Asia Pacific Smart Windows Market Size, Share, Trends and Forecast by Technology, Type, Application, and Country, 2025-2033

Market Overview:

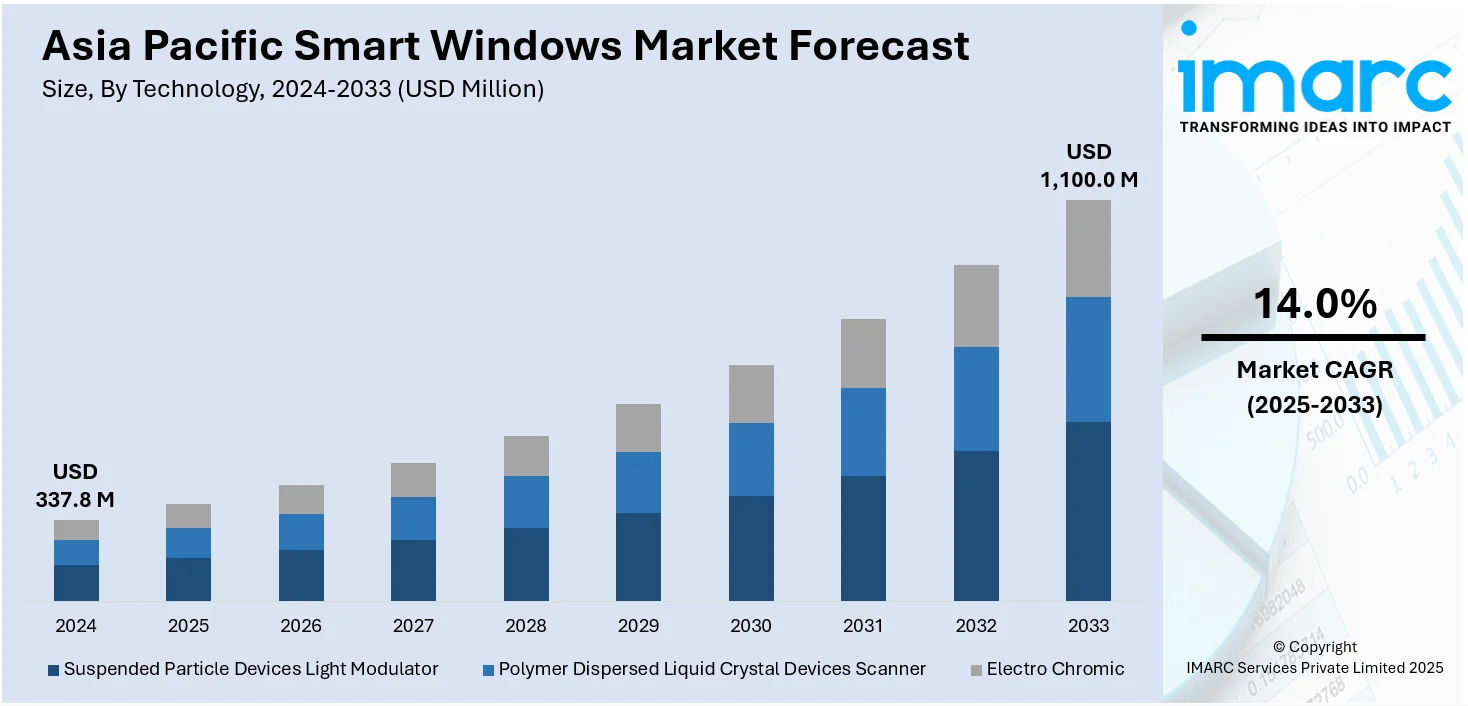

The Asia Pacific smart windows market size reached USD 337.8 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 1,100.0 Million by 2033, exhibiting a growth rate (CAGR) of 14.0% during 2025-2033.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 337.8 Million |

|

Market Forecast in 2033

|

USD 1,100.0 Million |

| Market Growth Rate (2025-2033) | 14.0% |

Smart windows, or switchable windows, refer to electronically powered windows that change color when exposed to light, heat or voltage. They can adjust their opacity from transparent to opaque and are usually operated through a switch, remote or a smartphone application. They are manufactured using materials such as electrochromic, liquid crystal and suspended particle glasses. These materials regulate the amount of heat and light entering the room and thereby assist in minimizing and conserving energy in buildings. As a result, smart windows are extensively used in commercial and residential complexes and automobiles.

To get more information on this market, Request Sample

Significant growth in the construction industry is one of the key factors creating a positive outlook for the market. In line with this, the increasing demand for energy-efficient commercial and residential buildings has resulted in the widespread adoption of smart windows across the Asia Pacific region. Furthermore, the extensive utilization of smart windows in automobiles for maintaining the inner temperature of the vehicles is providing a thrust to the market growth. They also offer features, such as anti-glare, remote access and dynamic light emission adjustment in the vehicle. Other factors, including improvements in the existing infrastructure, along with the implementation of favorable government policies to promote the use of energy-efficient products, are anticipated to drive the market further.

Key Market Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the Asia Pacific smart windows market report, along with forecasts at the regional and country level from 2025-2033. Our report has categorized the market based on technology, type, and application.

Breakup by Technology:

- Suspended Particle Devices Light Modulator

- Polymer Dispersed Liquid Crystal Devices Scanner

- Electro Chromic

Breakup by Type:

- OLED Glass

- Self-Dimming Window

- Self-Repairing

Breakup by Application:

- Residential

- Commercial

- Industrial

- Transport

Breakup by Country:

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

Competitive Landscape:

The competitive landscape of the industry has also been examined along with the profiles of the key players.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Million USD |

| Segment Coverage | Technology, Type, Application, Country |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

We expect the Asia Pacific smart windows market to exhibit a CAGR of 14.0% during 2025-2033.

The increasing demand for energy-efficient system, including smart windows, in commercial and residential complexes, is currently driving the Asia Pacific smart windows market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several Asia Pacific nations resulting in the temporary halt in various construction activities, thereby negatively impacting the smart windows market.

Based on the technology, the Asia Pacific smart windows market can be categorized into suspended particle devices light modulator, polymer dispersed liquid crystal devices scanner, and electro chromic. Among these, electro chromic technology exhibits a clear dominance in the market.

Based on the type, the Asia Pacific smart windows market has been segmented into OLED glass, self- dimming window, and self-repairing. Currently, self-dimming window represents the largest market share.

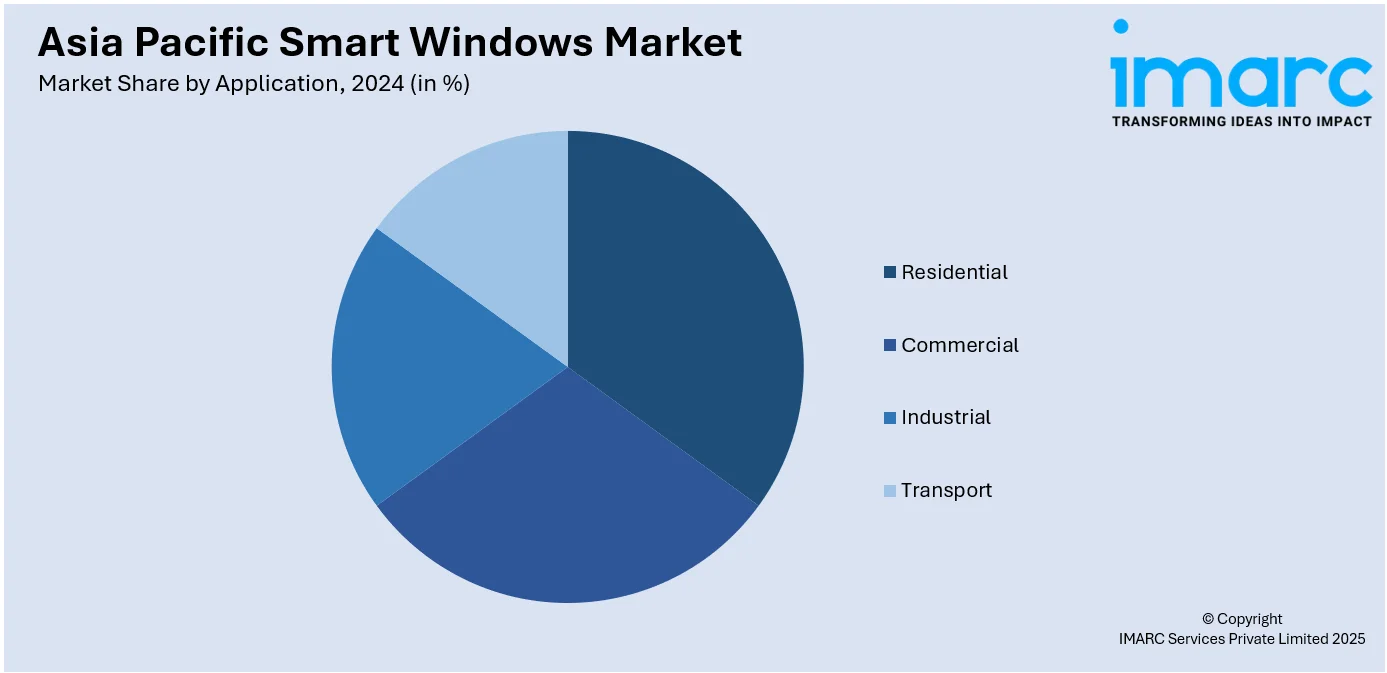

Based on the application, the Asia Pacific smart windows market can be bifurcated into residential, commercial, industrial, and transport. Among these, the transport sector accounts for the majority of the total market share.

On a regional level, the market has been classified into China, Japan, India, South Korea, Australia, Indonesia, and others, where China currently dominates the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)