Australia Data Center Power Market Size, Share, Trends and Forecast by Component, Size, Vertical, and Region 2026-2034

Australia Data Center Power Market Size & Forecast 2026-2034

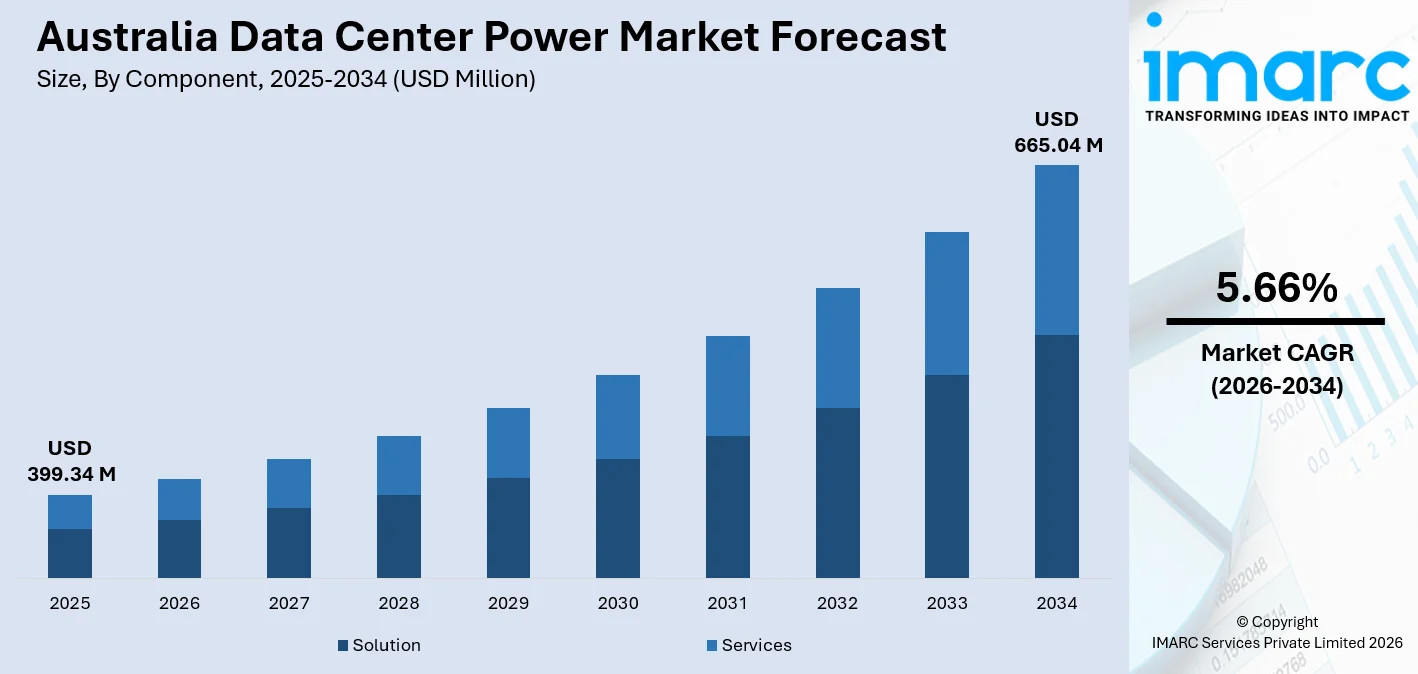

The Australia data center power market was valued at USD 399.34 Million in 2025 and is expected to reach USD 665.04 Million in 2034, growing at a CAGR of 5.66% during the forecast period of 2026-2034. The strategic position of Australia as a Southeast Asian digital hub, backed by the need for sovereign data and the increasing pace of digitalisation in the country, will ensure healthy expenditure on the infrastructure side. The ongoing growth in the number of data center spaces will add strength to the Australia data center power market share.

To get more information on this market Request Sample

Australia Data Center Power Industry Analysis: Key Insights

- Solution commands a 32% share by component in 2025 - purpose-built power management software and intelligent UPS systems are becoming structural requirements as operators optimize energy efficiency and minimize downtime risk across hyperscale and colocation environments.

- Enterprise data centers own 41% of capacity by size by 2025 - large-scale proprietary deployments driven by financial services, government agencies, and technology firms prioritize on-premises control, compliance, and high-availability power architecture over shared infrastructure.

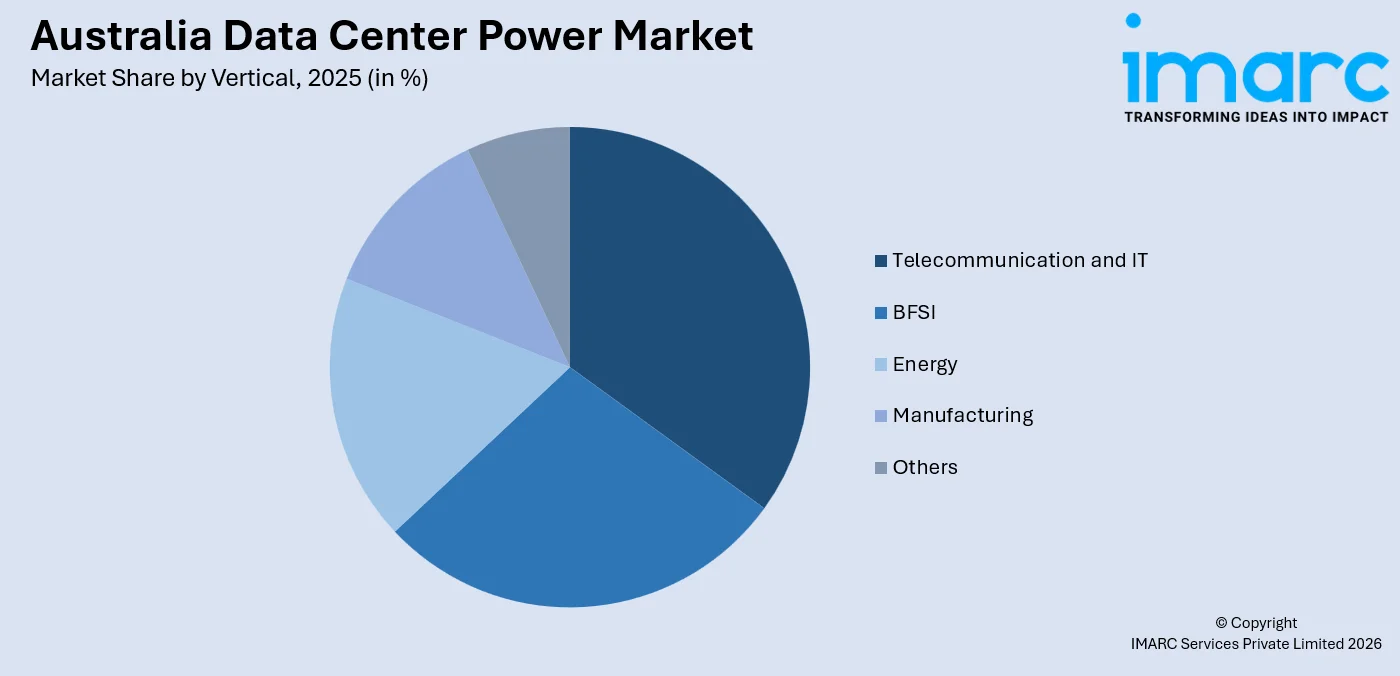

- Telecommunication and IT leads verticals at 30% in 2025 - Australia’s accelerating 5G rollout and cloud-native service delivery are compelling telcos and IT firms to dramatically scale up power infrastructure investment across metropolitan and regional deployments.

- New South Wales & ACT holds a 38% regional share in 2025 -Sydney’s status as Australia’s financial and technology capital, paired with the ACT’s government data concentration, anchors the highest density of data center power consumption in the country.

Australia Data Center Power Trends and Dynamic 2026

Market Trends

AI and hyperscale expansion fuelling unprecedented power demand

The data center industry in Australia is undergoing a revolution in its landscape due to the adoption of AI workloads and the entry of hyperscalers in the country. In March 2025, Microsoft announced its plan to invest AUD 5 billion in Australian data center infrastructure, focusing on Sydney and Melbourne campuses for Azure-based AI workloads and enterprise cloud services. This increase in compute resource deployments is having a direct impact on the demand for high-density power distribution and UPS systems.

Renewable energy integration reshaping power supply strategies

A significant change in the adoption of renewable energy sources is revolutionizing the Australia data center power market trends. This change in the power landscape is being driven by ESG initiatives from corporations and the Australian government’s push for net-zero emissions targets. The government’s plans to add 3.2GW of renewable energy and 1.9GW of battery storage capacity by 2035 to service the data centre load will limit price increases and offset the extra emissions.

Liquid cooling and advanced thermal management gaining traction

The rapid densification of server racks, especially in AI-optimized facilities, is making traditional air cooling impractical. This is heightening the need for combined power and cooling solutions rather than UPS and PDU systems.

- Edge Computing Proliferation: The proliferation of micro-data centres in regional Australia beyond capital cities is creating incremental demand for scalable power management solutions.

- Sovereign Data Localisation: Australian government mandates for domestic data processing are driving local data centre buildouts at a rapid pace, creating a need for power infrastructure.

- High-Density Power Distribution: The growing need for GPU computing in artificial intelligence clusters is increasing rack power density, creating a need for high-density PDUs.

- Modular UPS Adoption: Data centres in Australia are adopting modular UPS systems for scalability without downtime, reducing operational expenditure.

Growth Drivers

Hyperscaler capital expenditure driving infrastructure buildout

Global hyperscalers are committing unprecedented capital to Australian data center infrastructure, directly driving demand for power systems. In June 2025, Amazon Web Services announced a USD 12.97 billion investment in expand, operate and maintain its data center infrastructure in Australia from 2025 to 2029, including dedicated power upgrade programs for its Sydney region to accommodate growing AI and enterprise workload requirements across AWS campuses.

Government digital transformation and regulatory requirements

The federal government digital transformation initiative is one of the major growth catalysts for the Australia data center power market. In December 2025, the Digital Transformation Agency released a new Cloud Policy to set a clear direction for cloud adoption in the APS. The policy builds on a stronger foundation for secure, modern, and high-performing digital services and supports the use of new technologies in a responsible way. The policy will commence on 1 July 2026. This policy-driven requirement is concentrating demand for government-grade, high-availability power infrastructure at accredited facilities, particularly in Canberra.

Financial services compliance and enterprise digitisation

The financial services sector in Australia is one of the consistent growth drivers for data center power consumption in the country. The Australian Prudential Regulation Authority updated its CPS 234 cybersecurity standard, which requires all regulated financial institutions in the nation to have enhanced redundancy and backup power capabilities. This has resulted in significant investments in UPS upgrades and backup generators for data centers in banking and insurance sectors in the country.

- 5G Rollout and Telecom Infrastructure Development: Australia’s rollout of a nationwide 5G network by telcos is increasing demand for colocation data center power infrastructure at both metropolitan and rural tower infrastructure sites.

- Colocation Market Development: Increased demand for managed colocation services from enterprises is fueling capacity development in third-party data centers, thereby directly increasing colocation data center power infrastructure demand.

- Edge AI and IoT Deployments: Manufacturing, mining, and utilities sectors deploying Edge AI and IoT analytics solutions are fueling demand for distributed data center power infrastructure, excluding traditional enterprise data center deployments.

- Energy Efficiency and PUE Optimisation: Sustainability and regulatory drivers are increasing demand for energy efficiency solutions, such as smart PDUs, DCIM, and flywheel UPS systems.

Market Restraints

Electricity grid constraints and infrastructure limitations: The current aging electricity grid infrastructure in metropolitan markets in Australia presents capacity limitations for the connection of data center power requirements. Inadequate upgrades and long connection lead times with utilities can create significant project delivery and expansion timelines in critical markets.

High capital and operational expenditure requirements: The high capital expenditure requirements for the development of end-to-end power infrastructure solutions, including UPS systems, backup generators, and redundant utility connections, create significant barriers for mid-market data center operators looking to expand capacity in competitive metropolitan markets.

Environmental regulatory and planning approval complexities: Increasing regulatory and public concerns related to the environmental impacts of data center operations, including water usage for cooling and land use intensity, can create operational limitations for data center facilities. Complexities in planning approvals can create significant project delivery and expansion timelines for data center facilities.

Australia Data Center Power Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Solution | 32% | 2025 |

| Size | Enterprise Data Center | 41% | 2025 |

| Vertical | Telecommunication and IT | 30% | 2025 |

| Region | New South Wales & ACT | 38% | 2025 |

Component Insights

Solution- 32% Market Share (2025) | Leading Component

The solution segment, encompassing power monitoring software, DCIM platforms, and intelligent power management systems, leads the market with a 32% component share. In July 2025, Schneider Electric Australia launched its EcoStruxure IT platform for the local enterprise market, adopted by three major Sydney colocation operators to deliver real-time power analytics and capacity optimisation across high-density rack environments.

|

Segment Breakdown Solution (32%) · Services |

Size Insights

Enterprise Data Center- 41% Market Share (2025) | Leading Size

Enterprise data centers, managed by financial organizations, government entities, and leading technology companies, hold the highest share of data center capacity at 41%. In March 2026, Goodman Group, a global leading provider of essential services, today marked the official commencement of construction at Goodman’s SYD01 data centre in Artarmon, in northern Sydney’s business district. The 90MW data centre is part of several data centre projects Goodman is starting around the world as it continues to deliver its $18 billion global development program.

|

Segment Breakdown Enterprise Data Center (41%) · Mid-size Data Center · Large Data Center |

Vertical Insights

Access the comprehensive market breakdown Request Sample

Telecommunication and IT- 30% Market Share (2025) | Leading Vertical

The telecommunication and IT sector takes the lead in terms of data center capacity share at 30%, driven by Australia’s growing 5G network infrastructure and associated requirements for cloud-native services. Telstra International, the global division of telecommunications and technology company Telstra, has achieved significant advancements in the performance and flexibility of its Asia Pacific submarine cable and backhaul network with incremental 200Tbs, marking a 30 percent increase in total network capacity in key Asia Pacific routes.

|

Segment Breakdown Telecommunication and IT (30%) · BFSI · Energy · Manufacturing · Others |

Regional Insights

New South Wales & ACT- 38% market share (2025) | Leading Region

New South Wales and the Australian Capital Territory jointly anchor the market at 38%, driven by Sydney’s concentration of hyperscaler campuses and the ACT’s significant government data processing infrastructure. Sydney’s western corridor has emerged as a dedicated data centre precinct, with multiple operators securing development approvals for high-capacity facilities requiring intensive power infrastructure. The ACT government’s whole-of-government cloud strategy has further concentrated federal agency data workloads in Canberra, creating a stable, policy-driven demand base for resilient power systems and redundant utility connections.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

38%

|

|

Key States

|

Sydney, Canberra, Newcastle |

|

Major Growth Drivers

|

Hyperscaler investment, Government digitalisation, Financial services expansion |

|

Outlook

|

Australia’s dominant data center power hub |

|

Regional Breakdown New South Wales & ACT (38%) · Victoria & Tasmania · Queensland · Western Australia · Northern Territory & Southern Australia |

Victoria:

Victoria represents the second-largest data center power segment, anchored by Melbourne’s growing status as a financial technology and cloud services hub. In January 2026, Australia-based data center operator NextDC has received development approval from the state of Victoria for its 150-megawatt digital infrastructure campus in Melbourne at an investment cost of A$2 billion ($1.3 billion).

|

Metric

|

Details

|

|---|---|

|

Key States

|

Melbourne, Geelong, Bendigo |

|

Major Growth Drivers

|

Fintech expansion, Cloud service adoption, Manufacturing digitalisation |

|

Outlook

|

Strong secondary market with continued investment |

Queensland:

Queensland's data center power market is boosted by the Queensland Government's "Queensland Data Centre Strategy," which outlines the government's approach to workload consolidation in purpose-built data centers.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Brisbane, Gold Coast, Townsville |

|

Major Growth Drivers

|

Government digital services, Tourism technology, Resources sector digitisation |

|

Outlook

|

Growing investment in government and commercial facilities |

Western Australia:

Western Australia’s data center power requirements are increasingly driven by the resources sector’s adoption of cloud-based operational technology platforms and real-time analytics.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Perth, Kalgoorlie, Karratha |

|

Major Growth Drivers

|

Mining technology digitisation, Energy sector modernisation, Government cloud services |

|

Outlook

|

Resource-driven growth with stable demand pipeline |

South Australia and Northern Territory:

South Australia and the Northern Territory represent an emerging data center power segment supported by renewable energy abundance and government cloud migration priorities. The South Australia is focusing on data facility upgrades and power resilience improvements in Adelaide and remote data infrastructure supporting the Northern Territory.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Adelaide, Darwin, Alice Springs |

|

Major Growth Drivers

|

Renewable energy integration, Government digital migration, Defence sector requirements |

|

Outlook

|

Emerging market with renewable energy advantage |

Market Outlook 2026-2034

What is the future outlook of the Australia data center power market?

The Australia data center power market is expected to sustain steady revenue growth through 2034.

The outlook for Australia data center power market is extremely positive due to compounded growth in infrastructure for Artificial Intelligence solutions, data localisation policies from governments, and a growing rate of digitalisation in key industries. Further adoption of high-density data center power solutions, modular UPS solutions, and renewable energy-powered data center solutions will continue to fuel growth in this market. Regulatory policies from energy efficiency regulations and hyperscaler investment commitments will continue to fuel data center spend in this market through 2034.

Australia Data Center Power Market: Leading Key Players

The data center market in Australia has a competitive set of global technology conglomerates and data center power infrastructure providers competing in this space on aspects such as energy efficiency, services presence, and strategic partnerships with hyperscalers. The key players compete on aspects such as integrated power management solutions, strategic hyperscaler partnerships, and services presence to capitalize on growing demand in this space.

| Company | Leading Brands | Highlights |

|---|---|---|

| Schneider Electric | APC, EcoStruxure | Leading integrated power management provider; Galaxy VX modular UPS adopted by financial services data centres across New South Wales and Victoria in 2025 |

| Eaton Corporation | 9PX UPS, PowerChain | Modular lithium-ion UPS solutions for enterprise and government sectors; PowerChain platform deployed at government data facilities in Canberra and Brisbane |

| Vertiv Group | Liebert, Geist | Advanced cooling-integrated power infrastructure; expanded Australian technical service hub in Melbourne |

Major players in the Australia data center power market include ABB Ltd, Legrand, and Siemens AG.

Latest Development & News

- In March 2026, Biotech start-up Cortical Labs, which is based in Australia announced building two small data centers staffed by human brain cells, putting lab-grown neurons on silicon chips in a project that one day may compete with the likes of Nvidia Corp. chips.

- In March 2026, Cloud Carrier plans to use gas-fired engines to run their data centers, generating enough energy to power 70,000 homes. Experts are worried about the consequences of a large-scale rollout of similar-sized data centers on greenhouse gas emissions.

- In January 2026, Eaton is partnering with Flexnode, an innovative digital infrastructure company, to provide scalable rack and power infrastructure solutions for data center compute applications. Eaton is providing critical power backup, rack, and cable management solutions for Flexnode’s modules, which can reduce deployment time in data centers by up to 35%.

Australia Data Center Power Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Sizes Covered | Mid-Size Data Center, Enterprise Data Center, Large Data Center |

| Verticals Covered | BFSI, Telecommunication and IT, Energy, Manufacturing, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia data center power market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia data center power market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia data center power industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Data Center Power Market Report

The Australia data center power market was valued at USD 399.34 Million in 2025.

The Australia data Center Power market is anticipated to reach a value of USD 665.04 Million by 2034.

Solution dominates the market with a share of 32%, driven by growing operator demand for power monitoring software, DCIM platforms, and intelligent UPS management systems that optimize energy efficiency and ensure uptime compliance across hyperscale and colocation facilities.

Enterprise data center commands the market with a share of 41%, driven by financial institutions, government agencies, and large technology firms maintaining dedicated on-premise data processing facilities with stringent uptime and compliance requirements for mission-critical workload management.

Some of the major players in the Australia data center power market include Schneider Electric, Eaton Corporation, Vertiv Group, ABB Ltd, Legrand, Siemens AG, etc.

Australia’s data center power sector is witnessing accelerating adoption of lithium-ion battery-based UPS systems, replacing legacy VRLA batteries for superior cycle life and energy density. AI-driven predictive power management platforms are enabling dynamic capacity allocation and real-time anomaly detection, reducing unplanned downtime risk across mission-critical facilities.

New South Wales & ACT currently leads the Australia data center power market, accounting for a share of 38%. The region benefits from Sydney’s dense concentration of financial services data infrastructure, federal government facility requirements in Canberra, and continuous hyperscaler investment in high-capacity campus developments.

Key growth catalysts include Australia’s expanding role as a Southeast Asian internet exchange hub, proliferation of streaming and content delivery networks requiring low-latency processing, defence sector digitalisation mandates, autonomous vehicle testing requiring edge compute power infrastructure, and continued enterprise cloud migration across all industry verticals.

Key challenges include critical skills shortages in qualified data center power engineers and electricians, cybersecurity vulnerabilities in digitally connected power management systems, supply chain constraints affecting delivery lead times for switchgear and UPS components, and evolving state-level planning regulations creating approval uncertainty for new facility development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade