Australia Dairy Market Size, Share, Trends and Forecast by Product, Application, Distribution Channel, and Region, 2026-2034

Australia Dairy Market Summary:

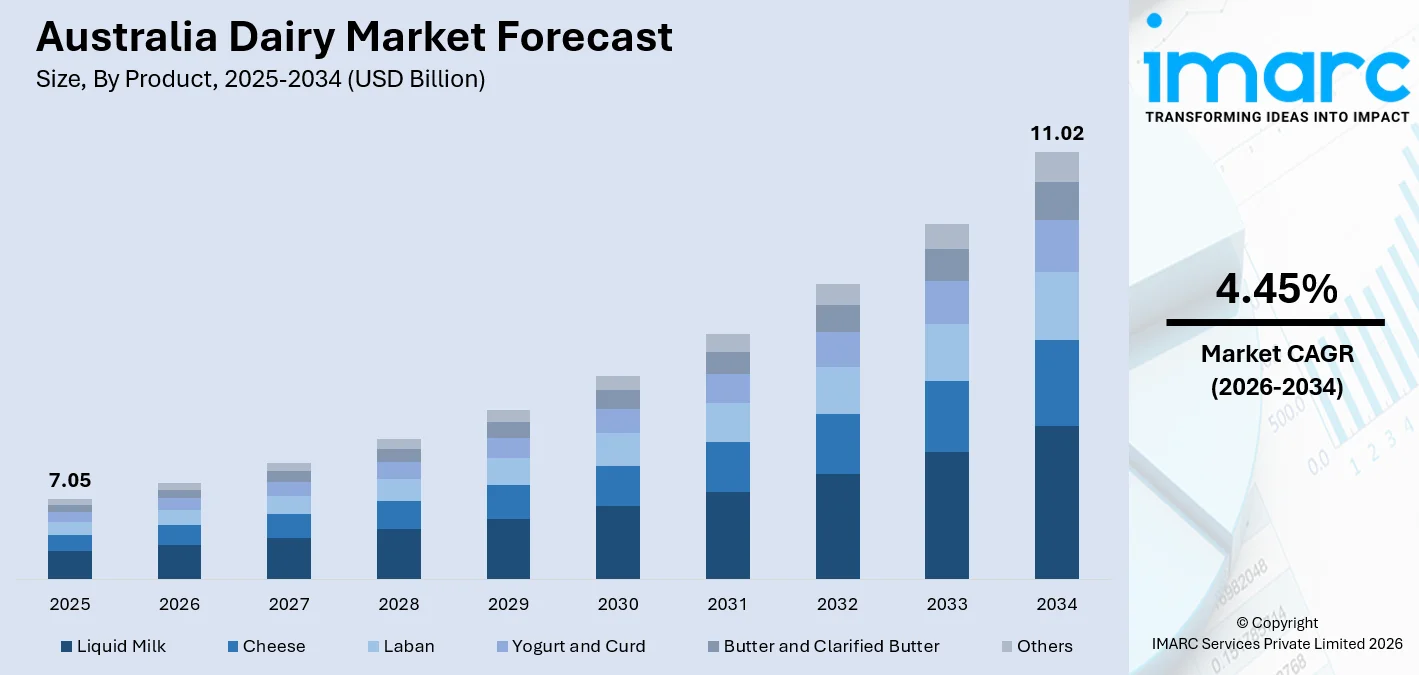

The Australia dairy market size was valued at USD 7.05 Billion in 2025 and is projected to reach USD 11.02 Billion by 2034, growing at a compound annual growth rate of 4.45% from 2026-2034.

The Australia dairy market is growing steadily and is driven by factors such as increasing health awareness among consumers, increasing demand for premium and specialty products, and increasing use of dairy farming technology. The high demand for dairy products in export markets and increasing use of dairy products in bakery products, confectionery products, and clinical nutrition also add to the growth of the Australia dairy market.

Key Takeaways and Insights:

- By Product: Liquid milk dominates the market with a share of 24.5% in 2025, owing to its status as an everyday staple consumed across all demographics and its widespread household, foodservice, and retail availability.

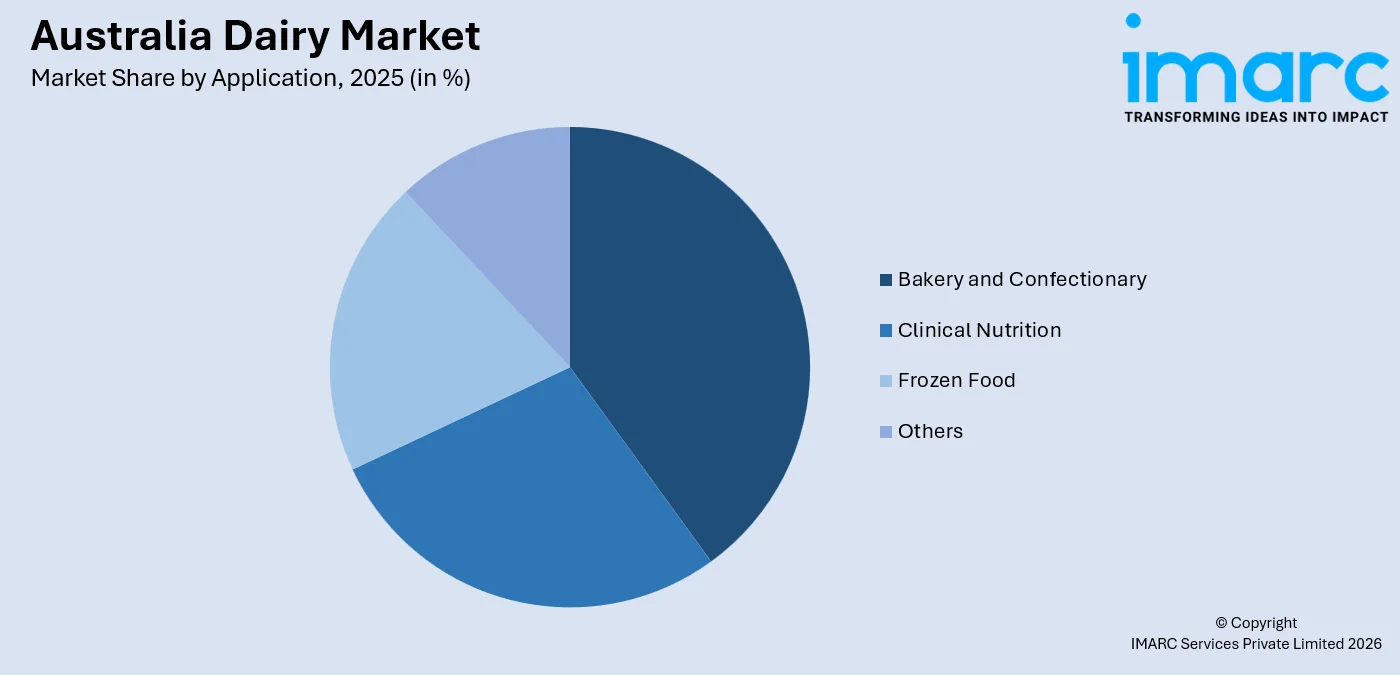

- By Application: The bakery and confectionery leads the market with a share of 32.6% in 2025, as dairy ingredients such as butter, cream, and milk powders are integral to producing premium baked goods and confections.

- By Distribution Channel: Supermarkets and hypermarkets represents the largest segment with a market share of 45.2% in 2025, as consumers rely on these one-stop retail outlets for convenient access to the full range of dairy products at competitive prices.

- By Region: Victoria & Tasmania dominates the market with a share of a 28.4% in 2025, underpinned by fertile land, favorable climate, and well-established dairy production infrastructure concentrated in southeastern Australia.

- Key Players: The Australia dairy market features a dynamic competitive landscape, with major domestic and international players focusing on product diversification, sustainable operations, and export-oriented strategies to strengthen their presence and capture evolving consumer demand.

To get more information on this market Request Sample

Australia's dairy industry occupies a central place in the nation's food and agriculture ecosystem, catering to a diverse population with wide-ranging nutritional and culinary needs. Consumer priorities have shifted substantially, with health and wellness now a primary determinant of purchasing decisions. This has prompted producers to invest in product reformulation, functional innovation, and clean-label credentials. In June 2025, Australian processor Bega Cheese reportedly sought informal clearance from the Australian Competition and Consumer Commission (ACCC) for a potential acquisition of Fonterra’s Oceania business, a move that could significantly reshape the country’s dairy processing landscape and expand Bega’s footprint across key domestic and export channels. The rise of premium and specialty dairy has opened profitable niches for large-scale processors and artisan producers alike. Growing export activity toward Asian markets reinforces Australia's position as a globally respected dairy supplier. Technology integration across the supply chain, spanning precision farming and cold-chain logistics, further enhances efficiency and broadens the Australia dairy market share.

Australia Dairy Market Trends:

Rising Demand for Premium and Specialty Dairy

Australian consumers are increasingly gravitating toward organic milk, artisanal cheeses, and probiotic-enriched yogurts, driven by a desire for indulgence and health benefits. In January 2026, The a2 Milk Company became the official dairy milk partner of the Australian Open, marking the first such partnership in the event’s history and leveraging a global platform to promote its premium, health-focused dairy products to a wide consumer base. Specialty dairies are gaining prominence as shoppers prioritize product provenance, unique flavors, and higher welfare farming credentials, reshaping the competitive dynamics of the Australia dairy market growth.

Technological Innovation Transforming Dairy Farming and Processing

Precision agriculture tools, automated milking systems, and IoT-enabled farm management platforms are transforming dairy production across Australia. In 2026, industry reporting highlighted that Australian dairy farmers are increasingly adopting automated milking systems and data-driven technologies, with robotic milking and sensor-based monitoring improving herd health tracking and operational efficiency, particularly in key regions like Victoria. Advances in pasteurization, packaging, and cold-chain logistics extend product shelf life and facilitate wider distribution. Blockchain-based traceability solutions are also gaining traction among ethically minded consumers seeking transparency in dairy sourcing and production.

Sustainability and Ethical Practices Driving Brand Differentiation

Australian dairy brands are increasingly adopting sustainable farming practices, carbon reduction measures, and eco-friendly packaging to align with evolving consumer values. In February 2026, Saputo Dairy Australia launched a biogas-to-energy project at its Allansford facility, converting wastewater into renewable energy and reducing carbon emissions by up to 14,000 tonnes annually, highlighting the sector’s growing investment in circular and low-carbon production systems. Certifications for animal welfare and transparent ingredient sourcing are influencing purchase decisions, particularly among younger demographics. Sustainability-led branding is becoming a meaningful differentiator in a competitive Australian dairy marketplace.

Market Outlook 2026-2034:

The Australia dairy market is well-positioned for steady expansion over the forecast period. Rising health consciousness will fuel demand for functional and premium dairy products, while innovations in processing and packaging create new opportunities. Export growth toward Asian markets, supported by trade agreements, will bolster revenue. Cold-chain expansion will broaden geographic access across regional and remote areas. Sustainability will remain a key competitive differentiator. The market generated a revenue of USD 7.05 Billion in 2025 and is projected to reach a revenue of USD 11.02 Billion by 2034, growing at a compound annual growth rate of 4.45% from 2026-2034.

Australia Dairy Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Liquid Milk |

24.5% |

|

Application |

Bakery and Confectionary |

32.6% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

45.2% |

|

Region |

Victoria & Tasmania |

28.4% |

Product Insights:

- Liquid Milk

- Cheese

- Laban

- Yogurt and Curd

- Butter and Clarified Butter

- Others

The liquid milk with a market share of 24.5% of the total Australia dairy market in 2025.

Liquid milk retains its top spot as the best-selling product in the Australia dairy market, as it has been a regular part of the daily diet of all age groups and demographics. It is available in fresh, long-life, organic, and A2 forms, thus appealing to a wide range of consumers. The increasing interest in lactose-free milk varieties has also helped the product maintain its top position, as more consumers are looking towards health benefits as well as convenience.

The sustained demand for liquid milk products can be attributed to the wide range of uses, from consumption as a beverage at home, in the foodservice industry, as well as industrial purposes. It remains an essential ingredient in the production of various foods, from morning beverages to meals. To meet the changing demands of consumers, companies are focusing on sustainable packaging, carbon-reduced production, as well as fortified milk products with vitamins and minerals. These developments are attracting new consumers, as well as increasing loyalty from existing consumers, thus maintaining the revenue growth of the dairy industry in Australia.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Bakery and Confectionary

- Clinical Nutrition

- Frozen Food

- Others

Bakery and confectionery leads with a share of 32.6% of the total Australia dairy market in 2025.

Bakery and confectionery is the largest application area, with dairy ingredients like butter, cream, and milk powder being used in large quantities in various bakery products, pastries, cakes, chocolates, etc. The increasing demand for premium quality bakery products and confectioneries has put additional quality demands for dairy ingredients, thus encouraging manufacturers to look for quality dairy ingredients for use in these products. The increase in café culture in urban areas in Australia has further added to the demand for quality dairy ingredients in this particular application area.

This strong performance of the bakery and confectionery segment is part of the overall premiumization trend that is influencing food consumption patterns in Australia. The need for specialty baked products is leading to the use of differentiated dairy products such as cultured butter and high-fat cream to achieve strong flavor and texture profiles. The use of plant-dairy hybrids in baking is also gaining traction as a means of serving health-conscious and flexitarian consumers without compromising on taste and quality. All of this is contributing to the strong position of the application segment in terms of its contribution to the overall revenue of the Australia dairy market.

Distribution Channel Insights:

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialist Retailers

- Online Stores

- Others

The supermarkets and hypermarkets dominates with a market share of 45.2% of the total Australia dairy market in 2025.

Supermarkets and hypermarkets serve as the primary retail destination for dairy purchases across Australia. Their ability to offer a comprehensive product range, spanning conventional, organic, lactose-free, and premium dairy options under one roof, makes them the preferred shopping environment for the majority of Australian consumers. Competitive pricing, promotional activity, and well-developed cold-chain infrastructure ensure consistent product freshness and broad accessibility, cementing their dominance across both metropolitan and regional retail markets.

The continued expansion of private label dairy within supermarket chains is further strengthening this channel's market position. Retailers are diversifying their in-house dairy ranges to include organic, specialty, and functional product tiers, reducing dependence on branded suppliers while offering consumers greater value across price points. Investment in digital grocery platforms and click-and-collect services is also enhancing the reach of supermarket dairy offerings. As large retail chains continue to refine their category management strategies, their influence over dairy product visibility, pricing, and consumer purchasing behavior is expected to remain substantial.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Victoria and Tasmania exhibits a clear dominance with a 28.4% share of the total Australia dairy market in 2025.

Victoria and Tasmania collectively hold the leading regional position, underpinned by the most concentrated and productive dairy farming landscape in Australia. Victoria's Gippsland region is particularly notable for its scale of milk, cheese, and butter production, supported by fertile pastures, a temperate climate, and sophisticated processing infrastructure. Tasmania, meanwhile, contributes premium artisanal and organic dairy products that serve both domestic niche markets and high-value export channels, adding a distinct quality dimension to the region's overall dairy output.

The region's enduring leadership reflects decades of investment in agricultural productivity, cold-chain logistics, and processing technology. Strong relationships between producers, processors, and retail partners have created a well-integrated supply chain capable of serving both domestic consumers and international buyers efficiently. Ongoing sustainability initiatives, including carbon-reduction programs and water-efficient farming practices, are reinforcing the region's long-term competitiveness. As demand for premium and traceable dairy grows domestically and across Asian export markets, Victoria and Tasmania are well-positioned to maintain and extend their pivotal contribution to the Australia dairy market.

Market Dynamics:

Growth Drivers:

Why is the Australia Dairy Market Growing?

Health-Conscious Consumer Demand Fueling Dairy Innovation

Health and wellness have become central pillars of food purchasing decisions for Australian consumers. Growing awareness of dairy's role in supporting bone strength, muscle development, and digestive health is driving sustained demand across multiple product categories. In November 2025, Bega Group expanded its portfolio of functional dairy products with the launch of high-protein Dairy Farmers smoothies and plans for gut-health yogurt ranges, reflecting strong consumer demand for protein-rich and digestive health-focused dairy options. Products rich in protein, calcium, and probiotics are gaining popularity among fitness-focused individuals and aging demographics alike. Expanding interest in functional dairy formats, including kefir, cultured drinks, and probiotic yogurts, reflects a broader lifestyle shift toward preventive nutrition, creating new market penetration opportunities for industry participants.

Export Growth and Asian Market Penetration

Australia's geographic proximity to high-growth Asian economies positions its dairy sector advantageously for export expansion. Rising incomes and growing middle-class populations in China, Japan, and Southeast Asia are generating increasing demand for high-quality and nutritious dairy products. In December 2025, Bubs Australia confirmed that the U.S. FDA would continue facilitating imports of its infant formula products beyond 2025, supporting the company’s international expansion strategy across key export markets including Asia and North America. Australia's reputation for rigorous food safety standards and premium production gives it a strong competitive edge in these markets. Free trade agreements have reduced trade barriers, while investment in value-added categories such as specialty cheese, infant formula, and functional dairy powders enables producers to meet the specific demand profiles of target markets.

Technological Innovation Enhancing Production Efficiency and Quality

Technological advancement is playing an increasingly important role in Australia's dairy sector. Precision farming technologies, including automated milking systems, sensor-based herd monitoring, and IoT-integrated feed management, are enabling farmers to optimize productivity and improve animal welfare outcomes. In February 2025, reporting by ABC News highlighted that Australian dairy farms are increasingly deploying robotic “voluntary milking systems,” allowing cows to be milked automatically while generating real-time data on herd health and milk production, reflecting a broader shift toward automation and data-driven dairy operations. Advances in pasteurization, packaging, and cold-chain logistics extend product shelf life and ensure reliable delivery across vast distances. Investments in renewable energy and water-efficient operations reduce production costs while supporting sustainability goals, collectively improving the competitiveness and efficiency of Australian dairy production across domestic and international markets.

Market Restraints:

What Challenges the Australia Dairy Market is Facing?

Climate Variability and Environmental Risks

Australia's dairy sector is acutely exposed to climate-related risks, including prolonged droughts, water scarcity, and heat stress events that diminish pasture quality and reduce milk yields. These environmental pressures elevate feed and water procurement costs, strain farm profitability, and introduce unpredictability into production planning. The increasing frequency of extreme weather events poses a persistent long-term threat to the sustainability and output consistency of dairy farming operations across major producing regions.

Intensifying Competition from Plant-Based Alternatives

The rapid growth of plant-based dairy alternatives—including oat milk, almond milk, and soy-based products—is creating competitive pressure on traditional dairy categories. Health-conscious and environmentally aware consumers are increasingly exploring non-animal options, reducing per-capita dairy consumption in some market segments. This trend demands continuous innovation from dairy producers to reinforce the nutritional superiority and taste credentials of conventional dairy while adapting product portfolios to address evolving dietary preferences.

Regulatory Compliance and Rising Input Costs

Navigating stringent food safety regulations, environmental reporting requirements, and animal welfare standards imposes considerable operational costs on dairy producers. Smaller farming operations are particularly vulnerable to these compliance burdens, which can erode margins and limit investment capacity. Rising feed, energy, and labor costs further squeeze profitability, making cost management a persistent challenge for mid-sized producers seeking to balance quality obligations with commercial viability in a competitive marketplace.

Competitive Landscape:

The Australia dairy market features a competitive landscape encompassing large-scale multinational processors, established domestic cooperatives, and a growing segment of boutique and artisanal producers. Market participants differentiate through investment in product innovation, sustainable practices, and export market development. Premium and specialty categories, including organic milk, artisanal cheeses, and functional dairy, are emerging as key battlegrounds for competitive positioning, attracting both established players and newer entrants. Strategic mergers and acquisitions continue to reshape the ownership landscape, with large dairy groups seeking to consolidate market positions and expand portfolio breadth. Private label dairy has grown in prominence as retail chains develop in-house ranges across standard, organic, and premium tiers, while sustainability credentials are increasingly influencing brand loyalty and long-term supply chain partnerships.

Recent Developments:

- In December 2025, Australian dairy firm Pure Dairy officially opened a state‑of‑the‑art manufacturing facility in Dandenong South, Victoria, marking one of the largest private investments in the sector in decades. The 13,000 m² plant aims to boost production of cheese and dairy products, strengthen supply chains, and support export growth.

Australia Dairy Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Liquid Milk, Cheese, Laban, Yogurt and Curd, Butter and Clarified Butter, Others |

| Applications Covered | Bakery and Confectionary, Clinical Nutrition, Frozen Food, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialist Retailers, Online Stores, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The Australia dairy market size was valued at USD 7.05 Billion in 2025.

The Australia dairy market is expected to grow at a compound annual growth rate of 4.45% from 2026-2034 to reach USD 11.02 Billion by 2034.

Liquid milk holds the largest revenue share of 24.5%, owing to its status as an everyday dietary staple consumed across all demographics and widely distributed through retail, foodservice, and household channels.

Key factors driving the Australia dairy market include rising health awareness, growing consumer preference for premium and specialty products, technological advancements in farming and processing, robust export demand from Asian markets, and increasing applications of dairy across bakery, confectionery, and clinical nutrition.

Major challenges include climate variability and droughts impacting production, intensifying competition from plant-based alternatives, rising input and compliance costs, and supply chain complexities associated with serving both domestic and international markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)