Anti-venom Market Size, Share, Trends and Forecast by Species, Anti-Venom Type, Mode of Action, End User, and Region, 2026-2034

Anti-venom Market Size and Share:

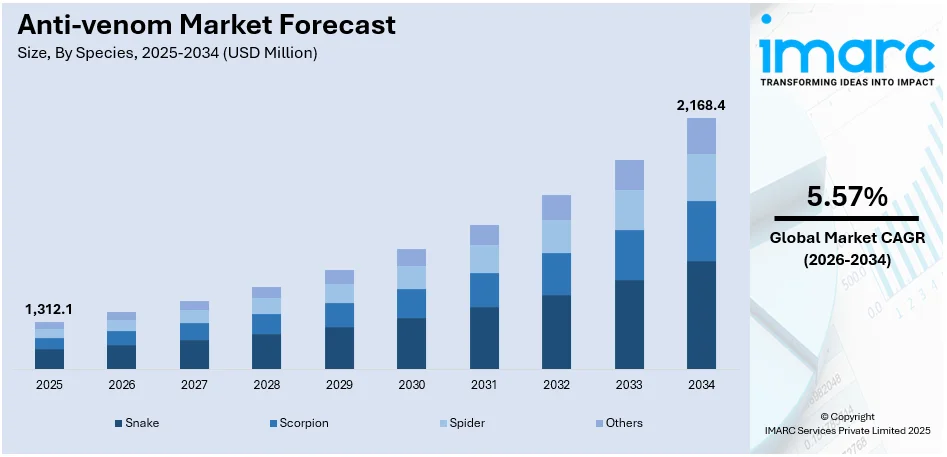

The global anti-venom market size was valued at USD 1,312.1 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 2,168.4 Million by 2034, exhibiting a CAGR of 5.57% during 2026-2034. North America currently dominates the market, holding a significant market share of over 37.8% in 2025. The rising incidences of snake bites and scorpion stings, the implementation of favorable government initiatives, and ongoing innovations in the industry represent some of the key factors driving the market toward growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1,312.1 Million |

|

Market Forecast in 2034

|

USD 2,168.4 Million |

| Market Growth Rate (2026-2034) | 5.57% |

The anti-venom market is driven by several key factors, including the rising incidence of snakebites and venomous insect stings, especially in tropical and subtropical regions. According to the WHO, several victims rely on conventional remedies rather than visiting hospitals or health centers. However, according to the statistics that are currently available, between 4.5 and 5.4 million people are bitten by snakes each year. Of these, 81,000 to 138,000 passes away from complications, and 1.8 to 2.7 million experience clinical disease. As global awareness of the dangers posed by venomous creatures increases, the demand for effective treatments, such as anti-venoms has surged. Rapid urbanization, deforestation, and climate change have expanded human encounters with venomous species, further escalating the need for these life-saving drugs. Advancements in biotechnology and research have led to the development of more effective and faster-acting anti-venoms, thereby improving treatment outcomes and driving market growth.

To get more information on this market Request Sample

In the United States, the anti-venom market is driven by factors such as the increasing awareness of venomous species, rising snakebite cases, and the growing demand for effective treatments. The advancements in biotechnology and the development of monoclonal antibody-based anti-venoms have led to more efficient, targeted therapies. Government initiatives, along with healthcare provider support, ensure timely access to life-saving treatments. The rising prevalence of outdoor activities and recreational tourism in regions with venomous species also contributes to the demand. Additionally, an increasing focus on improving the availability of anti-venoms in emergency medical settings propels market growth in the country. For instance, in February 2024, Scripps Researchers created an antibody that can prevent the effects of deadly toxins contained in the venoms of many different snake species that are found in Australia, Asia, and Africa. The antibody, which shielded mice from the typically fatal venom of snakes like king cobras and black mambas, was reported in Science Translational Medicine on February 21, 2024.

Anti-venom Market Trends:

Rising Incidence of Snakebites and Venomous Stings

The increasing occurrence of snakebites and venomous insect stings, especially in tropical and subtropical regions, is a primary driver for the anti-venom market growth. Factors such as urbanization, deforestation, and climate change have expanded human encounters with venomous species. This growth in cases, coupled with an increased awareness of the importance of timely treatment, has heightened the demand for effective anti-venoms to mitigate fatalities and long-term health complications. According to the World Health Organization (WHO), in many tropical and subtropical nations, snakebite is a neglected public health concern. Most of these take place in Latin America, Asia, and Africa. An estimated 435,000 to 580,000 snake bites that require medical attention occur each year in Africa, and up to 2 million individuals in Asia are bitten by snakes.

Advancements in Biotechnology

Advances in biotechnology have significantly enhanced the development of more effective and targeted anti-venoms. The emergence of monoclonal antibody-based anti-venoms has improved efficacy and safety, offering faster, more precise treatments. New research in venom immunotherapy and recombinant technology has expanded the range of available anti-venoms, addressing various venom types and improving the chances of successful outcomes. These innovations have helped lower production costs while increasing the overall availability and accessibility of anti-venom treatments. For instance, in July 2024, Scientists from the Liverpool School of Tropical Medicine and the University of Sydney discovered the finding that heparin, which is used as a blood thinner, can also be used as a cheap counteragent for cobra venom. Every year, snakes claim the lives of almost 100,000 humans and Heparin can serve as an affordable antidote to cobra venom.

Government and Healthcare Support

Government initiatives, along with increasing healthcare system investments, are crucial drivers of the anti-venom market. Many governments in endemic regions allocate funds for acquiring and distributing anti-venoms, ensuring accessibility, particularly in rural and underserved areas. Additionally, public health organizations and NGOs partner to improve awareness and availability of life-saving treatments. This collective effort plays a vital role in reducing mortality rates from venomous bites and enhancing emergency medical responses in affected areas. For instance, in March 2024, The National Action Plan for Prevention and Control of Snakebite Envenoming (NAP-SE) in India was introduced by Union Health Secretary. NAPSE offers the Indian states a comprehensive framework for creating their action plans for managing, preventing, and controlling snakebites using the "One Health" concept, to halve the number of snakebite deaths by 2030. All levels of interested stakeholders will carry out the actions envisioned under the human, wildlife, tribal, and animal health components.

Anti-venom Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global anti-venom market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on species, anti-venom type, mode of action, and end user.

Analysis by Species:

- Snake

- Scorpion

- Spider

- Others

Snake stand as the largest component in 2025, holding around 52.3% of the market. Snakes hold the largest share in the anti-venom market due to the high global incidence of snakebites, particularly in tropical and subtropical regions, where they pose a significant public health issue. Snakebites often result in severe morbidity or mortality if untreated, driving the demand for effective anti-venoms. Moreover, the diversity and potency of snake venoms require specialized, region-specific anti-venoms, leading to extensive research and production efforts. Government and healthcare initiatives focus heavily on addressing snakebite envenomation due to its impact on vulnerable populations, further boosting the segment's dominance in the anti-venom market.

Analysis by Anti-venom Type:

- Polyvalent Anti-venom

- Monovalent Anti-venom

Polyvalent anti-venom leads the market with around 66.7% of the market share in 2025. Polyvalent anti-venom holds the largest share in the anti-venom market due to its broad-spectrum efficacy against multiple venomous species. This versatility makes it highly valuable in regions where diverse venomous creatures coexist, reducing the need for species-specific treatments. Polyvalent anti-venoms are especially critical in emergencies where identifying the exact species may be difficult. Their widespread availability and convenience for healthcare providers further enhance their adoption. Additionally, advancements in production techniques and improved safety profiles have increased their effectiveness and reduced adverse reactions, making them the preferred choice for treating envenomation in many parts of the world.

Analysis by Mode of Action:

- Cytotoxic

- Neurotoxic

- Haemotoxic

- Cardiotoxic

- Myotoxic

- Others

Neurotoxic leads the market with around 32.3% of the market share in 2025. Neurotoxic anti-venom holds the largest share in the anti-venom market due to the prevalence and severity of neurotoxic envenomation caused by venomous snakes, such as cobras and kraits, and other creatures. Neurotoxins disrupt nerve signaling, leading to paralysis, respiratory failure, and potentially death, requiring immediate and effective treatment. The high mortality and morbidity associated with neurotoxic bites drive demand for specialized anti-venoms. Moreover, neurotoxic envenomation is common in regions with a significant burden of snakebites, prompting governments and healthcare systems to prioritize its treatment. Advances in neurotoxin-targeted therapies further support this segment's dominance in the anti-venom market.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Clinics

- Ambulatory Surgical Centers

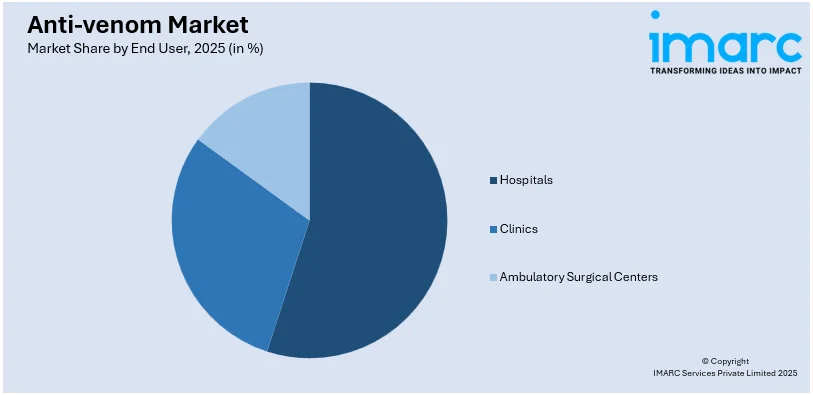

Hospitals leads the market with around 62.8% of market share in 2025. Hospitals hold the largest share in the anti-venom market due to their central role in treating venomous bites and stings. They are equipped with specialized facilities and trained medical personnel to administer anti-venom, monitor patients, and manage potential complications. Hospitals are often the primary healthcare providers in emergencies, where timely administration of anti-venom is critical. Moreover, government programs and public health initiatives ensure anti-venom availability in hospitals, particularly in regions prone to envenomation. The trust in hospitals for accurate diagnosis, species identification, and comprehensive care further strengthens their position as the leading end-user in the anti-venom market.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 37.8%. In North America, the anti-venom market is driven by the rising prevalence of venomous bites and stings from species like rattlesnakes, copperheads, and black widow spiders. Outdoor activities such as hiking and camping, combined with expanding urbanization into wildlife habitats, increase human encounters with venomous species. The region's advanced healthcare infrastructure supports the availability and accessibility of anti-venom, ensuring timely treatment in emergency settings. Technological advancements, such as improved production techniques and the development of safer, more effective anti-venoms, contribute to market growth. Government initiatives and public health awareness campaigns further promote the use of anti-venoms, especially in high-risk regions. Additionally, North America's significant focus on research and development fosters innovations like monoclonal antibody-based anti-venoms, enhancing treatment precision. The growing awareness among healthcare providers and the public about the dangers of envenomation also drives demand, solidifying North America's role as a key market for anti-venoms.

Key Regional Takeaways:

United States Anti-Venom Market Analysis

In 2025, the United States accounted for the market share of over 88.90%. The demand for advanced treatments is fueling the development of immunological therapies that provide rapid and effective solutions for venomous bites and stings. A robust healthcare infrastructure supports the adoption of these innovations, alongside rising investments in pharmaceutical research. According to the National Association of Manufacturers, the U.S. pharmaceutical manufacturing industry, contributing USD 355 Billion to the economy in 2021 (a 24% rise in direct output since 2019), is pivotal in advancing anti-venom production, leveraging its growth to address critical healthcare challenges effectively. The prevalence of venomous species across various regions necessitates the development of region-specific solutions, pushing research organizations to focus on tailored formulations. Public awareness campaigns about venom-related hazards and available remedies are also contributing to higher demand. Moreover, stringent regulatory frameworks ensure the availability of high-quality, safe treatments, attracting significant investments in production and distribution. The collaboration between research institutions and hospitals is enhancing the accessibility and effectiveness of these remedies. The growing interest in biopharmaceuticals further drives innovation, with technological advancements enabling faster development of more efficient treatments. Overall, favorable healthcare policies and advancements in treatment methodologies are pivotal drivers in this space.

Asia Pacific Anti-Venom Market Analysis

High incidences of venomous bites and stings in densely populated rural regions are creating demand for accessible treatments. According to the WHO, in Asia up to 2 million people are envenomed by snakes each year. This is further supported by significant government initiatives aimed at increasing healthcare accessibility in remote areas. According to the India Brand Equity Foundation, the Indian healthcare industry, valued at USD 372 Billion in 2023, is rapidly expanding with USD 2.7-3.5 Million new tech jobs expected, enhancing accessibility to critical services like anti-venom treatments. Increased healthcare spending, now at 2.1% of GDP, and an 8% CAGR in the hospital market further boost advancements in emergency care delivery. Local pharmaceutical companies are increasingly investing in manufacturing effective therapeutic solutions tailored to regional venom profiles. Traditional medicine's integration with modern biopharmaceutical methods is also becoming a key driver, allowing cost-effective production and localized distribution. Rising awareness about envenomation risks and first-aid measures is encouraging quicker treatment-seeking behaviors. Advances in medical training and better-equipped healthcare facilities in emerging economies are enhancing access to therapeutic solutions. The growth in private healthcare investments complements government efforts, ensuring broader availability of life-saving treatments in high-risk zones. A growing focus on health technology further supports the rapid production and distribution of therapies in this region.

Europe Anti-venom Market Analysis

Strict regulatory frameworks encourage the development of effective and safe formulations for managing venom-related emergencies. Increasing public interest in wildlife and outdoor activities has heightened awareness of the risks associated with envenomation. For instance, wildlife tourism, comprising 7% of global tourism, sees Europe as a key market, with 80% of African wildlife tourists and 58% of European tour operators engaged, driving interest in anti-venom research and conservation benefits. Partnerships between universities and research institutions foster innovative approaches to venom neutralization and symptom management. Government-backed initiatives emphasize improving supply chains and ensuring faster distribution of vital treatments. Conservation programs for venomous species also generate valuable data, contributing to enhanced knowledge for developing neutralizing agents. Europe’s diverse climatic regions harbor different venomous species, necessitating region-specific treatments and boosting research activities. Advances in recombinant DNA technology and protein engineering are paving the way for synthetic formulations with fewer side effects. Training and education programs target at-risk groups, ensuring timely access to necessary interventions.

Latin America Anti-Venom Market Analysis

The prevalence of venomous snake species across tropical and subtropical regions propels the demand for life-saving interventions, as bites from these creatures often result in severe medical conditions. Increased public awareness of the risks associated with such bites has spurred demand for improved treatment solutions. Government initiatives aimed at reducing mortality rates associated with envenomation are also key contributors to advancements in this field. Moreover, collaborations between research institutions and biotechnology companies are fostering innovation, focusing on the development of more effective solutions. The region's expanding medical infrastructure supports the distribution of these interventions, particularly in remote areas where bites are more frequent. According to ITA, Brazil, the largest healthcare market in Latin America with healthcare expenditure of 9.47% of its GDP approximately USD 161 Billion. This robust medical infrastructure supports advancements in anti-venom production, crucial for addressing venomous bites in a biodiverse region. Additionally, educational campaigns highlighting the importance of rapid treatment are driving awareness among rural populations, emphasizing the urgency of addressing envenomation incidents promptly to mitigate fatalities.

Middle East and Africa Anti-Venom Market Analysis

The unique biodiversity in arid and semi-arid regions, including scorpions and other venomous species, drives demand for specialized interventions. Increased agricultural and industrial activity in rural areas has elevated human-animal interactions, heightening the need for effective solutions. According to WHO, snakebite incidents are notably high in Iraq, Jordan, Lebanon, Oman, Saudi Arabia, and Yemen, with Saudi Arabia alone reporting 1,019 cases from 2005–2010. These cases provide critical data for developing targeted and region-specific antivenom therapies. International partnerships and local production facilities are improving access to these treatments in underserved regions. Moreover, the rising focus on public health preparedness has led to enhanced resource allocation for venom-related medical emergencies. Advances in venom research are enabling the development of region-specific solutions, considering the local venom profiles. Public health campaigns targeting rural and nomadic communities are helping to spread awareness about envenomation risks and preventive measures, fostering a culture of preparedness and swift response to incidents. Additionally, the focus on training healthcare providers for venom emergencies enhances treatment outcomes.

Competitive Landscape:

The anti-venom market is highly competitive, with major players such as Pfizer, Bharat Serums and Vaccines, CSL Behring, and Instituto Bioclon leading the industry. These companies focus on extensive research and development to produce effective and safer anti-venoms. Emerging biotechnology firms are introducing advanced solutions like monoclonal antibody-based anti-venoms, intensifying competition. Strategic collaborations with governments and health organizations ensure market access in endemic regions. Manufacturers emphasize expanding distribution networks and improving affordability to enhance market presence. Regional players also play a significant role by catering to localized venom-specific needs, making the competitive landscape dynamic and innovation-driven.

The report has also analysed the competitive landscape of the market with some of the key players being:

- Bharat Serums and Vaccines Limited (BSV)

- Boehringer Ingelheim International GmbH

- Boston Scientific Corporation

- CSL Limited

- Haffkine Bio-Pharmaceutical Corporation Limited

- Incepta Pharmaceuticals Limited

- Merck & Co. Inc.

- Merck KGaA

- MicroPharm Limited

- Pfizer Inc.

- Rare Disease Therapeutics Inc.

Latest News and Developments:

- August 2024: Three companies have signed an MoU to locally produce anti-snake venom drugs in Nigeria, addressing the country's critical shortage. The partnership includes Echitab Study Limited, the Federal Ministry of Health, and other stakeholders. This initiative aims to ensure affordable and accessible treatment for snakebite victims. The collaboration marks a significant step toward reducing reliance on imported anti-venom products.

- August 2024, MicroPharm UK, announced a partnership with Nigeria's AMA Medical Manufacturing to establish a facility for affordable anti-venom production. This collaboration entails a multi-Million-dollar investment and years of technology transfer, aiming to enhance local manufacturing capabilities and improve access to life-saving treatments in Nigeria.

- August 2022: Bharat Serums and Vaccines Ltd. partnered with the Indian Institute of Science (IISc) to develop antivenom for snakebite treatment in India. This collaboration focuses on advancing antivenom therapy to provide more effective solutions. The initiative aims to address the critical need for life-saving treatments for snakebite victims. This step is expected to enhance healthcare outcomes in rural and high-risk areas.

- March 2022: Ophirex, Inc. announced that the U.S. FDA granted Fast Track designation to varespladib-methyl, an anti-venom treatment for snakebites. The company is conducting clinical trials for this oral broad-spectrum antidote, targeting its use in the United States and India. Varespladib-methyl aims to provide effective and accessible treatment for various snakebite envenomations. This milestone underscores advancements in addressing a critical global health challenge.

- April 2021: Rare Disease Therapeutics, Inc. announced an expanded FDA-approved indication for ANAVIP antivenom. ANAVIP now includes treatment for envenomation caused by all North American Pit Vipers. The updated approval enhances the availability of effective treatment for snakebite victims in the region. ANAVIP is lauded for its extended neutralizing effects, reducing the risk of recurrent venom effects. This expansion marks a pivotal advancement in managing pit viper envenomation in North America.

Anti-venom Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Species Covered | Snake, Scorpion, Spider, and Others |

| Anti-venom Type Covered | Polyvalent Anti-venom, Monovalent Anti-venom |

| Mode of Action Covered | Cytotoxic, Neurotoxic, Haemotoxic, Cardiotoxic, Myotoxic, and Others |

| End User Covered | Hospitals, Clinics, Ambulatory Surgical Centers |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bharat Serums and Vaccines Limited (BSV), Boehringer Ingelheim International GmbH, Boston Scientific Corporation, CSL Limited, Haffkine Bio-Pharmaceutical Corporation Limited, Incepta Pharmaceuticals Limited, Merck & Co. Inc., Merck KGaA, MicroPharm Limited, Pfizer Inc., Rare Disease Therapeutics Inc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the anti-venom market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global anti-venom market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the anti-venom industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

Anti-venom is a medical treatment used to neutralize the toxic effects of venom from snakebites, insect stings, or other venomous creatures. It contains antibodies or other substances that counteract the venom, preventing or reducing severe symptoms like paralysis, tissue damage, and organ failure, thereby increasing the chances of survival.

The anti-venom market was valued at USD 1,312.1 Million in 2025.

IMARC estimates the global Anti-venom market to exhibit a CAGR of 5.57% during 2026-2034.

The anti-venom market is driven by the rising incidence of venomous bites, advancements in biotechnology, increased awareness of envenomation risks, and government initiatives for better healthcare access. Growing outdoor activities, climate change, and the demand for safer, more effective anti-venoms also contribute to market expansion and innovation.

Snakes dominate the anti-venom market due to the high incidence of snakebites and their severe health consequences globally.

Polyvalent anti-venom leads the market by anti-venom type due to its broad-spectrum effectiveness, treating multiple venomous species with a single treatment.

Neurotoxic represented the largest segment by mode of action, due to the high prevalence and severity of neurotoxic envenomation, causing life-threatening conditions.

According to the report, hospitals dominate the anti-venom market due to their expertise, facilities, and critical role in emergency envenomation treatment and monitoring.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein North America currently dominates the global market.

Some of the major players in the global anti-venom market include Bharat Serums and Vaccines Limited (BSV), Boehringer Ingelheim International GmbH, Boston Scientific Corporation, CSL Limited, Haffkine Bio-Pharmaceutical Corporation Limited, Incepta Pharmaceuticals Limited, Merck & Co. Inc., Merck KGaA, MicroPharm Limited, Pfizer Inc., Rare Disease Therapeutics Inc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)