Global Hydrographic Survey Equipment Market Expected to Reach USD 4.9 Billion by 2033 - IMARC Group

Global Hydrographic Survey Equipment Market Statistics, Outlook and Regional Analysis 2025-2033

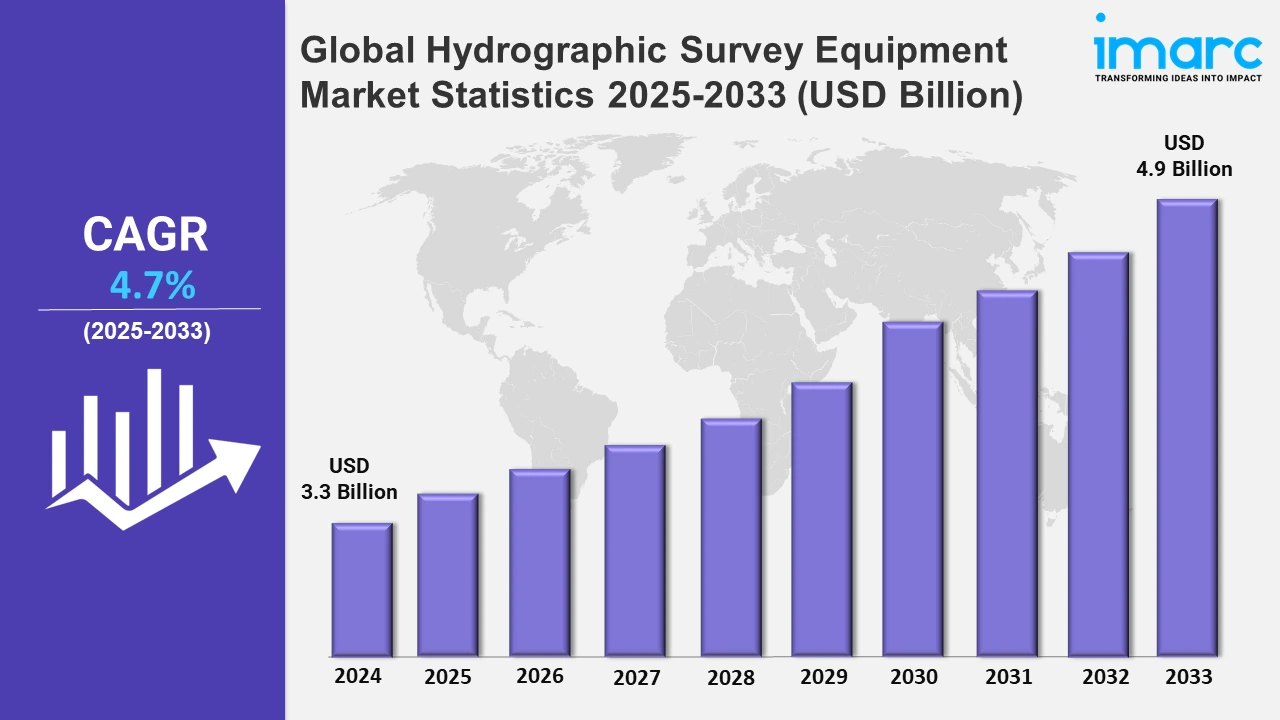

The global hydrographic survey equipment market size was valued at USD 3.3 Billion in 2024, and it is expected to reach USD 4.9 Billion by 2033, exhibiting a growth rate (CAGR) of 4.7% from 2025 to 2033.

To get more information on this market, Request Sample

The hydrographic survey equipment market is experiencing significant advancements driven by the integration of cutting-edge technologies and the rising demand for efficient data collection tools. Increasing maritime activities, along with the need for precise underwater mapping, are driving innovation in this domain. In line with this, key players are investing in advanced equipment to enhance survey accuracy and operational efficiency. For instance, in March 2024, BRIX Marine launched the 3011-CTC survey vessel, Lugudi Barana. This state-of-the-art vessel features advanced hydrographic survey equipment, including a hydraulic winch, "T" transom A-frame, and precise deployment systems. These advancements enable superior data collection, thereby enhancing operational workflows for maritime applications. At the same time, EIVA introduced a containerized remotely operated towed vehicle (ROTV) hydrographic survey solution for the UK Ministry of Defence in August 2024. This system integrates the ScanFish L ROTV, Sonardyne’s SPRINT-Nav Mini, and Voyis’ Observer Pro, offering rapid deployment and advanced data analysis. This agile solution reflects the increasing demand for modular and easily deployable survey systems tailored for diverse marine environments.

Moreover, the growing emphasis on national defense and strategic maritime capabilities is positively impacting the market. The commissioning of INS Sandhayak by the Indian Navy in February 2024 highlights this trend. The vessel represents a leap in hydrographic survey technology equipped with Kongsberg HUGIN AUV, multi-beam echo-sounders, side-scan sonars, remotely operated vehicles (ROVs), and advanced data acquisition systems. This enhances capabilities in ports, harbors, and deep-sea navigation, setting new benchmarks in underwater exploration and maritime safety. Furthermore, these technological strides, coupled with the increasing investments in R&D activities and the rising maritime operations, are reshaping the market, thereby offering immense growth opportunities globally.

Global Hydrographic Survey Equipment Market Statistics, By Region

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America dominates the hydrographic survey equipment market due to the region's substantial investment in maritime safety, navigation, and environmental monitoring.

North America Hydrographic Survey Equipment Market Trends:

North America is leading in the market, driven by advanced technologies, such as bathymetric equipment, multi-beam echo-sounders, and sonar systems, which are widely adopted, owing to government initiatives. In March 2024, NOAA began its hydrographic survey season, deploying these advanced tools across U.S. coastal regions. This initiative enhances nautical charting, hazard identification, and ecosystem studies. Moreover, the demand for accurate seafloor mapping for maritime trade, coastal development, and environmental conservation solidifies North America's leadership in the hydrographic survey equipment sector.

Europe Hydrographic Survey Equipment Market Trends:

In Europe, the market is growing due to advancements in ocean mapping for offshore wind projects. Countries like Norway are leveraging advanced sonar systems for seabed surveys in wind farm construction. Besides this, increased investments in port expansions and maritime safety in the UK and Germany drive demand. Also, the adoption of autonomous survey vessels highlights Europe's focus on modernizing its maritime operations.

Asia-Pacific Hydrographic Survey Equipment Market Trends:

Asia-Pacific sees rapid growth in the hydrographic survey equipment market due to rising offshore oil and gas exploration in nations like India. Furthermore, technological advancements, such as multi-beam echo sounders, are aiding detailed seabed mapping. Coastal infrastructure projects in Japan and China further fuel demand, ensuring accurate marine data for port developments. Meanwhile, increased focus on disaster management in this region also boosts equipment adoption.

Latin America Hydrographic Survey Equipment Market Trends:

In Latin America, the market is driven by offshore energy projects in Brazil, and the exploration of pre-salt oil reserves necessitates high-precision survey systems like side-scan sonars. In line with this, governments are focusing on improving maritime safety for fishing and cargo routes. Moreover, Chile's investments in hydrographic research for coastal ecosystem management highlight growing environmental applications in the region.

Middle East and Africa Hydrographic Survey Equipment Market Trends:

The Middle East and Africa market expands with increased offshore drilling and port infrastructure projects, especially in Saudi Arabia. In contrast, demand for bathymetric survey tools is rising due to Red Sea port developments. Furthermore, African nations like South Africa are employing advanced equipment for marine conservation projects. Enhanced maritime trade routes and security needs also push the adoption of cutting-edge survey technologies.

Top Companies Leading in the Hydrographic Survey Equipment Industry

Some of the leading hydrographic survey equipment market companies include EdgeTech, Innomar Technologie GmbH, iXblue SAS, Kongsberg Gruppen ASA, Raytheon Technologies Corporation, Sonardyne International Ltd., SyQwest Incorporated, Teledyne Technologies Inc., Topcon Corporation, Tritech International Limited (Moog Inc.), and Valeport Ltd., among many others. In March 2024, Kongsberg launched the Seapath 385 navigation system, integrating GNSS signals and advanced inertial sensors for hydrographic surveys. It sets a new benchmark in precision navigation for demanding hydrographic survey applications globally, offering centimeter-level accuracy, enhanced algorithms, and modular design.

Global Hydrographic Survey Equipment Market Segmentation Coverage

- On the basis of the type, the market has been bifurcated into sensing systems, positioning systems, subsea sensors, software, unmanned vehicles, and others, wherein unmanned vehicles represent the most preferred segment. It enhances hydrographic surveys by providing precise data collection in remote or hazardous areas, thereby increasing efficiency and safety for mapping underwater environments.

- Based on the depth, the market is categorized into shallow water and deep water, amongst which shallow water dominates the market. It ensures accurate depth measurement, sediment analysis, and navigational charting, essential for ports, coastal management, and habitat preservation.

- On the basis of the platform, the market has been divided into surface vessels, USVs and UUVs, and aircraft. Among these, USVs and UUVs exhibit a clear dominance in the market. They revolutionize hydrographic surveys, enabling autonomous, high-resolution data acquisition in challenging marine environments for research, defense, and commercial applications.

- Based on the application, the market is bifurcated into hydrographic or bathymetry survey, port and harbor management, offshore oil and gas survey, cable or pipeline route survey, and others, wherein offshore oil and gas survey dominates the market. Hydrographic survey equipment supports offshore oil and gas projects by mapping seabeds, identifying pipeline routes, and assessing environmental conditions, thereby ensuring safe and efficient operations.

- On the basis of the end use, the market is segmented into commercial, research, and defense. Currently, commercial accounts for the majority of the total market share. Commercial sectors leverage hydrographic survey equipment for port development, resource exploration, and maritime navigation, which is fostering economic growth through underwater mapping and analysis.

| Report Features | Details |

|---|---|

| Market Size in 2024 | USD 3.3 Billion |

| Market Forecast in 2033 | USD 4.9 Billion |

| Market Growth Rate 2025-2033 | 4.7% |

| Units | Billion USD |

| Segment Coverage | Type, Depth, Platform, Application, End Use, Region |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | EdgeTech, Innomar Technologie GmbH, iXblue SAS, Kongsberg Gruppen ASA, Raytheon Technologies Corporation, Sonardyne International Ltd., SyQwest Incorporated, Teledyne Technologies Inc., Topcon Corporation, Tritech International Limited (Moog Inc.), Valeport Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)