development. Offshore drilling and fracking operations face intense scrutiny, raising project costs, extending approval timelines, and increasing reputational risk for operators across Australia.

- High Operational Costs: Australian oil and gas operations rank among the world's highest cost, driven by remote geography, specialized offshore technology requirements, and elevated labour costs. These structural cost disadvantages relative to Middle Eastern and US producers constrain profit margins and reduce competitiveness in volatile global commodity markets.

Market Opportunities

- Hydrogen Production: Australia is strategically positioned to become a major hydrogen exporter, leveraging existing gas infrastructure and abundant renewable energy. Both green hydrogen and blue hydrogen from natural gas with carbon capture present viable commercial pathways, with proximity to decarbonization-focused Asian markets providing a natural demand base.

- Carbon Capture and Storage: Australia's depleted gas fields and geological formations provide suitable CO₂ storage sites, enabling operators to continue fossil fuel production while meeting emissions obligations. Government funding and industry partnerships are advancing CCS commercially, enhancing Australia's competitiveness in carbon-constrained global markets.

Market Challenges

- Regulatory Uncertainty and Permitting Delays: Evolving environmental legislation and protracted approval processes for new exploration projects create significant investment uncertainty. These delays extend timelines, increase financing costs, and deter capital allocation from international investors requiring policy stability for long-lead energy projects.

- Intensifying Global LNG Competition: Emergence of new LNG supply from the United States, Qatar, and East Africa is increasing competition for long-term Asian supply contracts. Australian producers face structural cost disadvantages, necessitating technology adoption and operational efficiency improvements to retain contract positions against new low-cost suppliers.

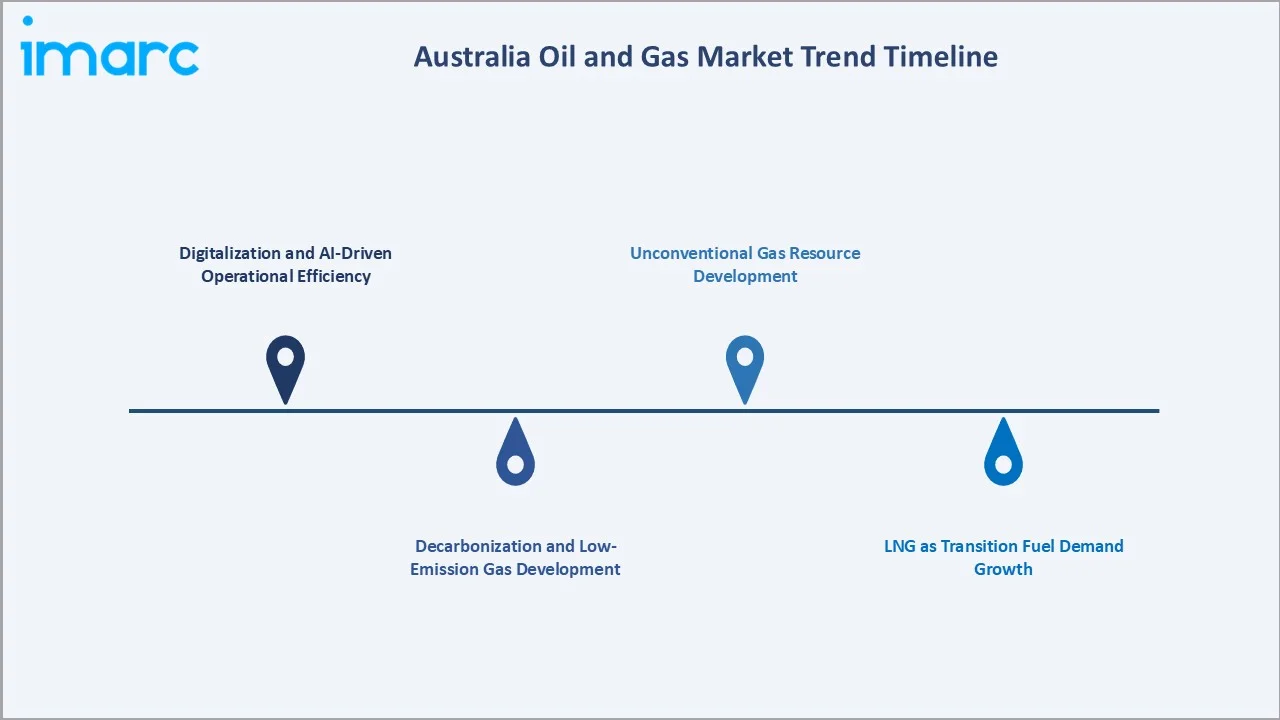

Emerging Market Trends

1. Digitalization and AI-Driven Operational Efficiency

Artificial intelligence, IoT sensors, and predictive analytics are transforming upstream exploration accuracy and production optimization. Operators deploy AI-enabled predictive maintenance systems that reduce downtime, lower operating costs, and improve safety outcomes across offshore platforms and remote onshore facilities throughout Australia.

2. Decarbonization and Low-Emission Gas Development

Australian gas producers are investing in low-emission production methods, carbon offset programs, and CCS technology integration to satisfy increasingly stringent carbon credential requirements from Asian LNG buyers. This trend reshapes project economics and drives collaboration between energy majors and government-backed clean energy research institutions.

3. LNG as Transition Fuel Demand Growth

Natural gas's role as a transition fuel in Asia's coal-to-clean energy pivot is sustaining long-term LNG demand well beyond 2030. Australia's established export infrastructure and trusted supply relationships with major Asian utilities provide a structural competitive advantage as Asia's transition from coal accelerates through the forecast decade.

4. Unconventional Gas Resource Development

Shale and tight gas development in the Beetaloo and Canning basins is gaining momentum as conventional field maturation creates supply gaps. Advances in horizontal drilling and hydraulic fracturing technology are improving economic viability, offering a pathway to extend Australia's gas production horizon and reinforce domestic energy security through 2034.

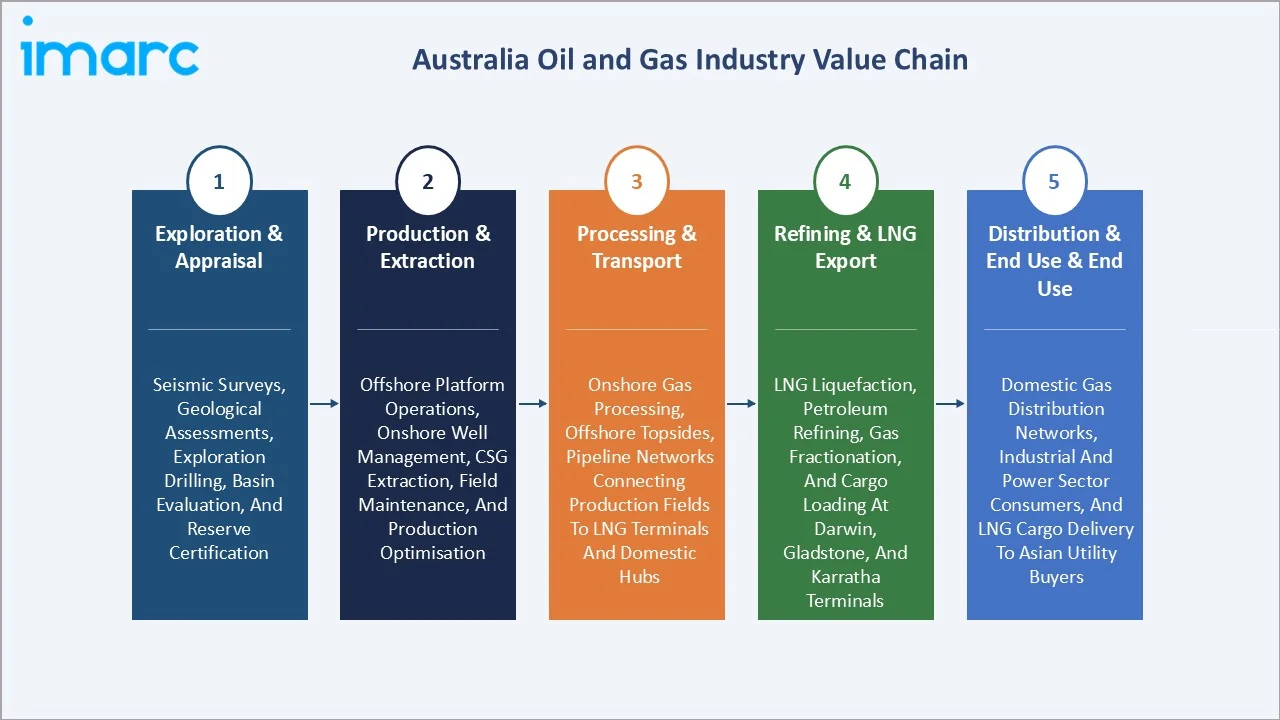

Industry Value Chain Analysis

The Australia oil and gas value chain spans five integrated stages from exploration through end-use distribution. Upstream exploration and production capture the primary resource value, while LNG export terminals and downstream refining create high-value products that command premium pricing in international energy markets.

|

Stage |

Key Activities |

|

Exploration & Appraisal |

Seismic surveys, geological assessments, exploration drilling, basin evaluation, and reserve certification |

|

Production & Extraction |

Offshore platform operations, onshore well management, CSG extraction, field maintenance, and production optimisation |

|

Processing & Transport |

Onshore gas processing, offshore topsides, pipeline networks connecting production fields to LNG terminals and domestic hubs |

|

Refining & LNG Export |

LNG liquefaction, petroleum refining, gas fractionation, and cargo loading at Darwin, Gladstone, and Karratha terminals |

|

Distribution & End Use |

Domestic gas distribution networks, industrial and power sector consumers, and LNG cargo delivery to Asian utility buyers |

Upstream stages, exploration, drilling, and production, capture the highest intrinsic resource value and attract the largest share of capital expenditure across Australia's oil and gas sector. Midstream pipeline transport and LNG liquefaction represent critical value-enabling infrastructure that connects remote production fields to export terminals and domestic distribution networks. These stages command a significant margin through processing fees, tariffs, and long-term capacity agreements with upstream producers and downstream buyers.

Technology Landscape in the Australia Oil and Gas Industry

AI-Powered Exploration and Drilling Optimization

Machine learning algorithms are processing vast seismic datasets to improve subsurface reservoir characterization and reduce exploration risk. AI-driven drilling optimization tools enhance bit performance and reduce non-productive time, lowering well costs and improving drilling precision in complex offshore geological formations across Australian basins.

Floating LNG and Offshore Processing Technology

Shell's Prelude FLNG facility demonstrated the commercial viability of floating LNG technology, enabling monetization of remote gas fields previously inaccessible by pipeline. This technology unlocks significant stranded gas in Australia's offshore basins, offering a cost-competitive alternative to onshore LNG facility construction for isolated accumulations.

Carbon Capture, Utilization, and Storage Technology

Gorgon CCS, one of the world's largest carbon capture projects, injects CO₂ into subsurface formations beneath Barrow Island. Advances in CCS monitoring, injection technology, and geological storage verification are improving reliability and reducing costs, making CCS a commercially viable emissions reduction pathway for Australian LNG producers globally.

Digital Twin and Predictive Maintenance Platforms

Operators are deploying digital twin platforms creating real-time virtual replicas of offshore platforms and processing facilities. These systems enable predictive maintenance scheduling, remote operational monitoring, and emergency response planning, significantly reducing unplanned downtime and improving safety across geographically dispersed offshore assets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Upstream |

50.0% |

2025 |

|

Application |

Offshore |

60.0% |

2025 |

|

Region |

Western Australia |

40.0% |

2025 |

By Type

Upstream commands a 50.0% majority share in 2025 owing to Australia's role as a leading LNG exporter with extensive deepwater exploration activity. The Carnarvon, Browse, and Bonaparte basins support multi-decade production commitments with major Asian buyers, sustaining capital investment in exploration, appraisal, and production optimization.

To access detailed market analysis, Request Sample

Downstream (30.0%) captures value from LNG liquefaction, petroleum refining, and petrochemical production. Midstream (20.0%) encompasses pipeline networks and processing plants linking upstream production to domestic consumers and LNG export terminals, representing a critical but capital-intensive enabling infrastructure segment across Australia.

By Application

Offshore dominates at 60.0% in 2025, driven by world-class deepwater LNG projects including Gorgon, Wheatstone, Ichthys, Prelude, and the developing Scarborough project. Offshore production benefits from large reservoir sizes, long plateau production periods, and established LNG export infrastructure supporting high-volume, long-term supply commitments to Asia.

Onshore (40.0%) encompasses Queensland's coal seam gas fields feeding the Gladstone LNG complex, Cooper Basin conventional gas production supplying the eastern domestic gas market, and emerging Northern Territory unconventional gas resources in the Beetaloo Basin representing a significant future supply growth opportunity for domestic and export markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Western Australia |

40.0% |

Concentration of offshore LNG projects; world-scale Gorgon, Wheatstone, and Scarborough developments; major operator headquarters |

|

Queensland |

25.0% |

Coal seam gas and LNG exports from the Gladstone complex; long-term Asian supply contracts from APLNG, QCLNG, and GLNG projects |

|

Northern Territory & Southern Australia |

15.0% |

Ichthys LNG project; Beetaloo Basin unconventional gas potential; Cooper Basin conventional gas production |

|

ACT & New South Wales |

12.0% |

Domestic gas demand from industrial and power sectors; pipeline gas imports from Queensland and South Australia |

|

Victoria & Tasmania |

8.0% |

Offshore Otway and Bass Strait gas production; domestic supply for southeastern industrial and residential consumers |

Queensland, at 25.0% in 2025, is underpinned by three world-scale LNG trains at Gladstone that collectively process coal seam gas from the Surat and Bowen basins. The state's CSG-to-LNG model pioneered a globally replicated supply chain integration approach, generating substantial long-term contract revenue from Asian utility buyers seeking reliable alternative supply sources.

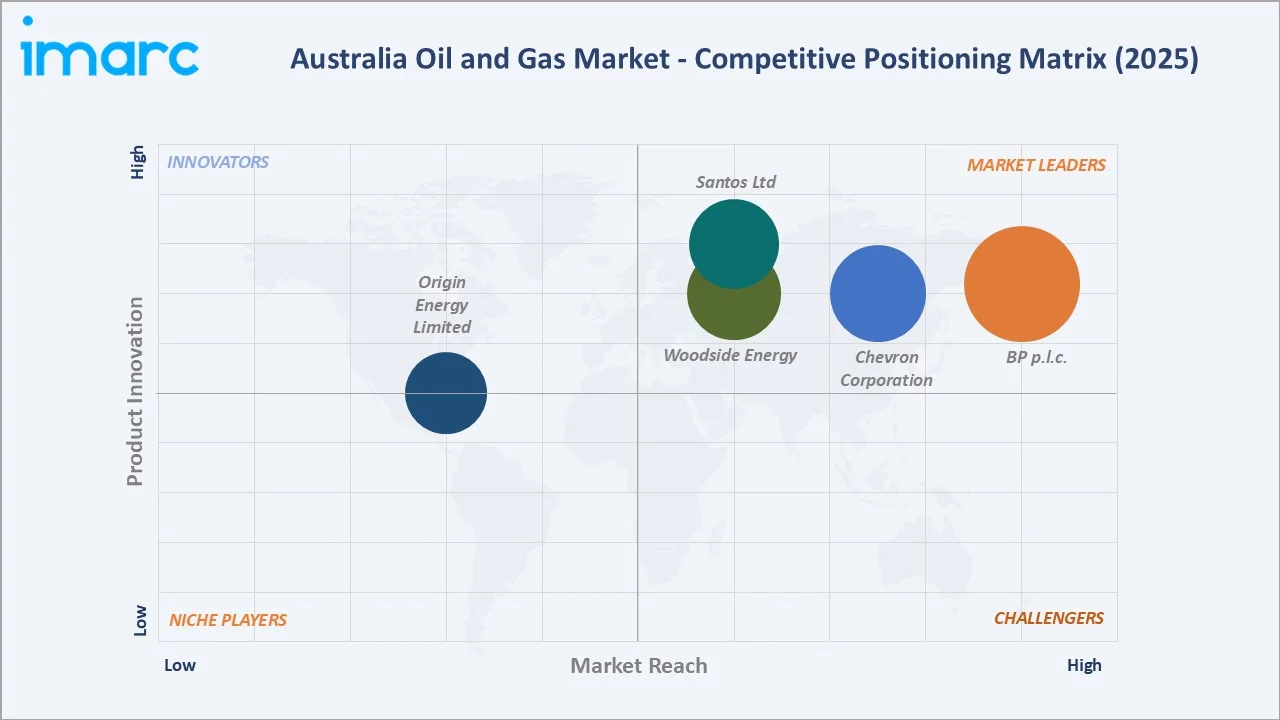

Competitive Landscape

The Australia oil and gas market is moderately concentrated at the operator level, with global energy majors and domestic independent producers collectively commanding the largest market shares. International majors leverage technical expertise, balance sheet depth, and Asian buyer relationships, while domestic independents focus on niche basin positions and production optimization to maintain competitive unit economics in this high-cost environment.

|

Company Name |

Key Products / Operations |

Market Position |

Global Strategic Focus |

|

BP p.l.c. |

Upstream oil and gas |

Leader |

Transitioning toward low-carbon energy, maintaining Australian gas production while expanding renewable investment |

|

Chevron Corporation |

Oil and Natural gas |

Leader |

Major LNG exporter to Asia; deploying CCS at Gorgon; expanding low-carbon energy transition strategy |

|

Origin Energy Limited |

LNG |

Established |

Integrated energy company; leveraging APLNG production; expanding renewable energy portfolio |

|

Santos Ltd |

Upstream Gas and Liquids, LNG |

Leader |

Major pan-Asian LNG supplier; growing through Dorado oil and Barossa gas developments |

|

Woodside Energy |

Oil and gas, LNG |

Leader |

Australia's largest dedicated oil and gas company, advancing Scarborough, building hydrogen export capability |

Key players include BP p.l.c., Chevron Corporation, Origin Energy Limited, Santos Ltd, and Woodside Energy, among others.

Key Company Profiles

Woodside Energy

Woodside Energy is Australia's largest independent oil and gas company, operating a diversified LNG asset portfolio. The company is expanding internationally and investing in hydrogen production to extend its growth horizon and position itself as a future clean energy exporter.

- Product Portfolio: Oil and gas, LNG

- Strategic Focus: Woodside is executing a dual strategy of maximizing production from established LNG assets while advancing the Scarborough project as its next major growth platform, concurrently building hydrogen export capability targeting decarbonization-focused Asian buyers seeking alternative low-emission fuels to complement conventional LNG supply.

Santos Ltd

Santos Ltd is a leading pan-Asian LNG, growing through the Dorado oil development and Barossa gas project, both representing significant near-term production additions to its established LNG portfolio serving long-term contracted Asian customers.

- Product Portfolio: Upstream Gas and Liquids, LNG

- Strategic Focus: Santos is executing a portfolio expansion strategy through Barossa and Dorado development while maintaining disciplined capital allocation to existing LNG assets. The company is advancing CCS integration at Darwin LNG and exploring carbon-neutral LNG credentials to meet evolving Asian buyer requirements for lower-emission gas supply.

Chevron Corporation

Chevron Corporation operates Australia's largest LNG projects in Western Australia, collectively representing its single largest international capital investment. Chevron's Australian portfolio is a cornerstone of its upstream strategy, supplying long-term contracted LNG volumes to major Asian utilities under multi-decade supply agreements.

- Product Portfolio: Oil and Natural Gas

- Strategic Focus: Chevron's Australian strategy centers on maximizing production reliability at Gorgon and Wheatstone while advancing CCS technology to reduce emissions intensity, and selectively investing in exploration acreage adjacent to existing infrastructure to support future backfill opportunities that extend LNG train utilization over the long term.

Market Concentration Analysis

The Australia oil and gas market is moderately concentrated at the project level, with a small number of large LNG projects accounting for the majority of production value. Woodside Energy, Santos, and Chevron collectively operate the country's largest LNG production capacity, though joint venture structures distribute equity broadly among global majors and financial investors with long-term contracted revenue streams.

At the basin level, Western Australian offshore resources dominate concentration metrics, reflecting the scale differential between Carnarvon Basin world-class LNG projects and smaller-scale onshore and southeastern Australian conventional gas production. This geographic concentration creates supply chain dependencies that both operators and regulators are actively managing through infrastructure diversity and interconnection initiatives across Australia.

Investment & Growth Opportunities

Fastest-Growing Segments

Offshore applications represent the highest-growth segment through 2034 at approximately 6.80% CAGR, capturing investment in Scarborough, Barossa, and Browse Basin development. Upstream benefits from new exploration commitments and greenfield LNG investments that extend Australia's production horizon well beyond existing project plateau periods.

Emerging Markets

Queensland and the Northern Territory are emerging as significant investment frontiers. Beetaloo Basin unconventional gas represents a potentially transformative new supply source, while Queensland's CSG fields continue to attract capital for production optimisation and reserve extension drilling supporting the Gladstone LNG complex feedstock supply requirements.

Venture & Investment Trends

Global energy majors and private equity are increasing capital allocation to Australian hydrogen and CCS projects, reflecting the strategic value of existing gas infrastructure for new energy transition applications. Government co-investment through CCS and Hydrogen Headstart programs is catalyzing private capital mobilization across low-emission technology projects.

Future Market Outlook (2026-2034)

The Australia oil and gas market is forecast to expand from USD 432.1 Million in 2025 to USD 736.8 Million by 2034 at a CAGR of 5.93%, driven by Asia's sustained gas demand, new offshore LNG project commissioning, and Australia's strategic positioning as a reliable long-term supplier to the world's fastest-growing energy markets.

Three structural forces will shape the market through 2034: new offshore developments—principally Scarborough and Barossa—will expand production capacity and extend contracted LNG supply; decarbonization integration through CCS and hydrogen will redefine the revenue mix; and digital transformation will compress operating costs, improving economics for all operators.

Research Methodology

Primary Research

Primary research encompassed structured interviews with upstream operators, LNG terminal managers, pipeline infrastructure owners, government energy policymakers, and Asian LNG buyer representatives. Primary data validated market sizing, segment shares, regional demand estimates, and evolving operational cost and investment trends in the Australian oil and gas market.

Secondary Research

Key secondary sources include Australian Department of Industry, Science and Resources energy statistics, Geoscience Australia resource assessments, NOPSEMA regulatory data, IEA natural gas market reports, Wood Mackenzie upstream analytics, annual reports from key operators, and APPEA industry association publications on Australian oil and gas production and investment.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models incorporating Australian GDP growth rates, Asian LNG demand projections, operator capital expenditure guidance, and commodity price scenario analysis. Scenario modelling encompassed base, optimistic, and conservative cases through the 2034 horizon.

Australia Oil and Gas Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Upstream, Midstream, Downstream |

| Applications Covered | Offshore, Onshore |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | BP p.l.c., Chevron Corporation, Origin Energy Limited, Santos Ltd, Woodside Energy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia oil and gas market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia oil and gas market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia oil and gas industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Oil and Gas Market Report

The Australia oil and gas market reached USD 432.1 Million in 2025, reflecting sustained demand driven by LNG export growth, recovering upstream investment post-pandemic, and strong Asian energy demand underpinning long-term contracted supply agreements from Australian LNG producers.

The market is projected to reach USD 736.8 Million by 2034, growing at a CAGR of 5.93% during 2026-2034, driven by new offshore LNG commissioning, rising Asian energy demand, infrastructure expansion, and Australia's sustained competitive position as a major global LNG exporter.

Upstream leads with a 50.0% market share in 2025, driven by Australia's large-scale offshore LNG production. Downstream (30.0%) is the second largest, capturing LNG liquefaction and petroleum refining value, while Midstream (20.0%) encompasses pipeline and processing infrastructure.

Offshore dominates with a 60.0% share in 2025, underpinned by world-scale LNG projects in the Carnarvon, Browse, and Bonaparte basins. Onshore (40.0%) is driven by Queensland CSG-to-LNG and Cooper Basin conventional gas production serving domestic and export markets.

Western Australia leads with a 40.0% market share in 2025, underpinned by the Gorgon, Wheatstone, and North West Shelf LNG projects. Queensland follows at 25.0%, driven by the Gladstone LNG complex and coal seam gas production from the Surat and Bowen basins.

Offshore applications represent the fastest-growing segment at approximately 6.80% CAGR through 2034, driven by Scarborough and Barossa developments. Upstream is the fastest-growing type at approximately 6.20% CAGR, supported by exploration investment and new field commissioning.

Leading companies include BP p.l.c., Chevron Corporation, Origin Energy Limited, Santos Ltd, and Woodside Energy, among others.

Key drivers include LNG expansion initiatives responding to Asian energy demand, regional trade agreements securing long-term supply contracts, infrastructure upgrades improving supply chain efficiency, and rising Asian energy demand from economies transitioning from coal to cleaner gas.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)