India Cold Pressed Oil Market Size, Share, Trends and Forecast by Form, Packaging Type, Pack Size, Distribution Channel, and Region, 2026-2034

India Cold Pressed Oil Market Size, Share, Trends & Forecast (2026-2034)

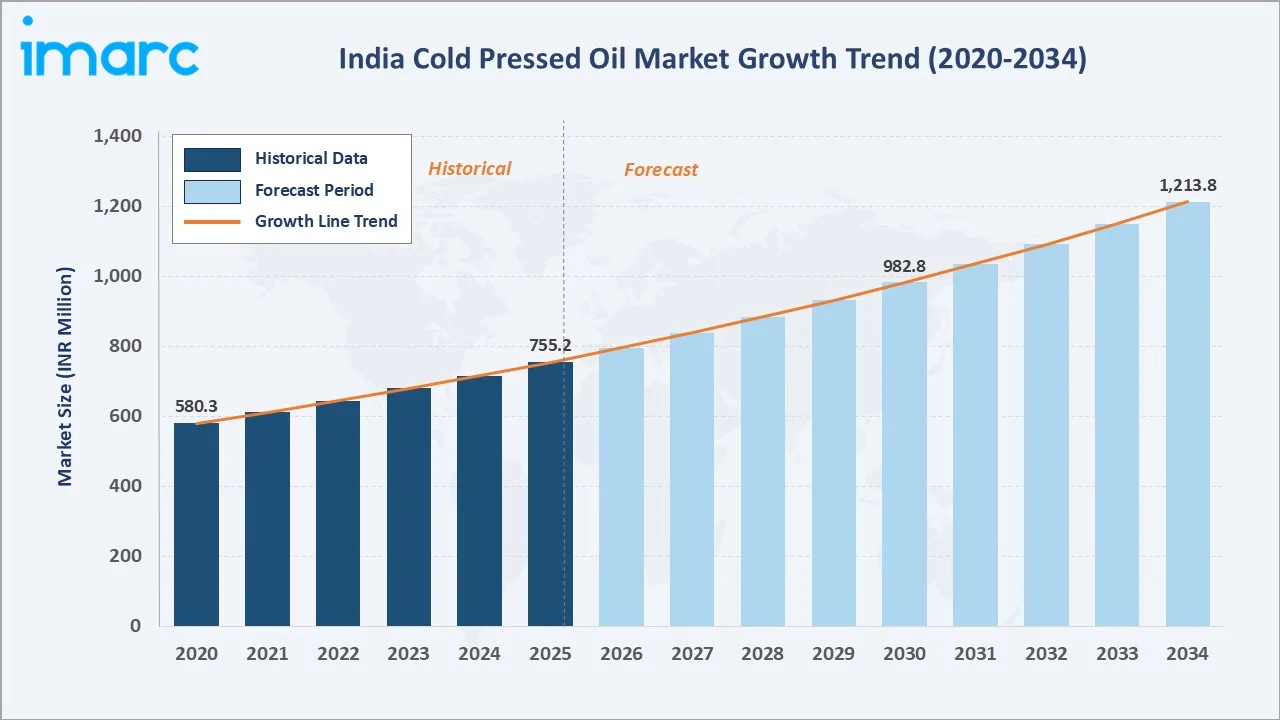

The India cold pressed oil market reached INR 755.2 Million in 2025 and is projected to reach INR 1,213.8 Million by 2034, growing at a CAGR of 5.41% during 2026-2034. The market is driven by rising health consciousness, Ayurvedic revival, and growing consumer preference for chemical-free, nutrient-preserving food processing methods. Traditional extraction techniques preserving essential fatty acids and antioxidants position these oils as premium wellness products across urban and semi-urban households.

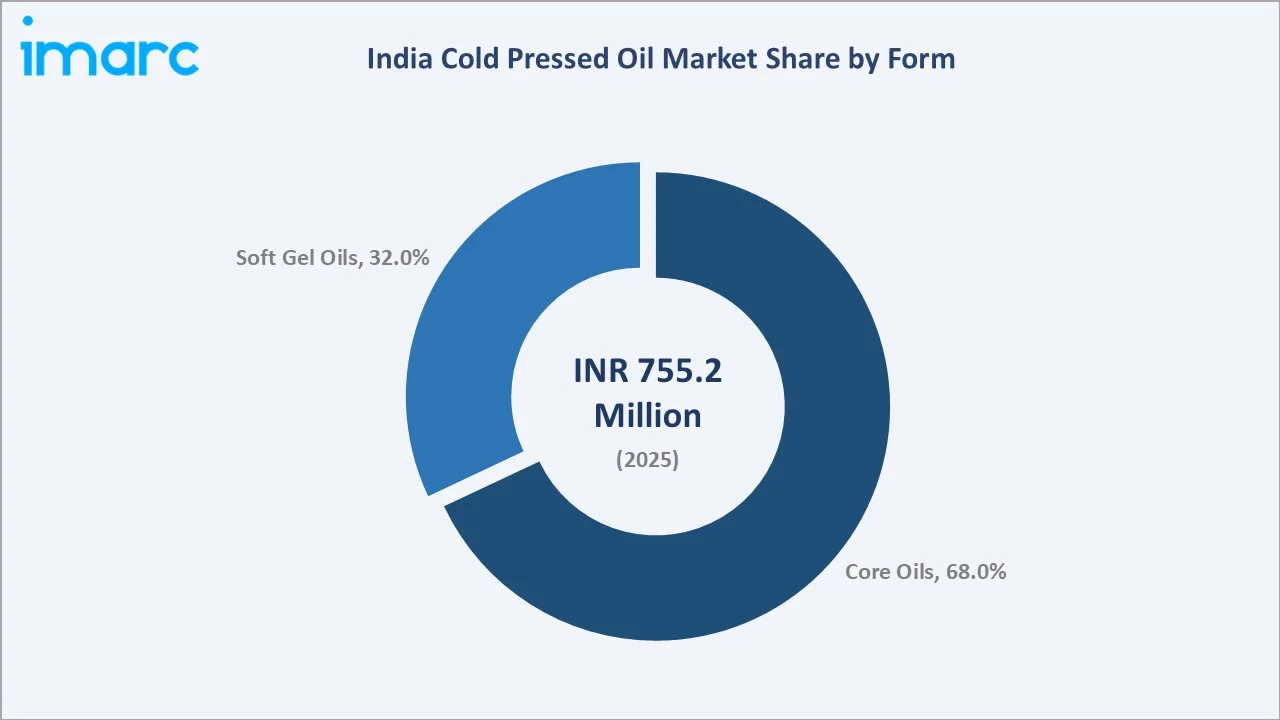

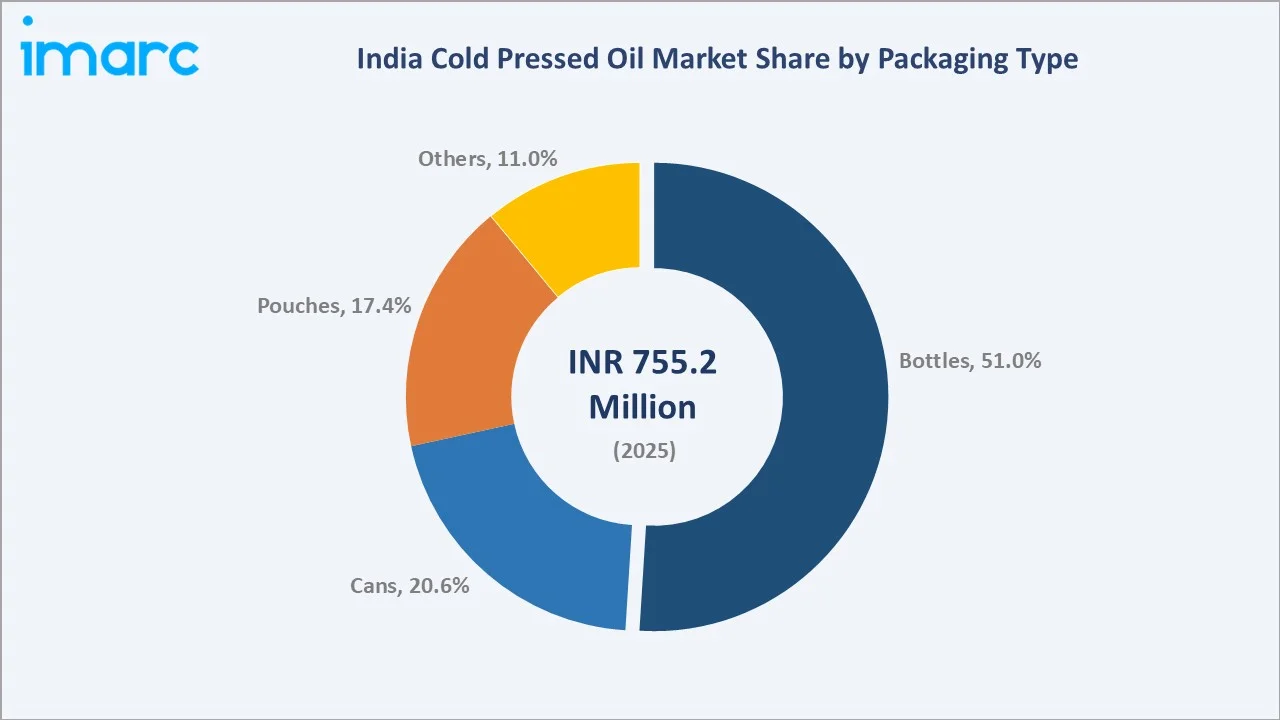

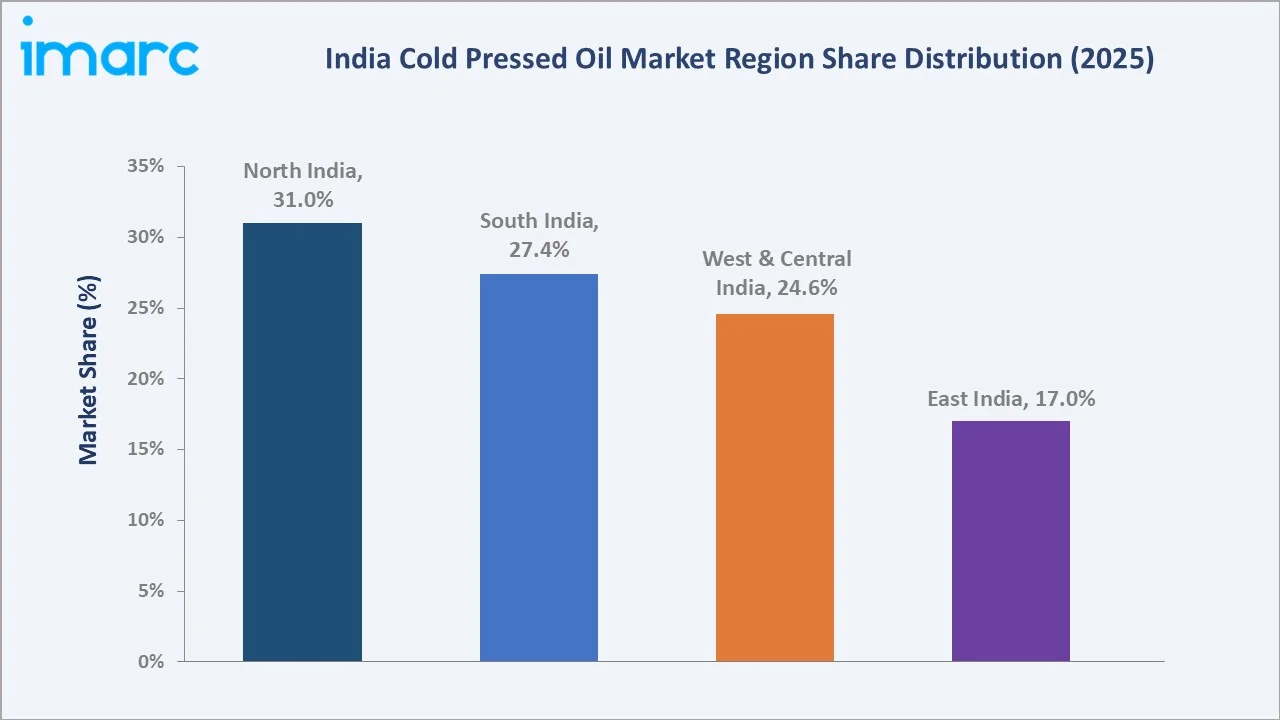

Core Oils dominate at 68.0%. Bottles lead packaging at 51.0%. North India commands 31.0% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 755.2 Million |

|

Forecast Market Size (2034) |

INR 1,213.8 Million |

|

CAGR (2026-2034) |

5.41% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Form |

Core Oils (68.0%, 2025) |

|

Dominant Packaging Type |

Bottles (51.0%, 2025) |

|

Leading Region |

North India (31.0%, 2025) |

The market expanded from INR 580.3 Million in 2020 to INR 755.2 Million in 2025, anchored at approximately INR 982.8 Million in 2030, and forecast to reach INR 1,213.8 Million by 2034. Rising disposable incomes enabling premium product adoption, Ayurvedic revival movements strengthening traditional oil demand, and digital commerce expanding cold pressed oil accessibility collectively sustain this growth trajectory.

To get more information on this market, Request Sample

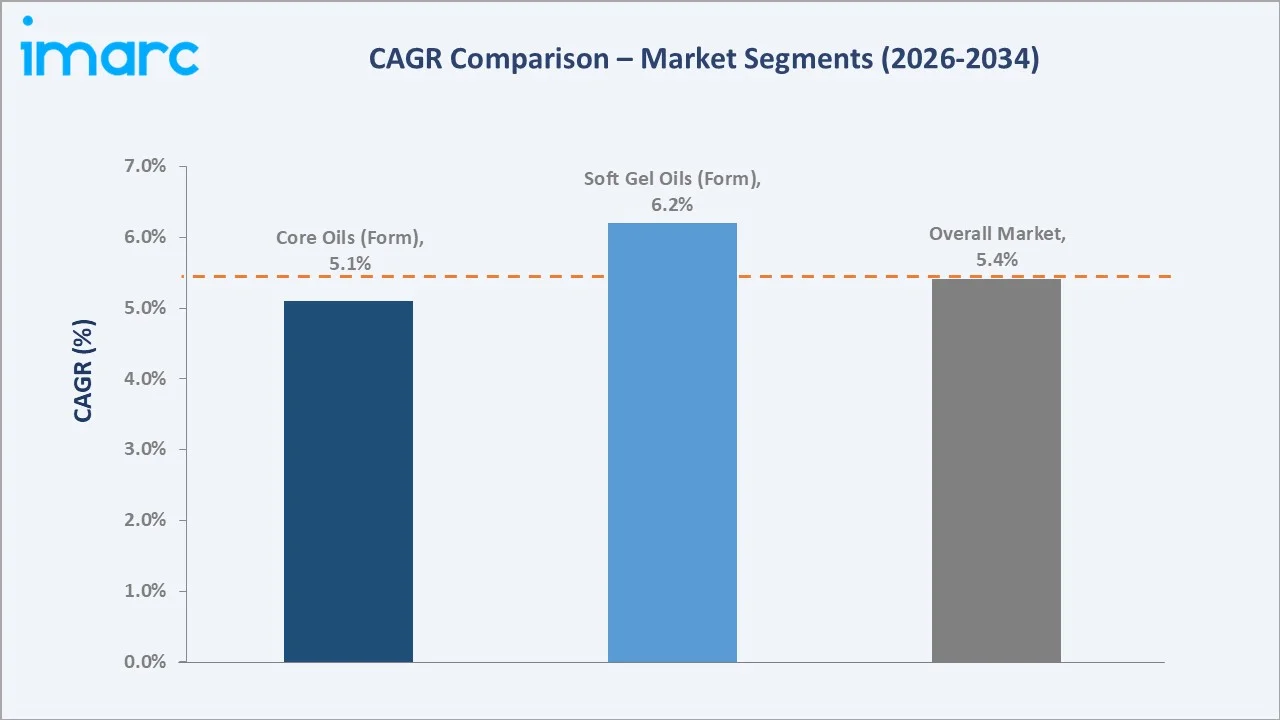

Core Oils grow steadily at approximately 5.1% CAGR supported by sustained culinary demand. Soft Gel Oils grow faster at approximately 6.2% CAGR through therapeutic supplementation channel expansion. Bottles lead packaging growth reflecting premiumization trends. North India maintains regional leadership while South India records the second-highest growth rate through expanding urban health consumer segments.

Executive Summary

The India cold pressed oil market reached INR 755.2 Million in 2025, representing one of India's fastest-growing wellness food segments. Cold pressed oils undergo mechanical extraction without chemical solvents or industrial heat, preserving heat-sensitive vitamins, antioxidants, and natural flavors critical to the premium positioning of this product category.

Core Oils at 68.0% dominate through widespread culinary application of mustard, groundnut, coconut, and sesame oils across India's diverse regional cuisines. Bottles at 51.0% lead packaging through strong consumer preference for transparent, tamper-evident containers enabling visual quality verification. North India at 31.0% leads regional demand through deep mustard oil cultural affinity and strong agricultural heritage.

The market is projected to reach INR 1,213.8 Million by 2034. Growth is anchored by expanding urban health-conscious consumer segments, rapid digital commerce penetration enabling premium DTC brand access, and Ayurvedic wellness mainstreaming reinforcing traditional cold pressed oil product associations.

Key Market Insights

|

Insight |

Data |

|

Dominant Form |

Core Oils – 68.0% share (2025) |

|

Dominant Packaging Type |

Bottles – 51.0% market share (2025) |

|

Leading Region |

North India – 31.0% market share (2025) |

|

Market Opportunity |

Premium heritage branding; Soft Gel therapeutic oil growth; organic certification adoption; e-commerce DTC channel expansion; Ayurvedic wellness positioning |

Key Analytical Observations Supporting The Above Data:

- Core Oils at 68.0%: The dominance of core oils reflects deep-rooted culinary traditions of mustard, groundnut, coconut, and sesame oils across Indian regional cuisines, creating structural household demand that transcends health trend cycles across all demographic segments.

- Bottles at 51.0%: Consumer preference for transparent, tamper-evident bottle containers enabling visual assessment of oil color, clarity, and quality drives packaging format dominance, particularly among premium and health-conscious urban purchasers in organized retail channels.

- North India at 31.0%: Punjab, Haryana, and Uttar Pradesh's deeply embedded mustard oil culinary traditions, combined with high agricultural oilseed production and growing urban premium consumer segments, create structural demand concentration in North India.

India Cold Pressed Oil Market Overview

The India cold pressed oil market encompasses the production, distribution, and retail of mechanically extracted oils from oilseeds and nuts processed without chemical solvents or high heat treatment. Primary product categories include mustard, groundnut, coconut, sesame, flaxseed, and kalonji core cooking oils, alongside soft gel therapeutic oil capsule formats targeting health supplementation needs.

The ecosystem integrates oilseed farmers, mechanical cold press equipment manufacturers, regional oil mill processors, FMCG corporations, Ayurvedic brands, packaging material suppliers, organized modern retail chains, e-commerce platforms, and health specialty distribution channels. Macroeconomic factors include rising disposable incomes, urbanization-driven health consciousness, Ayurvedic wellness mainstreaming, and government-supported organic agriculture expansion.

Market Dynamics

To evaluate market opportunities, Request Sample

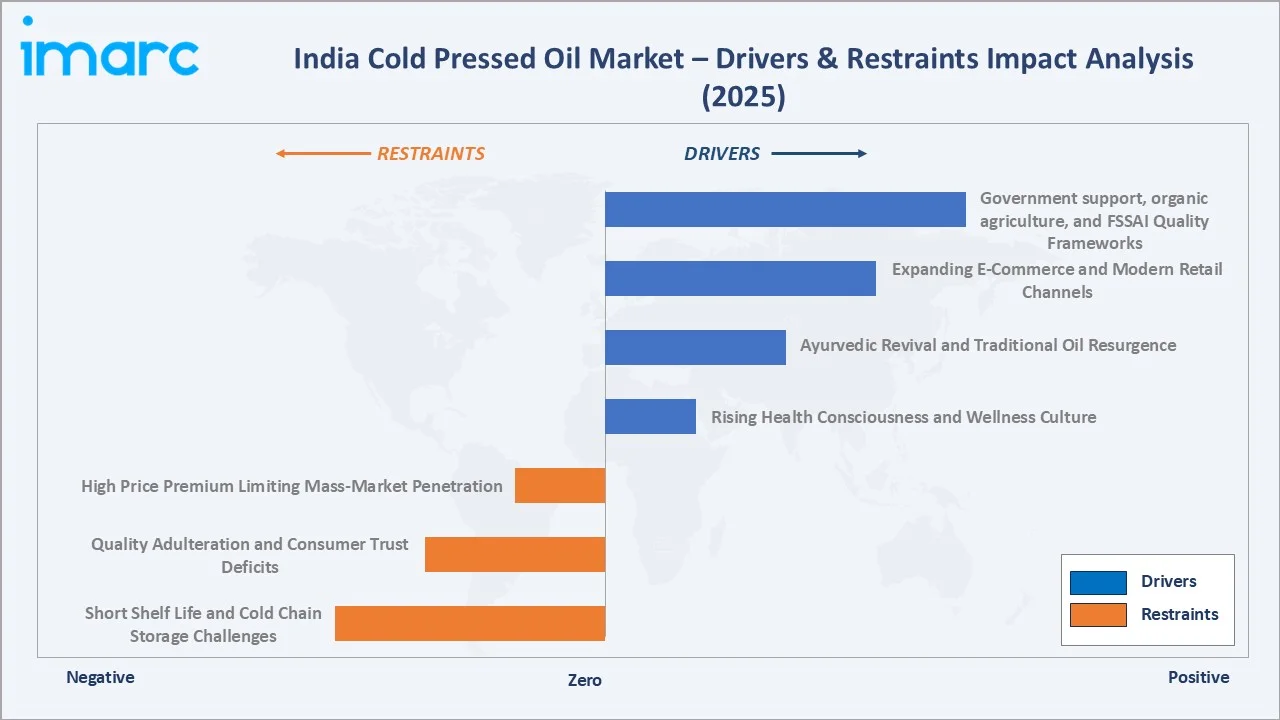

Market Drivers

- Rising Health Consciousness and Wellness Culture: India's urban and semi-urban consumers increasingly prioritize chemical-free, nutrient-dense food alternatives over refined counterparts. Cold pressed oils retaining essential fatty acids and antioxidants are gaining premium positioning as health foods, amplified by nutritionist endorsements, digital wellness media, and growing preventive healthcare awareness.

- Ayurvedic Revival and Traditional Oil Resurgence: India's Ayurvedic revival strongly endorses traditional cold pressed oils as holistic wellness ingredients across cooking, personal care, and therapeutic applications. Sesame, coconut, mustard, and kalonji oils carry deep Ayurvedic cultural associations, positioning cold pressed variants as premium health products gaining mainstream consumer adoption.

- Expanding E-Commerce and Modern Retail Channels: E-commerce platforms and modern trade chains have significantly expanded cold pressed oil accessibility beyond specialty health stores. Direct-to-consumer digital brands, hypermarket shelf expansion, quick-commerce delivery services, and subscription models are driving trial purchase rates among urban health-conscious consumers.

- Government Support, Organic Agriculture, and FSSAI Quality Frameworks: Government initiatives supporting organic farming, FSSAI quality labeling standards for cold pressed oils, and domestic agricultural processing promotion schemes are creating structured favourable market conditions, strengthening consumer confidence in cold pressed oil product authenticity claims.

Market Restraints

- High Price Premium Limiting Mass-Market Penetration: Cold pressed oils command 2–4x price premiums over refined alternatives due to lower extraction yields and mechanical processing costs. Price sensitivity across rural and semi-urban consumer segments remains a significant barrier, confining primary growth to premium urban demographics.

- Short Shelf Life and Cold Chain Storage Challenges: Absence of chemical preservatives reduces cold pressed oil shelf life versus refined alternatives. Supply chain temperature management complexity, shorter retail shelf life, and consumer storage education requirements increase distribution costs and limit geographic reach.

- Quality Adulteration and Consumer Trust Deficits: Market proliferation of products falsely claiming cold pressed origins creates consumer trust deficits. Absence of widespread third-party certification infrastructure and inconsistent regulatory enforcement enables quality misrepresentation, undermining authentic premium producer margins.

Market Opportunities

- Soft Gel Therapeutic Oil Segment Expansion: Flaxseed, fenugreek, kalonji, and black seed oils in soft gel capsule formats represent high-growth therapeutic product extensions addressing health-specific consumer needs across pharmacy and nutraceutical distribution channels with higher willingness-to-pay demographics.

- Premium Heritage and Single-Origin Branding: Regional provenance branding emphasizing specific agricultural origins, traditional extraction methods, and authentic cultural heritage creates powerful differentiation in crowded marketplaces, enabling superior price realization and defensible brand loyalty.

Market Challenges

- Fragmented Unorganized Sector Competitive Pressure: India's large unorganized cold pressed oil sector operates across thousands of small regional mills, producing lower-priced products that undercut organized sector premium brands with sustained pricing pressure particularly in rural and semi-urban geographies.

- Oilseed Supply Chain Volatility: Monsoon-dependent oilseed agriculture creates seasonal supply and pricing volatility for cold pressed oil processors, while procurement competition and price policy interventions create margin unpredictability complicating investment and production planning.

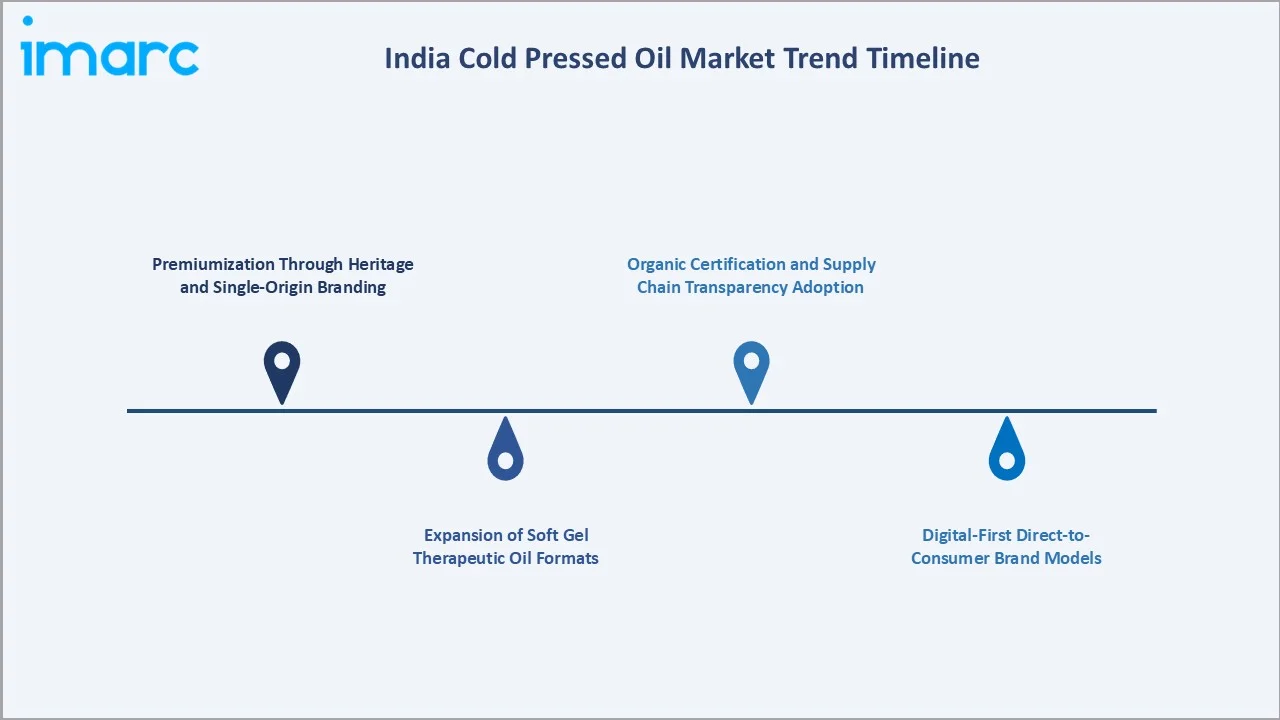

Emerging Market Trends

1. Premiumization Through Heritage and Single-Origin Branding

Manufacturers increasingly emphasize regional provenance, ancestral production methods, and single-origin oilseed sourcing to justify premium pricing strategies. Brands highlight traditional wooden churning techniques and family recipes passed through generations, creating differentiation in crowded marketplaces. Packaging incorporating vernacular languages and folk-art motifs transforms commodity oils into artisanal lifestyle products resonating with urban wellness consumers.

2. Expansion of Soft Gel Therapeutic Oil Formats

Therapeutic cold pressed oils in soft gel capsule formats are emerging as high-growth extensions beyond cooking applications. Flaxseed, kalonji, sesame, and fenugreek oil capsules target health-specific consumer needs and expand cold pressed oil distribution into pharmacy and nutraceutical channels, creating entirely new revenue streams with premium pricing and differentiated consumer demographics.

3. Digital-First Direct-to-Consumer Brand Models

Digitally native cold pressed oil brands are bypassing traditional retail through direct-to-consumer e-commerce, quick-commerce partnerships, and influencer-driven social media marketing. Subscription models, personalized oil selection tools, and social media content marketing create high-engagement acquisition strategies targeting urban millennial and Generation Z health-conscious consumers.

4. Organic Certification and Supply Chain Transparency Adoption

Blockchain-based supply chain traceability, QR-code origin verification, and third-party organic certification are emerging as competitive differentiators among premium cold pressed oil brands. Transparent sourcing documentation addresses consumer trust deficits around product authenticity and strengthens premium price justification narratives in organized retail channels.

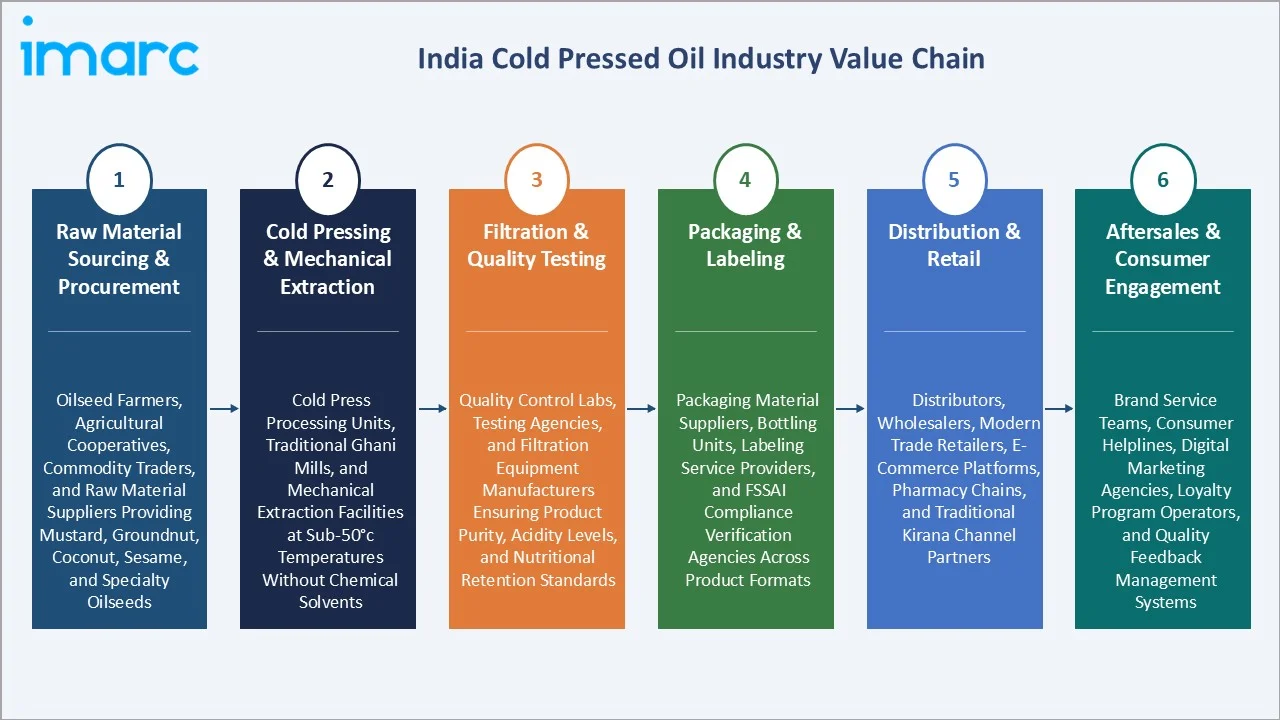

Industry Value Chain Analysis

The India cold pressed oil value chain integrates raw material procurement, mechanical cold pressing and extraction, filtration and quality testing, packaging and labeling operations, multi-channel distribution, and consumer engagement across organized modern trade, e-commerce, pharmacy, and traditional retail formats.

|

Stage |

Key Participants |

|

Raw Material Sourcing & Procurement |

Oilseed farmers, agricultural cooperatives, commodity traders, and raw material suppliers providing mustard, groundnut, coconut, sesame, and specialty oilseeds |

|

Cold Pressing & Mechanical Extraction |

Cold press processing units, traditional ghani mills, and mechanical extraction facilities operating at sub-50°C temperatures without chemical solvents |

|

Filtration & Quality Testing |

Quality control laboratories, testing agencies, and filtration equipment manufacturers ensuring product purity, acidity levels, and nutritional retention standards |

|

Packaging & Labeling |

Packaging material suppliers, bottling units, labeling service providers, and FSSAI compliance verification agencies across product formats |

|

Distribution & Retail |

Distributors, wholesalers, modern trade retailers, e-commerce platforms, pharmacy chains, and traditional kirana channel partners |

|

Aftersales & Consumer Engagement |

Brand service teams, consumer helplines, digital marketing agencies, loyalty program operators, and quality feedback management systems |

The cold pressing and extraction stage is the value chain's most quality-critical step, with extraction temperature and pressure management directly determining nutritional retention and product differentiation. The packaging selection stage significantly impacts consumer perceived quality, shelf-life performance, and brand positioning, making it a critical competitive lever for premium brand strategies.

Technology Landscape in the India Cold Pressed Oil Industry

Traditional Wooden Churning (Ghani) Technology

Traditional wooden churning technology uses bullock-driven or electric-powered wooden churns to cold press oilseeds at low rotational speeds and ambient temperatures. This method preserves cultural authenticity, natural flavors, and maximum nutritional integrity, commanding significant price premiums. Heritage ghani processing is a key brand differentiation asset for artisanal and premium segment producers.

Hydraulic Cold Press Technology

Hydraulic cold press machines apply controlled mechanical pressure to extract oils at temperatures consistently below 50°C without chemical solvent intervention. This technology enables scalable commercial production while maintaining cold pressed nutritional standards, serving mid-to-large, organized sector processors supplying modern trade chains and e-commerce platforms.

Advanced Centrifugal Filtration Technology

Centrifugal filtration systems enable efficient separation of cold pressed oil from press cake residue while preserving cold pressed product standards. Multi-stage filtration removes naturally occurring impurities and improves product clarity without chemical treatment, enabling consistent quality standards required for organized retail and premium e-commerce channel distribution.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Form |

Core Oils |

68.0% |

2025 |

|

Packaging Type |

Bottles |

51.0% |

2025 |

|

Pack Size |

1 Litre |

40.0% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

35.0% |

2025 |

|

Region |

North India |

31.0% |

2025 |

By Form

Core Oils lead at 68.0% (2025). Mustard, groundnut, coconut, and sesame oils command dominant market share through deep-rooted culinary traditions, widespread regional consumption patterns, and proven health benefit associations embedded across all Indian demographic segments. This segment provides the stable structural foundation of the India cold pressed oil market.

To access detailed market analysis, Request Sample

Soft Gel Oils at 32.0% represent the higher-growth emerging segment serving therapeutic and health supplementation applications across pharmacy and specialty health channels. Flaxseed, kalonji, fenugreek, and multi-seed soft gel oil formats are gaining significant traction among health-conscious consumers seeking preventive healthcare supplementation solutions.

By Packaging Type

Bottles lead at 51.0% (2025). Consumer preference for transparent, tamper-evident containers enabling visual quality verification of oil color and clarity drives bottle format dominance. Both glass and premium PET bottles reinforce artisanal and premium brand positioning strategies critical for organized modern retail channel and e-commerce premium segment success.

Cans at 20.6% serve bulk household and institutional buyers prioritizing product protection and extended storage. Pouches at 17.4% appeal to value-conscious consumers seeking affordable market entry points. Others at 11.0% encompasses sachets, jerry cans, and bulk dispensing formats serving specific foodservice and institutional procurement channels.

Regional Market Insights

|

Region |

Share (2025) |

Key India Cold Pressed Oil Market Drivers & Characteristics |

|

North India |

31.0% |

Driven by strong cultural affinity for traditional cooking oils, high agricultural oilseed production, and deeply embedded household consumption patterns across urban and rural segments |

|

South India |

27.4% |

Supported by high coconut and sesame oil consumption, strong Ayurvedic wellness adoption, and growing health-conscious urban consumer demand across major metropolitan areas |

|

West & Central India |

24.6% |

Driven by groundnut and sesame oil consumption traditions, expanding urban premium product demand, and growing modern trade infrastructure in Tier 2 cities |

|

East India |

17.0% |

Growing through traditional oil consumption heritage and rising health awareness among younger urban consumer segments across the region |

North India, at 31.0%, commands market leadership through strong traditional oil consumption heritage and high agricultural oilseed production. The region's well-established cold pressed oil awareness and extensive distribution networks across organized and traditional retail channels further reinforce its dominant market position.

South India, at 27.4%, is driven by strong coconut and sesame oil heritage and rapidly expanding health-conscious urban consumer demand. West and Central India at 24.6% reflects groundnut oil dominance and growing urban premium consumption. East India at 17.0% grows through traditional mustard oil heritage and rising health awareness among younger urban consumer segments.

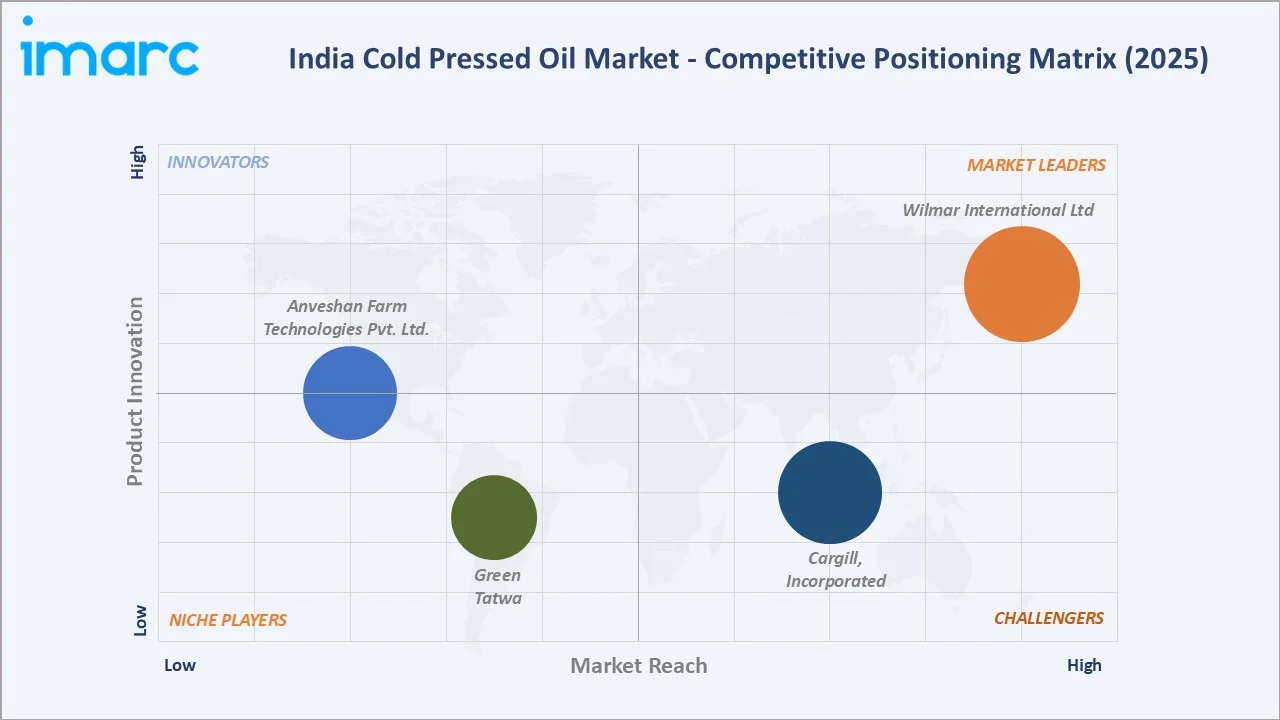

Competitive Landscape

The India cold pressed oil market features a blend of large FMCG corporations, Ayurvedic wellness brands, and regional specialty processors. Large, organized sector players compete on distribution scale and brand equity, while artisanal and heritage brands differentiate through provenance authenticity and premium positioning.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Wilmar International Ltd |

Fortune Premio Cold Press Mustard Oil |

Market Leader |

AWL Agri Business Ltd., part of Wilmar International Ltd leverages Fortune brand for large-scale cold pressed oil distribution across modern trade and e-commerce channels nationally. |

|

Cargill, Incorporated |

NatureFresh Premium Kachi Ghani Mustard Oil |

Strong Challenger |

Cargill India Pvt. Ltd. targets premium segments through its Nature Fresh brand, emphasizing purity and nutritional retention in cold pressed oils. |

|

Anveshan Farm Technologies Pvt. Ltd. |

Cold-Pressed Almond Oil |

Emerging Player |

Anveshan Farm Technologies Pvt. Ltd. is a growth-stage D2C food-tech startup offering traditional kolhu-pressed cold pressed oils, A2 ghee, and superfoods |

|

Green Tatwa |

Groundnut Oil, Coconut Oil, Sunflower Oil |

Niche Player |

Greentatwa Agri Tech LLP is a Hyderabad-based trader and wholesaler-distributor of cold pressed oils and agricultural products |

Key players include Wilmar International Ltd, Cargill, Incorporated, Anveshan Farm Technologies Pvt. Ltd., and Green Tatwa, among others.

Key Company Profiles

Wilmar International Ltd

Wilmar International Ltd. is a Singapore-based agribusiness conglomerate and the majority shareholder of AWL Agri Business Ltd., which operates the Fortune brand in India. Through AWL Agri Business, Wilmar International holds a dominant position in India's cold pressed oil segment.

- Key Products: Fortune Premio Cold Press Mustard Oil

- Strategic Focus: Strengthening presence in the high-value premium oils segment through Fortune Premio while expanding branded exports and scaling the HoReCa channel in India.

Cargill, Incorporated

Cargill, Incorporated is a US-based multinational food and agricultural commodities corporation operating in India. The company processes, refines, and markets a wide range of indigenous and imported edible oils and fats, with its brands NatureFresh, Gemini, Sweekar, Leonardo Olive Oil, Rath, and Sunflower.

- Key Products: NatureFresh Premium Kachi Ghani Mustard Oil

- Strategic Focus: Leveraging NatureFresh brand equity and Cargill India's three vegetable oil refineries located at Paradeep, Kandla, and Kurkumbh to scale cold pressed oil distribution across organized retail and e-commerce channels, targeting premium health-focused consumer segments nationwide.

Market Concentration Analysis

The India cold pressed oil market exhibits moderate concentration at the organized sector level, with large FMCG players holding meaningful distribution and brand recognition advantages. However, the overall market remains structurally fragmented due to India's large unorganized cold pressing sector operating thousands of small regional mills.

Organized sector players are progressively increasing market share through brand investments, modern retail shelf expansion, and e-commerce channel development. The premium segment demonstrates higher concentration among established brands, while value segments remain intensely competitive with significant unorganized sector pricing pressure across rural and semi-urban geographies.

Investment & Growth Opportunities

Highest Growth Segments

Soft Gel therapeutic oils (approximately 6.2% CAGR), premium single-origin heritage core oils, organic certified product variants, e-commerce direct-to-consumer brands, South India coconut oil premium segment, and Ayurvedic-positioned wellness oil formats represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Blockchain-enabled supply chain transparency platforms for verified cold pressed oil origin authentication represent high-value investment opportunities. Companies investing in traceable single-origin sourcing infrastructure and third-party organic certification can command significant premium pricing and sustainable brand differentiation in premium urban consumer segments.

Investment Themes

- Premium heritage DTC brand development for e-commerce and quick-commerce channels: Building authentic regional provenance brands through social media and direct-to-consumer channels requires lower capital intensity than traditional modern trade but achieves superior per-unit margins through direct consumer relationships and premium positioning.

- Soft gel therapeutic oil product range expansion into pharmacy and nutraceutical channels: Extending cold pressed oil portfolios into pharmacy distribution through soft gel therapeutic formats addresses consumer segments with significantly higher willingness-to-pay and lower price sensitivity than culinary categories, offering premium margin profiles.

Future Market Outlook (2026-2034)

The India cold pressed oil market is projected to grow from INR 755.2 Million in 2025 to INR 1,213.8 Million by 2034, delivering a 5.41% CAGR over the forecast period. The market's anchor value of INR 982.8 Million in 2030 represents an industry shaped by three concurrent demand forces: rising health consciousness driving premiumization, Ayurvedic revival reinforcing traditional product demand, and digital commerce democratizing premium brand access.

Three structural forces define India cold pressed oil market growth through 2034 with strong confidence. Rising health awareness and preventive nutrition adoption among India's expanding urban middle class creates sustained premium product demand resistant to short-term economic variability. Digital commerce expansion democratizes premium product access beyond major metropolitan centers. Government support for domestic oilseed processing value addition provides a consistently favorable policy environment for organized sector growth.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders including oilseed procurement managers, cold pressed oil processing unit directors, FMCG brand managers, modern trade category managers, e-commerce wellness platform category leads, Ayurvedic health practitioners, and regional cold pressed oil distributor principals across India.

Secondary Research

Secondary research encompassed FSSAI regulatory publications, APEDA agricultural processing data, Solvent Extractors Association of India statistics, company annual reports, e-commerce platform wellness product trend analyses, Ayurveda industry association reports, and over 55 secondary sources covering India edible oil market dynamics.

Forecasting Models

Market revenue forecasts developed using segmentation-based bottom-up models incorporating form segment growth drivers, packaging type penetration trends, regional consumption data, organized versus unorganized sector share evolution estimates, and e-commerce channel growth trajectory projections across India's consumer market through 2034.

India Cold Pressed Oil Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Million |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Forms Covered |

|

| Packaging Types Covered | Bottles, Cans, Pouches, Others |

| Pack Sizes Covered | 1 Litre, 5 Litres, 500 mL, Others |

| Distribution Channels Covered | Convenience Stores, Supermarkets and Hypermarkets, Online Stores, Others |

| Regions Covered | North India, South India, West & Central India, East India |

| States Covered | Delhi NCR, Uttar Pradesh, Punjab, Rajasthan, Haryana, Tamil Nadu, Karnataka, Kerala, Maharashtra, Gujarat, Madhya Pradesh, West Bengal, Bihar, Jharkhand, Others |

| Companies Covered | Wilmar International Ltd, Cargill, Incorporated, Anveshan Farm Technologies Pvt. Ltd., Green Tatwa, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Cold Pressed Oil Market Report

The India cold pressed oil market reached INR 755.2 Million in 2025, driven by Core Oils at 68.0% through culinary traditions, Bottles at 51.0% through consumer packaging preferences, and North India at 31.0% through deep traditional oil consumption heritage and strong regional agricultural oilseed production.

The market grows at 5.41% CAGR during 2026-2034, reaching INR 1,213.8 Million by 2034. This reflects rising health awareness, Ayurvedic wellness mainstreaming, premium product adoption across urban demographics, and rapid e-commerce channel expansion enabling premium brand accessibility.

Core Oils lead at 68.0% through widespread culinary applications deeply embedded in India's diverse regional cooking traditions. Soft Gel Oils at 32.0% represent the faster-growing therapeutic supplement segment targeting health-specific consumer needs across pharmacy and nutraceutical channels.

Bottles lead at 51.0% through consumer preference for transparent, tamper-evident containers enabling visual quality verification. Cans at 20.6% serve bulk buyers. Pouches at 17.4% target value-conscious consumers. Others at 11.0% covers sachets and bulk formats for institutional channels.

North India leads at 31.0% through deep traditional oil consumption heritage and strong agricultural oilseed production. South India at 27.4% follows through coconut and sesame oil heritage and growing health-conscious urban consumer demand.

Leading companies include Wilmar International Ltd, Cargill, Incorporated, Anveshan Farm Technologies Pvt. Ltd., and Green Tatwa, among others.

The market is projected to reach approximately INR 982.8 Million by 2030, driven by continued health consciousness growth, e-commerce channel expansion, organic certification adoption, and premium heritage branding strategy maturation across organized retail formats.

Three priority opportunities: premium heritage DTC brand development via e-commerce and social commerce channels; soft gel therapeutic oil range expansion targeting pharmacy and nutraceutical distribution; and blockchain supply chain transparency platform investment enabling verified origin authentication and premium pricing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)