Aircraft Hangar Market Size, Share, Trends and Forecast by Product, Construction, Application, and Region, 2025-2033

Aircraft Hangar Market Size and Share:

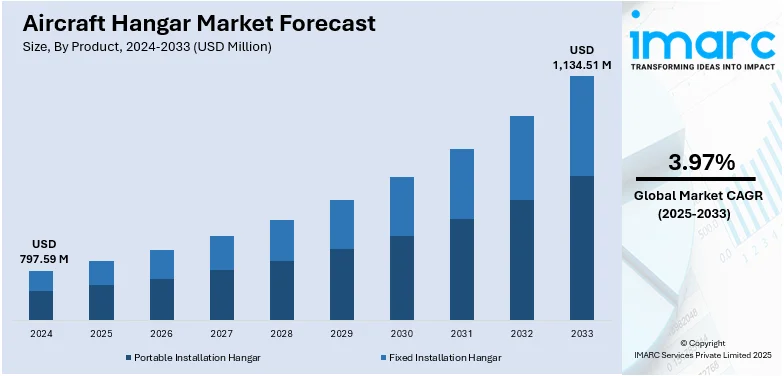

The global aircraft hangar market size was valued at USD 797.59 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 1,134.51 Million by 2033, exhibiting a CAGR of 3.97% from 2025-2033. North America currently dominates the market, holding a market share of over 36.7% in 2024. The market is growing due to rising demand for secure storage, maintenance and operational facilities for commercial, military and private aircraft. Advancements in construction materials, automation and sustainable designs are enhancing efficiency and durability. Increasing investments in aviation infrastructure and MRO facilities further support market expansion strengthening overall industry growth and aircraft hangar market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024 |

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 797.59 Million |

| Market Forecast in 2033 | USD 1,134.51 Million |

| Market Growth Rate (2025-2033) | 3.97% |

The aircraft hangar market is driven by growing aviation traffic, expansion of commercial airlines and rising investments in airport infrastructure. According to the data published by the International Air Transport Association, global air passenger demand hit a record high in 2024 with traffic rising 10.4% to 9.5 trillion RPKs. International demand surged by 13.6% while domestic traffic grew 5.7%. Overall capacity increased 8.7% achieving a load factor of 83.5% surpassing pre-pandemic levels by 3.8%. Increased demand for aircraft maintenance, repair and overhaul (MRO) services further supports hangar construction. Additionally, growing fleets of private jets and military aircraft necessitate specialized hangar facilities. Technological advancements including automated doors, climate control systems and modular designs also propel aircraft hangar market demand. Enhanced safety standards, regulatory compliance and the need for efficient aircraft storage and protection significantly contribute to industry expansion.

The United States aircraft hangar market is driven by increasing air travel demand, significant investment in airport infrastructure and a growing fleet of commercial and private aircraft. According to the data published by the Bureau of Transportation Statistics, in August 2024, U.S. airlines recorded 86.8 million passengers, a 4.5% increase from last year. Domestic passengers reached 74.8 million also a monthly high while international enplanements totaled 12 million marking a record for August. Rising defense expenditure and modernization of military aviation facilities also fuel market growth. Additionally, the expansion of aircraft maintenance, repair and overhaul (MRO) services necessitates advanced hangar solutions. Strict safety and regulatory requirements encourage investment in state-of-the-art hangars featuring automated doors, energy-efficient designs, and enhanced weather protection systems, further strengthening market demand across the US.

Aircraft Hangar Market Trends:

Growing Demand for Eco-Friendly Designs

Eco-friendly designs in aircraft hangars are increasingly preferred due to heightened environmental awareness and sustainability targets set by airports and airlines. Incorporation of energy-efficient LED lighting significantly reduces electricity consumption and operational costs. Installation of solar panels supports renewable energy use cutting carbon footprints. For instance, in October 2024, ATS Technic announced its plans to construct an innovative aluminum-based hangar at Dubai South aimed at cutting carbon emissions by up to 60%. Designed in line with LEED standards the facility will introduce advanced energy-efficient features establishing a new benchmark for sustainable aviation infrastructure in the region by 2025. Additionally, use of sustainable building materials like recycled steel and eco-friendly insulation enhances overall environmental benefits. Such sustainable practices help hangar operators meet regulatory standards, improve corporate image, and achieve long-term cost savings.

Increased Use of Smart Technology

The integration of smart technology in aircraft hangars including IoT-enabled devices, automated systems, and remote monitoring solutions enhances operational efficiency and safety. IoT sensors enable real-time monitoring of aircraft maintenance conditions, hangar security and environmental parameters such as humidity and temperature. Automated door systems facilitate faster aircraft movement reducing turnaround times. Remote surveillance and predictive maintenance software help identify potential issues early minimizing downtime. Companies are increasingly adopting virtual platforms to enhance customer engagement and showcase aircraft effectively. For instance, in December 2023, Jetcraft launched a virtual hangar offering 24/7 access to a range of aircraft in an immersive 360-degree experience. Following its Decentraland lounge, the hangar caters to tech-savvy buyers, providing seamless exploration of business jets. Collectively, these technologies improve productivity, safety compliance, and reduce long-term operational costs.

Expansion of Maintenance, Repair, and Overhaul (MRO) Facilities

The expansion of Maintenance, Repair, and Overhaul (MRO) facilities significantly drives the demand for aircraft hangar construction. With increasing airline fleets and stringent safety regulations, there is a growing need for specialized hangars equipped for comprehensive maintenance operations. Modern MRO hangars incorporate advanced infrastructure, including heavy maintenance docks, specialized tooling, and dedicated workspaces for aircraft repairs and servicing. The rising demand for efficient, compliant maintenance operations further accelerates hangar investments are creating positive aircraft hangar market outlook across the world.

Aircraft Hangar Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global aircraft hangar market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on product, construction, and application.

Analysis by Product:

- Portable Installation Hangar

- Fixed Installation Hangar

Fixed installation hangar stands as the largest product in 2024, holding around 77.4% of the market. Fixed installation hangars dominate the aircraft hangar market due to their large-scale, permanent structures designed for long-term aircraft storage, maintenance, and repairs. These hangars offer superior durability, security, and customization options, catering to commercial airlines, military bases, and MRO facilities. Their demand is driven by increasing air traffic, rising fleet expansions, and stringent aircraft maintenance regulations. With advancements in hangar design, including climate control and automation, fixed installation hangars remain the preferred choice for operators requiring reliable, high-capacity storage solutions.

Analysis by Construction:

- Steel Construction

- Wood Construction

- Fabric Construction

Steel construction leads the market with around 65.3% of market share in 2024. Steel construction dominates the aircraft hangar market due to its strength, durability, and cost efficiency. Steel hangars provide superior resistance to harsh weather conditions, ensuring long-term protection for aircraft. Their modular design allows for customization, rapid assembly, and expansion to accommodate growing fleet sizes. Increasing investments in aviation infrastructure, military bases, and MRO facilities further drive demand. With advancements in corrosion-resistant coatings and prefabrication techniques, steel remains the preferred material for aircraft hangars, offering reliability and structural integrity.

Analysis by Application:

- Commercial

- Military

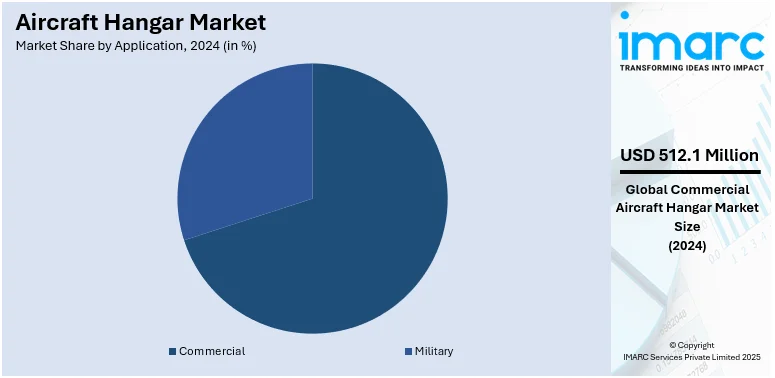

Commercial leads the market with around 64.2% of market share in 2024. The commercial sector leads the aircraft hangar market, driven by rising air passenger traffic, fleet expansions, and increasing airline investments in maintenance and storage facilities. Airlines and MRO providers require large, durable hangars for scheduled maintenance, repairs, and overnight storage. Growing demand for wide-body aircraft storage and advancements in hangar automation further boost market growth. With airports expanding infrastructure and airlines prioritizing operational efficiency, commercial aircraft hangars remain the dominant segment, ensuring aircraft safety, security, and regulatory compliance.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 36.7%. North America holds the largest share in the aircraft hangar market, driven by a well-established aviation industry, extensive commercial and military aircraft fleets, and significant investments in MRO infrastructure. The region's major airlines, defense organizations, and private aviation companies demand advanced hangar facilities for storage, maintenance, and operations. Stringent FAA regulations and ongoing airport expansion projects further support market growth. With the presence of key industry players and technological advancements in hangar design, North America remains the leading market for aircraft hangars.

Key Regional Takeaways:

United States Aircraft Hangar Market Analysis

In 2024, the United States accounted for over 88.50% of the aircraft hangar market in North America. The U.S. aircraft hangar market is expanding due to rising demand from commercial aviation, military operations, private aircraft owners, and the space industry. A well-established aviation infrastructure and high air traffic volume are fueling the need for advanced, large-capacity hangars designed for maintenance, repair, and storage. Key market trends include the adoption of smart hangars with automated systems, advanced climate control, and energy-efficient designs that enhance operational efficiency. Multi-functional hangar spaces are gaining traction, integrating cutting-edge technologies to improve aircraft servicing, safety, and logistical operations. Government investments are a major growth driver. The Federal Aviation Administration (FAA) continues to fund aviation infrastructure, while the Department of Defense plays a crucial role in military hangar development. According to the Department of the Air Force, USD 9.4 Billion has been allocated in its 2025 budget for readiness, emphasizing modernization to enhance military capabilities. The private aviation sector and growing space exploration initiatives are further accelerating hangar development. Companies are increasingly adopting prefabricated structures and modular designs to reduce costs and construction timelines. With sustained investments and technological advancements, the U.S. aircraft hangar market is poised for long-term growth.

Europe Aircraft Hangar Market Analysis

Europe’s aircraft hangar market is shaped by growing air travel demand, stringent environmental regulations, and the presence of leading aircraft manufacturers like Airbus. A recent study by green group Transport & Environment (T&E) projects that Europe’s aviation industry plans to double its passenger traffic by 2050, further amplifying the need for advanced hangar facilities. Major airports and defense sectors drive the demand for hangars built with energy-efficient materials and equipped with automated systems. Sustainable infrastructure is increasingly prioritized, with green hangars incorporating features such as solar panels and rainwater harvesting gaining traction. This focus on sustainability is complemented by the region's push for maintenance, repair, and overhaul (MRO) facilities, particularly in aviation hubs like Germany, France, and the UK. To address space and cost constraints while maintaining high standards, the market also turns to prefabrication and modular designs, ensuring compliance with European aviation standards and preparing for future growth.

Asia Pacific Aircraft Hangar Market Analysis

Asia Pacific's aircraft hangar market is expanding due to rising air passenger traffic, fleet expansion, and increasing investments in airport infrastructure. Countries like China, India, and Japan are witnessing significant growth in MRO facilities and military aviation, which drives demand for large, technologically advanced hangars. For instance, the India Brand Equity Foundation (IBEF) projects that India will become the third-largest aviation market in terms of passengers by 2024 and will require over 2,200 aircraft by 2042, further propelling hangar development. Additionally, the adoption of smart hangars with automated climate control and digital monitoring systems is on the rise. Government initiatives to enhance airport capacities, coupled with increasing private sector investments, further boost the market, while prefabricated structures gain popularity due to their cost efficiency and faster construction times.

Latin America Aircraft Hangar Market Analysis

The Latin American aircraft hangar market is driven by increasing aviation activities, rising demand for MRO services, and the expansion of regional airports. Brazil and Mexico are leading markets due to their growing commercial and defense aviation sectors. According to the Mexico Projects Hub, the Mexican Airport System (SAM) consists of 80 airports, including 66 international and 14 domestic airports, as well as 1,524 aerodromes and 589 heliports. Notably, three airport groups (OMA, ASUR, and GAP), along with the AICM, handle 96% of the passenger traffic and 91% of the cargo. This infrastructure growth is contributing to an increased need for advanced hangars, particularly in high-traffic areas. The focus on cost-effective, prefabricated hangar solutions is growing to support smaller airports and private aircraft storage. Infrastructure modernization and government-backed projects are further fueling market expansion. However, economic fluctuations and budget constraints continue to pose challenges to large-scale investments in new hangar facilities.

Middle East and Africa Aircraft Hangar Market Analysis

The Middle East and Africa region is witnessing steady growth in the aircraft hangar market, driven by expanding airline fleets, military aviation investments, and rising MRO demand. Key players, including the UAE, Saudi Arabia, and South Africa, are investing in large-scale airport infrastructure projects. Recently, a report showcased investment opportunities valued at approximately USD 100 Billion and over 70 agreements worth USD 12 Billion, underlining robust confidence in the sector. In desert regions, where extreme weather conditions impact aircraft maintenance, there is a strong demand for advanced, climate-controlled hangars. The region’s focus on aviation tourism and cargo transport further bolsters market expansion, with a notable shift toward prefabricated and modular hangar solutions.

Competitive Landscape:

The aircraft hangar market is highly competitive, with companies focusing on innovation, customization, and durability to meet diverse aviation requirements. Key players emphasize advanced materials, modular construction, and automation to enhance efficiency and cost-effectiveness. Strategic partnerships, mergers, and acquisitions are common as firms expand their market presence and technological capabilities. The growing demand for sustainable hangars with energy-efficient designs and smart monitoring systems further intensifies competition. Market participants also invest in expanding manufacturing facilities and global distribution networks to cater to rising demand from commercial, military, and private aviation sectors, ensuring long-term growth and market leadership.

The report provides a comprehensive analysis of the competitive landscape in the aircraft hangar market with detailed profiles of all major companies including:

- Allied Steel Buildings Inc.

- Big Top Manufacturing Inc.

- BlueScope Construction, Inc.

- DIUK Arches Ltd.

- Erect-A-Tube Inc.

- Fulfab Inc.

- HTS TENTIQ GmbH

- J & M Steel Solutions Inc.

- John Reid & Sons (Strucsteel) Ltd.

- Rubb Buildings Ltd. (Zurhaar AS)

Latest News and Developments:

- In March 2025, Katowice Airport announced its plans to construct Hangar H4, expanding aircraft maintenance capacity with a PLN 1.5 billion investment. The 11.2K m² hangar, set to be completed by Q1 2026, will create 200-300 jobs and support ongoing infrastructure growth, enhancing the airport’s MRO capabilities.

- In September 2024, Asia Digital Engineering (ADE) opened a 380,000 ft² hangar in Kuala Lumpur the largest in Malaysia, featuring 14 narrowbody maintenance lines primarily for AirAsia. ADE plans further expansion with additional hangars and enhanced maintenance capabilities, emphasizing its digital innovations and potential third-party services.

- In July 2024, DHL Express Spain announced its plans to invest over EUR 40 million in a new aircraft maintenance hangar at Vitoria-Gasteiz, set to open by mid-2027. This facility will enhance maintenance capacity, employ around 50 workers, and support sustainability efforts by being carbon-neutral, reducing reliance on non-DHL European maintenance sites.

Aircraft Hangar Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Portable Installation Hangar, Fixed Installation Hangar |

| Constructions Covered | Steel Construction, Wood Construction, Fabric Construction |

| Applications Covered | Commercial, Military |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Allied Steel Buildings Inc., Big Top Manufacturing Inc., BlueScope Construction, Inc., DIUK Arches Ltd., Erect-A-Tube Inc., Fulfab Inc., HTS TENTIQ GmbH, J & M Steel Solutions Inc., John Reid & Sons (Strucsteel) Ltd., Rubb Buildings Ltd. (Zurhaar AS), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aircraft hangar market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global aircraft hangar market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aircraft hangar industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The aircraft hangar market was valued at USD 797.59 Million in 2024.

IMARC estimates the aircraft hangar market to reach USD 1,134.51 Million by 2033, exhibiting a CAGR of 3.97% during 2025-2033.

The aircraft hangar market is driven by increasing global air traffic, rising demand for MRO facilities, expanding aircraft fleets and advancements in hangar automation. Growing investments in aviation infrastructure and stricter maintenance regulations further propel market growth.

North America holds the largest aircraft hangar market share, driven by a well-established aviation sector, increasing investments in MRO facilities, and a growing commercial and military aircraft fleet. Stringent regulatory requirements, technological advancements, and airport infrastructure expansion further strengthen the region’s market leadership.

Some of the major players in the aircraft hangar market include Allied Steel Buildings Inc., Big Top Manufacturing Inc., BlueScope Construction, Inc., DIUK Arches Ltd., Erect-A-Tube Inc., Fulfab Inc., HTS TENTIQ GmbH, J & M Steel Solutions Inc., John Reid & Sons (Strucsteel) Ltd., Rubb Buildings Ltd. (Zurhaar AS), etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)