Global Compound Semiconductor Market Expected to Reach USD 177.0 Billion by 2033 - IMARC Group

Global Compound Semiconductor Market Statistics, Outlook and Regional Analysis 2025-2033

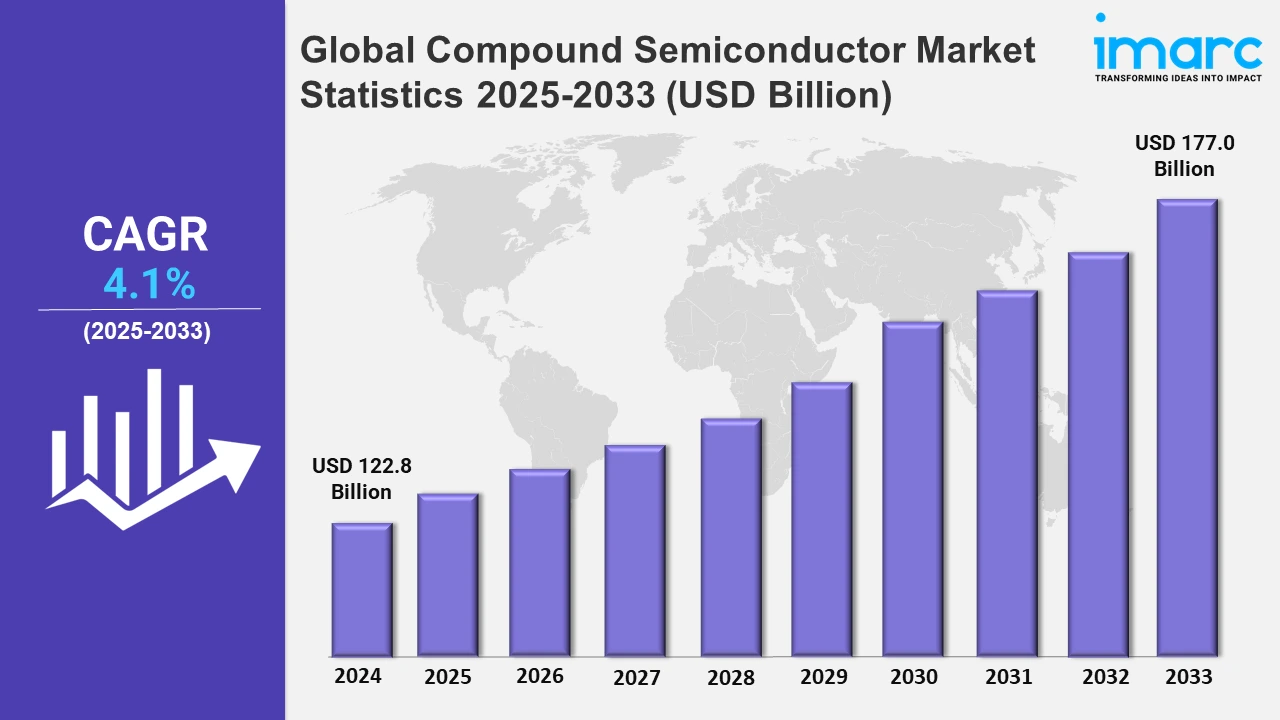

The global compound semiconductor market size was valued at USD 122.8 Billion in 2024, and it is expected to reach USD 177.0 Billion by 2033, exhibiting a growth rate (CAGR) of 4.1% from 2025 to 2033.

To get more information on this market, Request Sample

The global compound semiconductor market is experiencing robust growth driven by the increasing demand for high-performance electronic devices in numerous end-use industries, including telecommunications, automotive, and consumer electronics. Along with this, the rapid adoption of 5G technology, which requires advanced semiconductors for efficient power management and high-frequency operations, is significantly supporting the market. According to a research report by IMARC Group, the global 5G services market size reached USD 128.1 Billion in 2023. The market is expected to reach USD 3,431.8 Billion by 2032, exhibiting a growth rate (CAGR) of 44.1% during 2024-2032. In addition to this, the rising popularity of compound semiconductors, such as gallium nitride (GaN) and silicon carbide (SiC) for their superior thermal stability, energy efficiency, and performance under extreme conditions is also propelling the market growth. Additionally, the growing penetration of electric vehicles (EVs) is escalating demand for compound semiconductors in power electronics to facilitate faster charging, longer battery life, and enhanced reliability. On 7th May 2024, Infineon announced that it will supply its SiC power modules HybridPACK Drive G2 CoolSiC, and bare die products to Xiaomi EV for its recently announced SU7 until 2027. Infineon will be supplying two HybridPACK Drive G2 CoolSiC 1200 V modules for the Xiaomi SU7 Max. Infineon also supplies Xiaomi EV with a large portfolio of other products per car, including EiceDRIVER gate drivers, and more than ten microcontrollers in different applications. Moreover, considerable rise in the adoption of the Internet of Things (IoT) and smart devices is augmenting the need for semiconductors with high power density and efficient signal transmission capabilities, emphasizing their critical role in modern technology.

Furthermore, the increasing utilization of compound semiconductors in renewable energy sources, especially in photovoltaic and wind energy is driving the market forward. These materials are core for power inverters and converters, which increase efficiency as well as reliability of energy generation in renewable energy systems. Increasing government investments and incentives in renewable energy projects worldwide are accelerating the adoption of these semiconductors. As per a Press Trust of India (PTI) report, India will witness more than 83% of the rise in investments in renewable energy projects to around USD 16.5 billion in 2024, with the country focusing on energy transition to reduce carbon emissions. This spike reflects the country's commitment to energy transition and reducing carbon emissions, as outlined by the power ministry. This is in line with India's ambitious target of having 500 GW of renewable energy by 2030 and its resolve to reduce overall power generation capacity from fossil fuels to less than 50%. India has committed to a net zero emission target by 2070. Apart from this, process improvement in manufacturing provides compound semiconductors that are more economical and can be deployed widely across industries. Markets for defense and aerospace further propel growth through deployment in radar systems, satellite communication, and advanced sensors. With increased awareness regarding sustainability and energy savings coupled with continual innovations, the market is witnessing significant expansion.

Global Compound Semiconductor Market Statistics, By Region

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific accounted for the largest market share on account of rapid 5G adoption, growing electric vehicle demand, and a growing consumer electronics sector, supported by a strong manufacturing base.

Asia-Pacific Compound Semiconductor Market Trends:

Asia Pacific leads the market due to its strong industrial base, latest technological advancements, and high demand from key end-user industries. Major players in the region include Chinese, Japanese, South Korean, and Taiwanese semiconductor manufacturers that maintain high levels of innovation and production capacity. The rapid adoption of 5G technology, along with increasing investments in electric vehicles and widespread IoT devices' deployment, are fueling growth within the market in this region. Also, the industry retains a leading due to the growing consumer electronics market and the strong supply chain of the region. On August 14, 2024, the Asia-Pacific F5.5G All-Optical Summit was successfully hosted in Bangkok, themed "F5.5G All-Optical Access, Premium Transmission for Intelligence," attracting over 200 customers and partners from around Asia and the Pacific to share a glimpse of network technology innovation in all-optical network industries in the Asia-Pacific region. On the sidelines of the summit, Huawei launched F5.5G "All-Optical Access + Premium Transmission" network solution to lead intelligence transformation and grow a digital economy in the Asia-Pacific region. Moreover, supportive government initiatives are promoting the adoption of renewable energy and bolstering semiconductor manufacturing, further strengthening Asia-Pacific’s position as the leading regional market.

North America Compound Semiconductor Market Trends:

North America leads in compound semiconductor innovations, largely based on strong demand from defense and aerospace as well as telecommunication sectors. The massive pace of 5G and IoT ecosystems expansion creates huge opportunities in high-performance semiconductors. Significant investments in renewable energy technologies combined with a strong consumer electronics market continue to drive the steady growth of the region.

Europe Compound Semiconductor Market Trends:

Compound semiconductors in Europe are driven by automotive technologies, including electric vehicles and autonomous systems. The region has robust research and development initiatives and government policies favoring clean energy and sustainable technology. Increasing adoption of 5G infrastructure and industrial IoT further accelerates demand, making Europe an important market across the globe.

Latin America Compound Semiconductor Market Trends:

With growing renewable energy projects and smart infrastructure initiatives in Latin America, the compound semiconductor market is increasing. An increased penetration of IoT technology, further growth in communication networks, also enhance the market in Latin America. Government policies encouraging clean energy and technological advancement are gradually integrating the region into the global semiconductor supply chain.

Middle East and Africa Compound Semiconductor Market Trends:

The Middle East and Africa market for compound semiconductors is being driven by increasing investment in renewable energy and telecom infrastructure. Urbanization, and smart city projects are further creating demand for higher-end electronic components. In this region, despite all challenges in manufacturing capacity, its technology-driven development focus remains supportive of steady market growth.

Top Companies Leading in the Compound Semiconductor Industry

Some of the leading compound semiconductor market companies include Infineon Technologies AG, Microchip Technology Inc., Mitsubishi Electric Corporation, Nexperia, NXP Semiconductors, Onsemi (Semiconductor Components Industries, LLC), Qorvo Inc., STMicroelectronics, Texas Instruments Incorporated, and Wolfspeed Inc., among others. On 11th September 2024, Infineon Technologies was able to successfully produce the world's first 300 mm power GaN wafer technology, claiming to be the world's first company to master this breakthrough technology in an existing and scalable high-volume manufacturing environment. It believes that this breakthrough will be able to drive the market for GaN-based power semiconductors. Production on 300 mm wafers compared to 200 mm technology, offers 2.3 times more chips per wafer.

Global Compound Semiconductor Market Segmentation Coverage

- On the basis of the type, the market has been categorized into III-V compound semiconductor (gallium nitride, gallium phosphide, gallium arsenide, indium phosphide, and indium antimonide), II-VI compound semiconductor (cadmium selenide, cadmium telluride, and zinc selenide), sapphire, IV-IV compound semiconductor, and others, wherein III-V compound semiconductor represent the leading segment, as they have excellent electronic and optoelectronic properties, offering them ideal materials in high-speed and high-frequency applications. They are used throughout 5G networks, in LED technology, and in solar cells, where the performance provided is superior in terms of energy efficiency and thermal stability. Their versatility across several industries ensures that they represent the largest segment of the market.

- Based on the product, the market is classified into power semiconductor, transistor, integrated circuits, diodes and rectifiers, and others, amongst which power semiconductor are at the forefront of the market as they have a prime role to play in many applications of energy-efficient power conversion and management, especially in electric vehicles, renewable energy systems, and industrial equipment. As they are capable of bearing high voltages and high currents, they form a crucial element in modern electronics. Hence, they form the biggest product segment in the market as energy optimization demand increases.

- On the basis of the deposition technology, the market has been divided into chemical vapor deposition, molecular beam epitaxy, hydride vapor phase epitaxy, ammonothermal, atomic layer deposition, and others. Among these, chemical vapor deposition accounts for the majority of the market share, due to its precision and efficiency in creating high-quality compound semiconductor layers. Widely used in manufacturing optoelectronic and power devices, CVD ensures superior material uniformity and scalability. Its adoption across industries like telecommunications, automotive, and renewable energy solidifies its position as the largest deposition technology segment in the market.

- Based on the application, the market is segregated into IT and telecom, aerospace and defense, automotive, consumer electronics, healthcare, and industrial and energy and power. The demand curve for compound semiconductors is led by the IT and telecom sector due to its wide rollout of 5G and high-speed data networks. Compound semiconductors help in power management efficiently, signal amplification, and high-frequency operation of telecom infrastructure. As global connectivity and data demands grow, IT and telecom remain the dominant application segments in the market.

| Report Features | Details |

|---|---|

| Market Size in 2024 | USD 122.8 Billion |

| Market Forecast in 2033 | USD 177.0 Billion |

| Market Growth Rate 2025-2033 | 4.1% |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered |

|

| Products Covered | Power Semiconductor, Transistor, Integrated Circuits, Diodes and Rectifiers, Others |

| Deposition Technologies Covered | Chemical Vapor Deposition, Molecular Beam Epitaxy, Hydride Vapor Phase Epitaxy, Ammonothermal, Atomic Layer Deposition, Others |

| Applications Covered | IT And Telecom, Aerospace and Defense, Automotive, Consumer Electronics, Healthcare, Industrial and Energy, and Power |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Infineon Technologies AG, Microchip Technology Inc., Mitsubishi Electric Corporation, Nexperia, NXP Semiconductors, Onsemi (Semiconductor Components Industries, LLC), Qorvo Inc., STMicroelectronics, Texas Instruments Incorporated, Wolfspeed Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Browse IMARC Related Reports on Compound Semiconductor Market:

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)