Global Heat Exchanger Market Expected to Reach USD 30.8 Billion by 2033 - IMARC Group

Global Heat Exchanger Market Statistics, Outlook and Regional Analysis 2025-2033

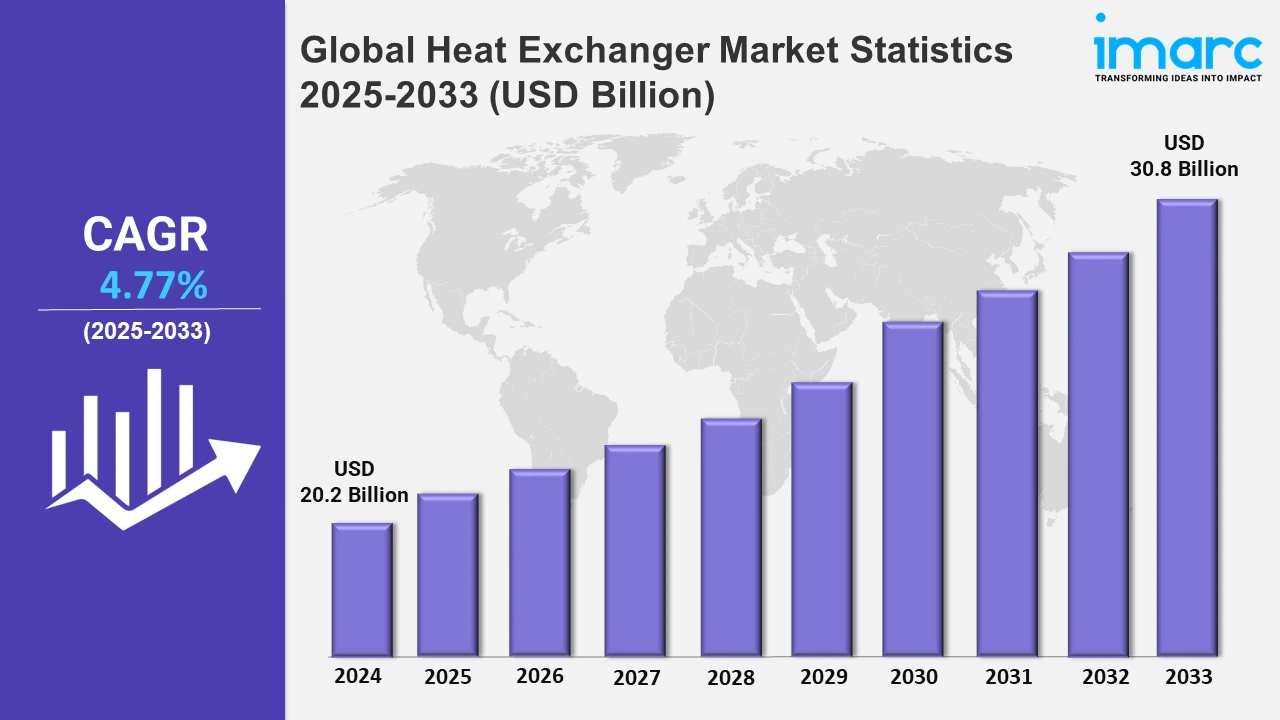

The global heat exchanger market size was valued at USD 20.2 Billion in 2024, and it is expected to reach USD 30.8 Billion by 2033, exhibiting a growth rate (CAGR) of 4.77% from 2025 to 2033.

To get more information on this market, Request Sample

The growth of the global heat exchanger market is driven by several factors, including increasing energy efficiency demands, expanding industrial applications, and the integration of advanced technologies. As industries such as chemical processing, power generation, and heating, ventilation, and air conditioning (HVAC) systems expand globally, heat exchangers are vital for optimizing energy transfer and reducing operational costs. In addition to this, stringent government regulations promoting energy efficiency and sustainability have spurred the adoption of advanced heat exchangers in industries like oil and gas, where waste heat recovery is critical, thereby strengthening the market growth. For instance, the European Union’s initiatives on green energy significantly contribute to regional demand for high-performance systems. Moreover, with new energy-efficient systems being launched in the market, like Variable Refrigerant Flow (VRF) technologies, the gains are 30% or more in energy savings, which are also supported by government regulations in terms of efficiency, like updated Seasonal Energy Efficiency Ratio 2 (SEER 2) standards that started in 2023.

The industry is also being transformed by the continuous development of microchannel and the Internet of Things (IoT) enabled heat exchangers. These technologies offer increased efficiency in heat transfer, predictive maintenance, and less downtime, making them critical for industries with high-performance standards. The Asia-Pacific region, especially China and India, has experienced rapid industrialization and infrastructure development, creating huge opportunities, with government policies that focus on energy optimization. Meanwhile, North America and Europe, maintain strong market positions, respectively, supported by well-developed industry areas and strong frameworks of regulatory guidelines. Manufacturers also increasingly focus on advanced alloys of stainless steel and aluminum to construct sturdier exchangers with higher performance. Another significant factor acting as a growth inducer is the integration of heat exchangers with renewable energy systems like geothermal and solar thermal plants that align with the transition to clean energy sources worldwide.

Global Heat Exchanger Market Statistics, By Region

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, Argentina, Colombia, Chile, Peru, and others); and the Middle East and Africa (Turkey, Saudi Arabia, Iran, United Arab Emirates, and others). According to the report, Europe accounted for the largest market share, primarily attributed to green energy initiatives emphasizing the adoption of sustainable technologies and stringent energy efficiency regulations in driving industrial upgrades.

North America Heat Exchanger Market Trends:

Growing investments in energy infrastructures, combined with adoption of cutting-edge manufacturing techniques, is increasing the usage of heat exchangers in North America. Improvements in energy recovery systems mainly within U.S. shale gas-based oil and gas refineries have increased usage. Both regions are supportive through governments incentives along with corporate sustainability that focus on maintaining energy-efficient HVAC systems.

Asia-Pacific Heat Exchanger Market Trends:

Rapid industrialization and urbanization in the countries, among which China, India, and Southeast Asia, increase the need for heat exchangers in the Asia-Pacific region. Besides the above-mentioned sectors, booming chemical, petrochemical, and food processing industries have had a great influence on demand increases, while government-led initiatives for greening and investments for infrastructure upgradation support market growth further.

Europe Heat Exchanger Market Trends:

New renewable energy technologies and the growing use of district heating are among the key drivers of European demand for heat exchangers. For instance, in Germany, an energy transition involves the conversion of waste heat into electricity with highly efficient heat exchangers that increase electricity consumption by 35%. The use of 3D-printed heat exchangers also boosts efficiency and supports sustainability in aerospace and automotive. Projects such as Bremen's Uberseeinsel energy plant show that the market is witnessing robust growth through the integration of heat exchangers and river-based heating systems.

Latin America Heat Exchanger Market Trends:

Increased focus on industrial diversification and energy optimization is driving demand for heat exchangers in Latin America. Leading drivers include Brazil's ethanol production, increasing investments in renewable energy, industrial expansion in Argentina and Mexico, and efforts to improve efficiency in power generation.

Middle East and Africa Heat Exchanger Market Trends:

The demand for heat exchangers in the Middle East and Africa is fueled by large-scale oil and gas projects as well as water desalination initiatives. Regional diversification of energy resources, which incorporates solar thermal as well as geothermal energy systems, will spur demand for high-performance heat exchangers. Urban development and industrial growth spur demand.

Top Companies Leading in the Heat Exchanger Industry

Some of the leading heat exchanger market companies include Alfa Laval AB, API Heat Transfer, Boyd, Chart Industries, Danfoss, GE Vernova, GEA Group Aktiengesellschaft, Hisaka Works, Ltd., IHI Plant Services Corporation, Johnson Controls, Kelvion Holding GmbH, Mersen, Modine Manufacturing Company, SPX FLOW, Inc., Xylem, among many others.

- February 2024: Danfoss India launched its Microchannel Heat Exchanger (MCHE) technology at the ACREX India 2024 exhibition. With its innovative Next Gen Evaporator, this energy-efficient invention revolutionizes air-cooled units, outperforming standard fin tube heat exchangers.

Global Heat Exchanger Market Segmentation Coverage

- On the basis of the type, the market has been categorized into shell and tube, plate and frame, air cooled, and others, wherein shell and tube represent the leading segment. Shell and tube heat exchangers are predominant because of their robust design, high thermal efficiency, and suitability at extreme temperatures and pressures. These exchangers have a large application in the power generation, oil, gas, and chemical industries, providing economic scalability to large applications. Furthermore, the versatility of dealing with diverse fluids makes them dominant in the market.

- Based on the material, the market is classified into carbon steel, stainless steel, nickel, and others, amongst which stainless steel dominates the market. Material-wise, stainless steel is dominating the industry with excellent corrosion resistance and toughness along with high-temperature and high-pressure operability. For pharmaceuticals, food processing, and chemicals, the hygiene and long service life make this the best material to use. With global sustainability, stainless steel's recyclability further makes it desirable for use across all applications.

- On the basis of the end use industry, the market has been divided into chemical, petrochemical and oil & gas, HVAC and refrigeration, food and beverage, power generation, paper and pulp, and others. Among these, chemical account for the majority of the market share. The chemical industry dominates the market for heat exchangers because of the high energy-intensive processes requiring precise temperature regulation. Heat exchangers are used in distillation, condensation, and reaction cooling operations. Increasing investments in chemical manufacturing in emerging economies and stringent safety standards further boost their deployment in this sector.

| Report Features | Details |

|---|---|

| Market Size in 2024 | USD 20.2 Billion |

| Market Forecast in 2033 | USD 30.8 Billion |

| Market Growth Rate 2025-2033 | 4.77% |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Shell and Tube, Plate and Frame, Air Cooled, Others |

| Materials Covered | Carbon Steel, Stainless Steel, Nickel, Others |

| End-Use Industries Covered | Chemical, Petrochemical and Oil & Gas, HVAC and Refrigeration, Food and Beverage, Power Generation, Paper and Pulp, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | Alfa Laval AB, API Heat Transfer, Boyd, Chart Industries, Danfoss, GE Vernova, GEA Group Aktiengesellschaft, Hisaka Works, Ltd., IHI Plant Services Corporation, Johnson Controls, Kelvion Holding GmbH, Mersen, Modine Manufacturing Company, SPX FLOW, Inc., Xylem, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Browse IMARC Related Reports on Heat Exchanger Market:

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)